Most financial professionals–to include those that work in the banking industry–do not have a clear understanding of how money and banking work on a gold standard. This is hardly something to be ashamed of–most mathematicians don’t have a clear understanding of how an abacus works, and yet no one would consider that a negative mark. There’s no responsibility to understand the inner workings of the antiquated, obsolete technologies of one’s field.

With that said, there’s a lot of value to be gained from learning how money and banking work on a gold standard–both the “free banking” and the “central banking” varieties. There’s also value in learning how the U.S. monetary system got from where it was in the 17th century to where it is today. The field of money and banking is filled with concepts that are difficult to intuitively grasp–concepts like reserves, deposits, base money, money multiplication, and so on. In a study of the gold standard and its history, each of these concepts is made concrete–you can readily point to the piece of paper, or the block of metal, that each concept refers to. Ironically, the intricacies of the modern monetary system are easier to understand once one has learned how the equivalent concepts work on a gold standard.

In this piece, I’m going to carefully and rigorously explain how different types of gold standards work. I’m going to begin with a discussion of how bartering gives rise to precious metals as a privileged asset class. I’m then going to discuss money supply expansion on a gold standard–what the actual mechanism is. After that, I’m going to discuss David Hume’s famous price-specie flow mechanism, which maintains a balance of payments between regions and nations that use a gold standard. I’m then going to discuss the underlying mechanics of fractional-reserve free banking, to include a discussion of how it evolved. After that, I’m going to explain how the market settles on an interest rate in a fractional-reserve free banking system. I’m then going to explain how fractional-reserve central banking works on a gold standard, to include a discussion of the use of reserve requirements and base money supply expansion and contraction as a means of controlling bank funding costs and aggregate bank lending. Finally, I’m going to refute two misconceptions about the Gold Standard–first, that it caused the Great Depression (it categorically did not), and second, that its reign in the U.S. ended in 1971 (not true–its reign ended in the Spring of 1933).

Bartering, Precious Metals, and Mints

We begin with a simple barter economy in which individuals exchange goods and services directly, without using money. In a barter economy, certain commodities will come to be sought after not only because they satisfy the wants and needs of their owners, but also because they are durable and easy to exchange. Such commodities will provide their owners with a means through which to store wealth for consumption at a later date, by trading. On this measure, metals–specifically, precious metals–will score very high, and will be conferred with a trading value that substantially exceeds their direct and immediate usefulness in everyday life. The Father of Economics himself explains,

“In all countries, however, men seem at last to have been determined by irresistible reasons to give the preference, for this employment, to metals above every other commodity. Metals can not only be kept with as little loss as any other commodity, scarce any thing being less perishable than they are, but they can likewise, without any loss, be divided into any number of parts, as by fusion those parts can easily be reunited again; a quality which no other equally durable commodities possess, and which more than any other quality renders them fit to be the instruments of commerce and circulation. Different metals have been made use of by different nations for this purpose. Iron was the common instrument of commerce among the antient Spartans; copper among the antient Romans; and gold and silver among all rich and commercial nations.” (Adam Smith, The Wealth of Nations, 1776–Book I, Chapter IV, Section 4 – 5)

Crucially, the trading value of precious metals will end up being grounded in a self-fulfilling belief and confidence in that value, learned culturally and through a process of behavioral reinforcement. Individuals will come to expect that others will accept precious metals in exchange for real goods and services in the future, therefore they will accept precious metals in exchange for real goods and services now, holding the practice in place and validating the prior belief and confidence in it. Every form of money gains its power in this way–through the self-fulfilling belief and confidence that it will be accepted as such.

Now, in economic systems where precious metals are the predominant form of money, two practical problems emerge: measurement and fraud. It is inconvenient for individuals to have to measure the precise amount of precious metal they are trading every time they trade. Furthermore, what is presented as a precious metal may not be fully so–impurities may have been inserted to create the illusion that more is there than actually is.

The inevitable solution to these problems comes in the form of “Mints.” Mints are credible entities that use stamping and engraving to vouch for the weight and purity of units of precious metal. The Father of Economics again,

“People must always have been liable to the grossest frauds and impositions, and instead of a pound weight of pure silver, or pure copper, might receive in exchange for their goods, an adulterated composition of the coarsest and cheapest materials, which had, however, in their outward appearance, been made to resemble those metals. To prevent such abuses, to facilitate exchanges, and thereby to encourage all sorts of industry and commerce, it has been found necessary, in all countries that have made any considerable advances towards improvement, to affix a publick stamp upon certain quantities of such particular metals, as were in those countries commonly made use of to purchase goods. Hence the origin of coined money, and of those publick offices called mints.” (Adam Smith, The Wealth of Nations, 1776–Book I, Chapter IV, Section 7, emphasis added)

Mining and Money Supply Growth

In a healthy, progressing economy, where learning, technological innovation and population growth drive continual increases in output capacity–increases in the amount of wanted “stuff” that the economy is able to produce each year–the supply of money also needs to increase. If it doesn’t increase, the result will either be deflation or economic stagnation (for a clear explanation of the reasons why, click here). Both of these options are undesirable.

Fortunately, in a metal-based monetary system, there is a natural mechanism through which the money supply can expand: mining. Miners extract metals from the ground. They take the metals to mints to have them forged into coins. They then spend the coins into the economy, increasing the money supply.

The problem, of course, is that there is no assurance that the output of the mining industry, which sets the growth of the money supply, will proceed on a course commensurate with growth in the output capacity of the real economy–its ability to to produce the real things that people want and need. If the mining industry produces more new money than can be absorbed by growth in the economy’s output capacity, the result will be inflation, an increase in the price of everything relative to money. This is precisely what happened in Europe in the years after the Spanish and Portuguese discovered and mined The New World. They brought its ample supply of precious metal back home to coin and spend–but the economy’s output capacity was no different than before, and could not meet the demands of the increased spending. In contrast, if the mining industry does not produce enough new money to keep up with growth in the economy’s output capacity, the result will be deflation–what Europe frequently saw in the periods before the discovery of The New World.

In a metal-based monetary system, there is a natural feedback that helps keep the mining industry from producing too much or too little new money. If the industry produces too much new money, the ensuing inflation of prices and wages will make mining less profitable in real terms, and discourage further investments in mining. If the mining industry does not produce enough new money, the deflation of prices and wages will make mining more profitable in real terms, and encourage further investments in mining. To the extent that a metallic monetary system is closed to external flows, this feedback is the only feedback present to stabilize business cycles. Obviously, it can’t act quickly enough or with enough power to keep prices stable, which is why large cycles of inflation and deflation frequently occurred prior to the development and refinement of modern central banking.

If it seems crazy to think that humanity could have survived under such a primitive and constricted monetary arrangement–an arrangement where a limited, unsupervised, unmanaged supply of a physical object forms the basis of all major commerce–remember that the economies of the past were not as specialized and dependent upon money and trade as they are today. Trading in money would have been something that the wealthy and royal class would ever have to worry about. The rest would meet the basic needs of life–food, water, shelter–by producing it themselves, or by working for those with means and receiving it directly in compensation, as a serf in a feudal kingdom might do.

The Price-Specie Flow Mechanism

What is unique about a metal-based monetary system is that money from any one country or geographic region can easily be used in any other, without a need for conversion. All that is necessary is that individuals trust that the money consists of the materials that it claims to consist of, as signified in its stamp or engravement. Then, it can be traded just as its underlying materials would be traded. After all, it is those materials–its being those materials is the basis for its being worth something.

In early British America, Spanish silver dollars, obtained from trade with the West Indies, were a popular form of money, owing to the tight supply of British currency in the colonies. To use the Spanish dollars in commerce, there was no need to convert them into anything else; they were already 387 grains of pure silver, their content confirmed as such by the mark of the Spanish empire.

The prospect of simple, undistorted international flows under a metal-based monetary system gives way to an important feedback that enforces a balance of payments between different regions and nations and that acts to stabilize business cycles. This feedback is called the “price-specie flow mechanism”, introduced by the philosopher David Hume, who explained it in the following passage:

“Suppose four-fifths of all the money in Great Britain to be annihilated in one night, and the nation reduced to the same condition, with regard to specie, as in the reigns of the Harrys and Edwards. What would be the consequence? Must not the price of all labour and commodities sink in proportion, and every thing be sold as cheap as they were in those ages? What nation could then dispute with us in any foreign market, or pretend to navigate or to sell manufactures at the same price, which to us would afford sufficient profit? In how little time, therefore, must this bring back the money which we had lost, and raise us to the level of all the neighbouring nations? Where, after we have arrived, we immediately lose the advantage of the cheapness of labour and commodities; and the farther flowing in of money is stopped by our fulness and repletion.” (David Hume, Political Discourses, 1752–Part II, Essay V, Section 9)

“Again, suppose, that all the money of Great Britain were multiplied fivefold in a night, must not the contrary effect follow? Must not all labour and commodities rise to such an exorbitant height, that no neighbouring nations could afford to buy from us; while their commodities, on the other hand, became comparatively so cheap, that, in spite of all the laws which could be formed, they would be run in upon us, and our money flow out; till we fall to a level with foreigners, and lose that great superiority of riches, which had laid us under such disadvantages?” (David Hume, Political Discourses, 1752–Part II, Essay V, Section 10)

For a relevant example of the price-specie flow mechanism in action, suppose that Europe is on a primitive gold standard, and that Germans make lots of stuff that Greeks end up purchasing, but Greeks don’t make any stuff that Germans end up purchasing. Money–in this case, gold–will flow from Greece to Germany. The Greeks will literally be spending down their money supply, removing liquidity and purchasing power from their own economy. The liquidity and purchasing power will be sent to Germany, where it will circulate as income and fuel a German economic boom. The ensuing deflation of prices and wages in Greece, and the ensuing inflation of prices and wages in Germany, will prevent Greeks from purchasing goods and services from Germany, and will make it more attractive for Germans to purchase goods and services from Greece (or to invest in Greece). Money–again, gold–will therefore be pulled back in the other direction, from Germany back to Greece, moving the system towards a balanced equilibrium.

It is only with fiat money, money that can be created by a government at will, that this mechanism can be circumvented. The Chinese monetary authority, for example, can issue new Renminbi and use them to purchase U.S. dollars, exerting artificial downward pressure on the Renminbi relative to the U.S. dollar, and preserving a large trade imbalance between the two nations. Metal, in contrast, cannot be created at will, and so there is no way to circumvent the mechanism under a strict metallic monetary system.

Paradigm Shift: The Development of Fractional-Reserve Free Banking

Up to now, all we have for money are precious metals–coins and bars of gold and silver. There are promises, there is borrowing, there is debt–but these are not redeemable on demand for any defined amount. Anyone who accepts them as payment must accept illiquidity or the risk of mark-to-market losses if the holder chooses to trade them.

The paradigm shift that formally connected borrowing and debt with securities redeemable on demand for a defined amount occurred with the development of free banking. Historically, savers sought to keep their supplies of gold and silver–in both coin and bar form–in safe deposits maintained by goldsmiths. The goldsmiths would charge a fee for the deposit, and would issue a document–a banknote–redeemable for a certain amount of gold and silver on the holder’s request. Given that the goldsmiths generally had reputations as honest dealers, the banknotes would trade in the market as if they were the very gold and silver that they could be redeemed for.

Eventually, the goldsmiths realized that not everyone came to redeem their gold and silver deposits at the same time. The gold and silver deposits coming in (i.e., the banknotes being created) would generally balance out with the gold and silver deposits leaving (i.e., the banknotes being redeemed). This balancing out of incoming and outgoing deposit flows allowed the goldsmiths to issue more banknotes than they were storing in actual gold and silver. They could print and loan out banknotes in excess of the gold and silver deposits that they actually had on hand, and receive interest in compensation. Thus was born the phenomenon of fractional-reserve banking.

Initially, the banking was “free” banking, meaning that there was no government involvement other than to enforce contracts. The banknotes of each bank were accepted as payment based on the reputation and credibility of the bank. Each bank could issue whatever quantity of banknotes, over and above its actual holdings of gold and silver, that it felt comfortable issuing. But if the demand for redemption in gold and silver exceeded the supply on hand, that was the problem of the banks and the depositors–not the problem of the government or the taxpayer.

The U.S. operated under a free banking system from the initial Coinage Act of 1792 all the way until the Civil War. The currency was defined in terms of gold, silver and copper as follows:

Citizens would send the requisite amount of precious metal to the U.S. mint and have it coined for a small fee. They would then store the coins–and whatever other form of precious metal they owned–in banks, and receive banknotes in exchange. Individual banks issued different individual banknotes, with different designs.

In lieu of banknotes, bank customers also accepted simple deposits, against which they could write cheques. The difference between a cheque and a banknote is that a banknote represents a promise to pay to the holder, on demand. A cheque represents an order to a bank to pay a specific person, whether or not she is currently holding the cheque. So, for example, if I have a deposit account with Pittsfield bank in Massachussets, and I write a cheque to someone, that person has to deposit the cheque in order to use it as currency. He can’t trade it with others directly as money, because it was written to him from me. He has to take the cheque to his bank–say, Windham bank–to cash it (or deposit it). In that case, coins (gold and silver) will be transferred from Pittsfield to Windham. In contrast, if I give the person a banknote from Pittsfield as payment, he can use it directly in the market–provided, of course, that Pittsfield has a sound reputation as a bank.

The issuance of banknotes, and their widespread acceptance as a working substitute for the actual metallic money that they were redeemable for, created a mechanism through which the money supply–the supply of legal tender that had to be accepted to pay debts public and private–could expand in accordance with the economy’s needs. Granted, prior to the advent of fractional-reserve banking, it was possible to trade debt securities and debt contracts in lieu of actual gold and silver–but these securities and contracts were not redeemable on demand. The recipient had to accept a loss of liquidity and optionality in order to take them as payment. A banknote, in contrast, is redeemable on demand, by anyone who holds it, therefore it is operationally equivalent to the legal money–the coined precious metal–that backs it.

A true gold standard is a gold standard built on fractional-reserve free banking. The government defines the value of the currency in terms of precious metals, and then leaves banks in the private sector to do as they please–to issue whatever quantity of banknotes they want to issue, and to pay the price in bankruptcy if they behave in ways that create redemption demand in excess of what they can actually redeem. There is no government intervention, no regulatory imposition, no reserve requirement, no capital ratio–just the supervision of market participants themselves, who have to do their homework.

The Unstable Mechanics of Fractional-Reserve Free Banking

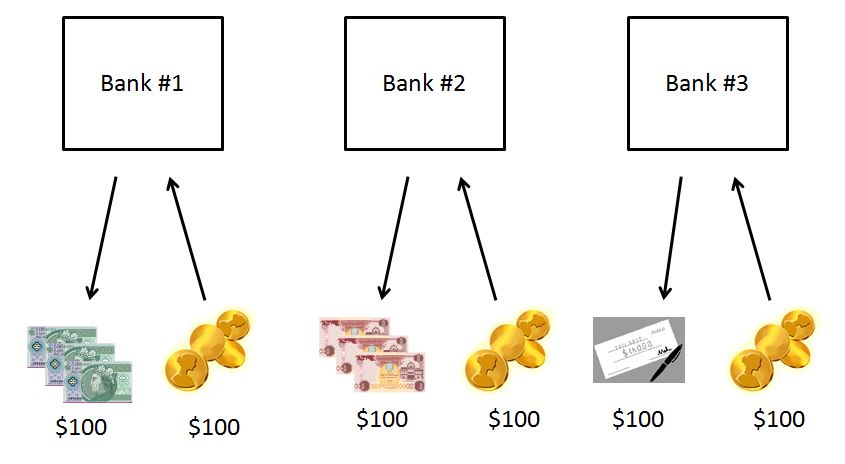

The following chart show how gold-based fractional-reserve free banking functions in practice.

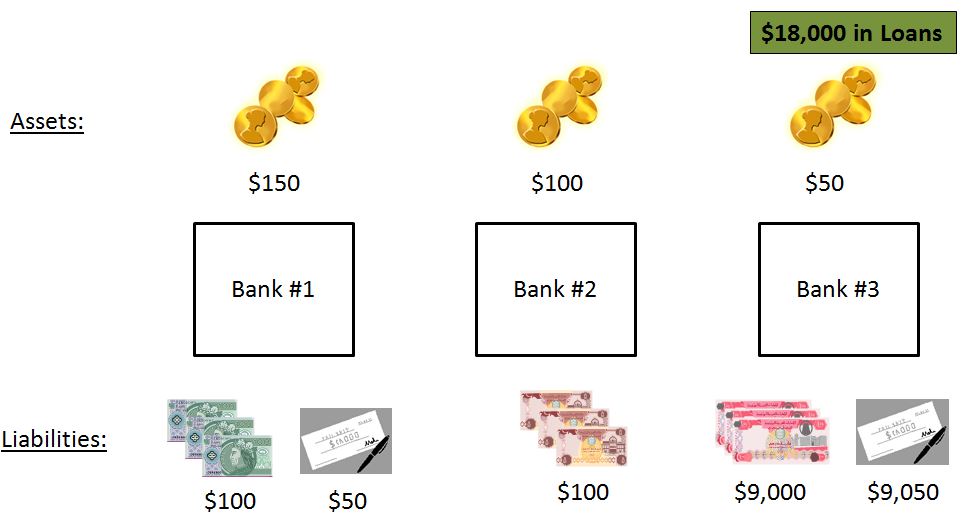

We begin before there has been any lending. Banks #1 and #2 have each received $100 in gold and have each issued $100 in banknotes to customers in exchange for it. Bank #3 has received $100 in gold and has issued checkable deposit accounts to customers with $100 recorded in them. We can define the M2 money supply to be the sum of banknotes, checking accounts, and gold and silver held privately, outside of banks. The M2 money supply for the system is then $300. We can define the base money supply to be the total supply of gold in the system. The base money supply is then $300. The base money supply equals the M2 money supply because there hasn’t yet been any lending. Lending is what will cause the M2 money supply to grow in excess of the base money supply.

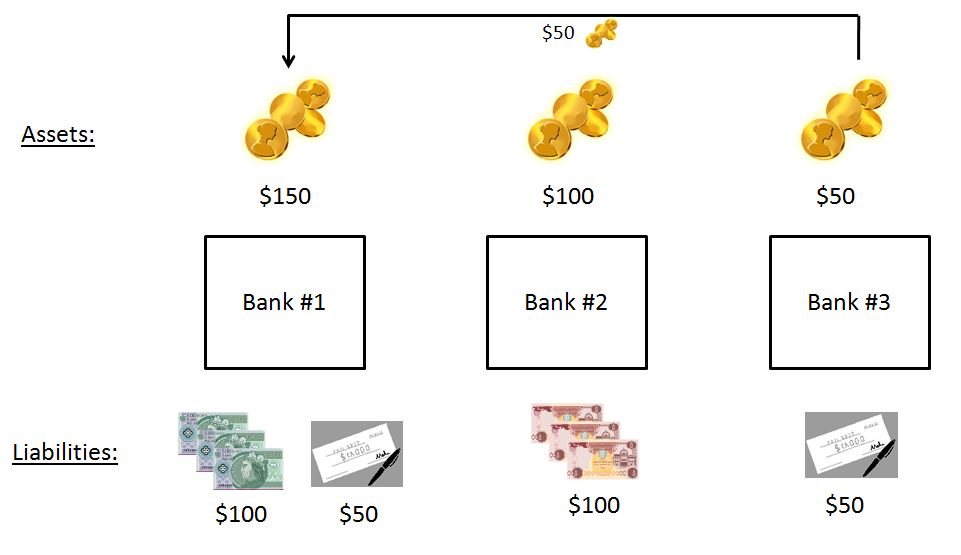

Let’s assume that a customer of Bank #3 writes a check for $50 to a person who deposits the check at Bank #1. At the end of the day, when the banks settle their payments, Bank #3 will send $50 worth of gold to Bank #1, and will reduce the customer’s deposit account by $50.

Here, we’ve broken the banking system out into assets and liabilities. The assets of the banking system are $300, all in the form of gold. The liabilities are also $300, in the form of banknotes and deposit accounts, both of which can be redeemed for gold on demand. The assets and the liabilities are equal because the banks aren’t carrying any of their own capital (and that’s fine–they don’t need to, there’s no regulator to impose a capital requirement in a free-banking system).

Now, let’s assume that Bank #3 issues new loans to customers worth $18,000.

We’ll assume that half of the loans are issued to the borrowers in the form of banknotes, and half are issued in the form of deposits, held at Bank #3. Crucially, Bank #3 has printed this new money out of thin air. That’s what banks do when they lend to the non-financial sector or purchase assets from the non-financial sector–they print new money. All banks do this, not just central banks. The money can be used like any other money in the system, provided that people trust the bank.

Taking a closer look at Bank #3, it now has $18,050 of assets, and $18,050 of liabilities. The assets are composed of $50 worth of base money (gold), and $18,000 worth of loans, which are obligations on the part of the customers to repay what was borrowed, with interest. The liabilities are $9,000 worth of banknotes, and $9,050 worth of deposit accounts.

Now, we can define the term “reserve” to mean any money–in this case, gold, because we’re on a gold standard–that the banking system is holding that can be used to meet redemption requests. Right now, the total quantity of reserves in the system equals the total quantity of base money, because all of the base money–all of the gold–is being held inside the banking system. All of the gold is in the hands of the banks and available to fund redemptions. Nobody has taken any gold out; there are no private holders.

If a customer writes a check out of his account in Bank #3, and that check gets deposited in Bank #1, Bank #3 will transfer reserves–in this case, gold–to Bank #1. Similarly, when a customer redeems one of Bank #3’s banknotes, reserves–again, gold–will be moved from Bank #3 into the hands of the customer.

So let’s assume that a customer of Bank #3 writes a $75 cheque that gets cashed at Bank #1. Alternatively, let’s assume that a customer tries to redeem $75 worth of Bank #3’s banknotes for gold. What will happen? Notice that Bank #3 doesn’t have $75 worth of reserves–gold on hand–to transfer to Bank #1, or to give to the customer that wants to take the gold out. So it will have to default on its liabilities. It promised to redeem the banknote in gold on demand, and it can’t.

We’ve arrived at the obvious problem with free banking on a gold standard. There’s no reserve requirement, no requirement for a capital cushion, and no lender of last resort. The system is therefore highly unstable, and becomes all the more unstable as the quantity of lending (which is determined by the investment and spending appetite of borrowers, and by the risk appetite of lenders) grows relative to the quantity of gold (which is determined by the business activities of gold miners, independently of what the economy is doing elsewhere).

If even a small fear of illiquidity or insolvency at a bank develops, it can snowball into a full-on bank run–of which there were far too many in the free-banking era. Granted, to help each other meet redemption requests, banks can issue short-term overnight gold loans to each other. But this isn’t enough to create stability; in times of trouble, when such lending is most needed, it will tend to disappear.

In addition to being unstable, free banking systems are also undesirable pro-cyclical. To understand the pro-cyclicality, we have to step back and examine how interest rates work in a free banking system.

Interest Rates in a Free Banking System

In a modern system, the central bank controls short-term low-risk interest rates–the rates at which banks borrow from each other, and at which they borrow from their customers (who hold deposits with them). That interest rate is the funding cost of the banking system. Its expected future trajectory plays a crucial role in determining interest rates across all other parts of the yield curve.

But we don’t have a central bank right now. We just have gold, and the market. How, then, will the system settle on an interest rate? The equilibrium value of any market interest rate will be a function of (1) the supply of funds that lenders wish to lend out and (2) the demand on the part of borrowers to borrow funds. If there is a high demand for borrowing, and a low supply of funds that lenders want to lend out, the market will tend to equilibriate at a high interest rate. If there is a low demand for borrowing, and a large supply of funds that lenders want to lend out, the market will tend to equilibriate at a low interest rate.

In good economic times, banks are going to feel confident, comfortable–willing to lend excess funds to each other. Customers will feel similar–willing to trust that the gold that backs their deposit accounts and banknotes is safe and sound inside bank vaults. They will not demand much in the form of interest to store their money, provided that they will be able to retain access to its use (and they will–there is no loss of liquidity when gold is deposited in a checking account or exchanged for a banknote–the money can still be spent now). The interest rate at which banks borrow from each other and from their customers will therefore be low. But we don’t want it to be low. We want it to be high, because environments of confidence and comfort are the kinds of environments that produce excessive, imprudent, unproductive lending and eventual inflation.

The only reason that banks would pay a high rate to borrow funds (gold) from each other, or from their customers, would be if they were facing redemption requests, or if they were uncomfortable with the amount of gold that they had on hand to meet redemption requests. Again, recall that banks don’t lend out their reserves–the actual base money, the gold. Those reserves are simply there to meet customer requests to redeem the banknotes and deposits that they create out of thin air.

But if times are good, banks aren’t going to be afraid of redemption requests. There lack of fear will be justified, as there aren’t going to be very many panicky customers trying to redeem. This setup will make it even easier for them to lend. In theory, as long as no one tries to redeem, they can offer an infinite supply of loans to the market, with each loan representing incremental profit. That’s obviously not what we want here. In good times, we want tighter monetary conditions, a tighter supply of loans to be taken out, in order to discourage excessive, imprudent, unproductive lending, and to mitigate an eventual inflation.

In bad times, the reverse will prove true. Banks won’t lend to each other, even when they have good collateral to post, and customers won’t be comfortable holding their savings in banks. They will want to take their savings out–which means taking out gold, and pushing the system towards default. Without a lender of last resort, the system will be at grave risk of seizing up, especially as rumors and stories of failed redemptions spread. Lest there be any confusion, this happened many times in the 19th century. During periods of economic contraction, the system was an absolute disaster, which is the reason why the country moved away from free banking, and towards a system of central banking.

Now, to be fair, free banking does offer a natural antidote to inflation. If excessive lending brings about inflation, market participants will redeem their gold and invest and spend it abroad (purchase cheap imports), in accordance with the price-specie flow mechanism. This will remove gold from the banking system, and raise the cost of funding for banks–assuming, of course, that banks feel a need to maintain a healthy supply of reserves. But again, in good times, there is nothing to say that banks will feel such a need. Inflation, and the ensuing migration of gold out of the system, is not likely to stop excessive lending in time to prevent actual problems. To the contrary, the migration of gold out of the system is likely to be a factor that only forces a reaction after it’s too late, after the economy is already in recession, when further risk-aversion and monetary tightness on the part of banks will be counterproductive.

Central Banking on a Gold Standard

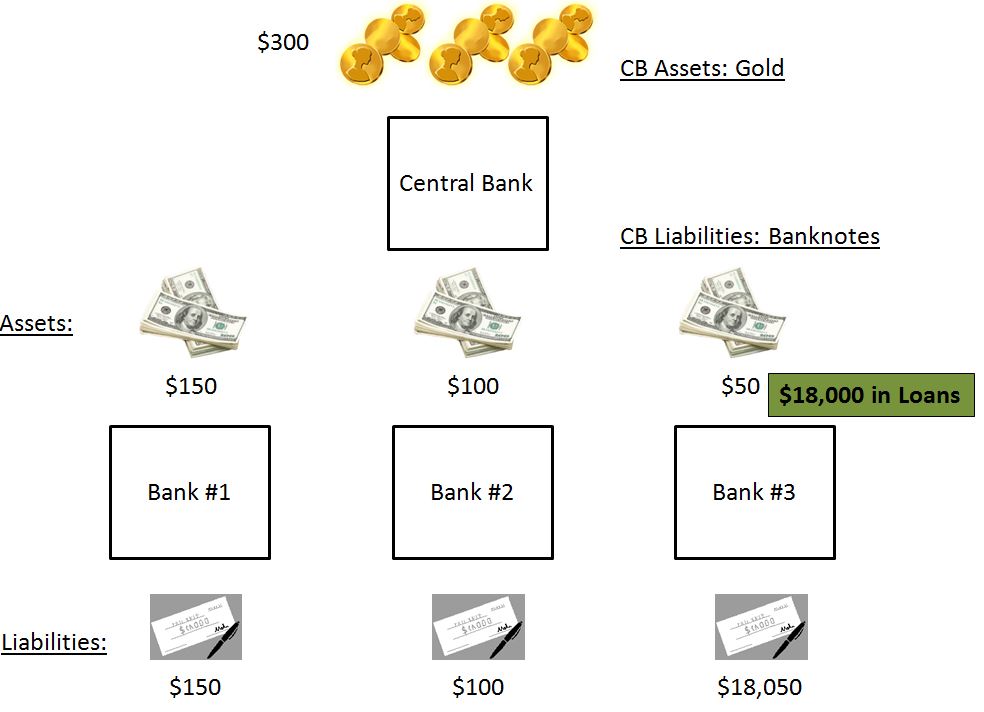

With the passage of the Federal Reserve Act in 1913, the U.S. financial system finalized its transition from a free banking system to a central banking system, using a gold standard. The following chart, which begins where the previous chart left off, gives a rough illustration of the way the system worked:

The system worked as follows. Private citizens would deposit their gold with private banks and receive credited deposit accounts in exchange. The private banks would then deposit the gold with the central bank. In exchange for the gold, the private banks would receive banknotes–in this case, Federal Reserve banknotes, “greenbacks.” As before, in lieu of receiving and holding actual paper banknotes from the central bank, the banks could receive credits on their deposit accounts with the central bank. To keep things simple and intuitive from here forward, I’m going to treat these deposit accounts as if they were simple paper banknotes held by the banks in vaults–they just as easily could be.

Instead of depositing gold with private banks, citizens could also deposit their gold directly with the central bank, and receive banknotes directly from the central bank in exchange. But the banknotes would eventually end up on deposit at private banks, where people would store money. So the system would arrive at the same outcome.

Notice that in this model, the central bank is fulfilling the same role that private banks fulfilled on the free banking model. It is issuing banknotes that can be redeemed on demand in gold, against a reserve supply of gold to meet potential redemption requests. Crucially, it has the power to issue an amount in banknotes that is greater than the amount that it is actually carrying in gold. It therefore has the power to act as a genuine fractional-reserve bank. That power is what allows it to expand the monetary base, control short-term interest rates, and function as a lender of last resort. As long as customers do not seek to redeem their banknotes for gold in an amount that exceeds the amount of gold that the central bank actually has on hand, then the central bank can issue, out of thin air, as many banknotes as it wants.

This is actually a common misconception–that the central bank on a gold standard is necessarily constricted by the supply of physical gold. Not true. What constricts the central bank on a gold standard is (1) the amount of confidence that the public has in the central bank and (2) the severity of trade imbalances. If the public does not panic and try to redeem gold, and if the price-specie flow mechanism does not force a gold outflow in response to a substantial trade imbalance, then a gold standard will impose no constraint on the central bank at all.

Now, what is critically different from the free banking model is that the central bank imposes a reserve requirement on the private banks. They have to hold a certain quantity of banknotes as reserves in their vaults equal to a percentage of their total deposit liabilities.

You might think that the purpose of this requirement is to ensure that the banks maintain sufficient liquidity to meet possible redemptions–in our Americanized example, customers going to the bank and asking to redeem their deposits in greenbacks, or writing cheques on their deposit accounts which then get cashed at other banks, forcing a transfer of greenbacks from the bank in question to those other banks. But the system now has a lender of last resort–the Fed. That lender is there to print and loan to banks any greenbacks that are needed to meet redemption requests. As long as the Fed is willing to conduct this lending, there is no need for the banks to hold any reserves at all.

The real reason why the reserve requirement exists is to allow the central bank to control the proliferation of bank lending, and to therefore maintain price stability. Notice that if there were no reserve requirement, it would be up to the banks to decide how much “funding” they needed. As long as their incoming deposits consistently offset their outgoing deposits (those redeemed for greenbacks or cashed via cheque in other banks), they could theoretically loan out an infinite supply of new deposits (that is, print an infinite supply of new money), against a very small supply of banknotes on reserve in vault, or even against no banknote reserves at all.

The central bank controls the proliferation of bank lending by controlling its cost–by making it cheap or expensive. It controls the cost of bank lending by setting a reserve requirement, and then using open market operations–asset purchases and sales–to control the total amount of banknotes in the banking system. If we assume that all but a few banknotes will end up deposited in banks, then the total amount of banknotes in the banking system just is the total quantity of funds available for banks to use to meet their reserve requirements.

When the central bank makes purchases from the private sector, it takes assets out of the system, and puts banknotes in. Prior to the purchases, the assets were being held directly by the individuals that owned them–with no involvement from banks (unless banks were the owners, which we’ll assume they weren’t). But the individuals have now sold the assets to the central bank, and have received banknotes instead. They’re going to take those banknotes to banks and deposit them. The banknotes will therefore become bank funds, stored in a vault, which can be used to meet reserve requirements. You can see, then, how asset purchases end up putting funds into the banking system. Asset sales take them out, through a process that is exactly the reverse.

If you add up all of the bank loans in the economy, you will get some number–in our earlier example, that number was $18,000. If there is a 10 to 1 reserve ratio requirement, then you can know that banks, collectively, will need to hold $1,800–$18,000 divided by 10–in banknote reserves in their vaults to be compliant with the reserve requirement.

Suppose that the central bank purchases assets so that the total quantity of banknotes in the system ends up being something like $3,600. In aggregate, banks will end up with significantly more banknotes than they need to meet the $1,800 reserve requirement. Of course, some banks, like Bank #3 in our earlier example, may end up being right up against the reserve requirement, or even in violation of it. But if that’s true, then other banks will necessarily have an excess supply of banknotes on reserve that can be lent out. In aggregate, the demand for banknotes–reserves, monetary base, all the same–will be well-quenched, and the rate at which banks lend to each other will be very low–in this case, close to zero.

Now, suppose instead that the central bank sells assets so that the total quantity of banknotes in the system ends up being something like $1,802. In aggregate, the banking system will have $2 worth of excess funds that won’t need to be held on reserve in vault, and that can be lent out to other banks. It goes without saying that the cost of borrowing that $2 will be very high, and therefore the probability that the banking system will add another $20 to its aggregate supply of loans (what $2 of extra reserves allows on a 10 to 1 reserve ratio) will be very low. By shrinking the supply of banknotes down to $1,802, just above what is necessary for the aggregate banking system, with its current quantity of outstanding loans, to be compliant with the reserve requirement, the central bank has successfully discouraged further bank lending. If the central bank wants, it can even force banks to reduce their outstanding loans. Just sell assets so that the quantity of reserves falls below $1,800–then, to be compliant with the reserve requirement, banks in aggregate will need to call loans in or sell them to the non-financial sector.

Two Misconceptions About the Gold Standard

Before concluding I want to clear up two misconceptions about the Gold Standard. The first misconception relates to the idea that the gold standard somehow caused or exacerbated the Great Depression. This simply is not true. What caused and exacerbated the Great Depression, from the Panic of 1930 until FDR’s banking holiday in the spring of 1933, was the unwillingness on the part of the Federal Reserve to lend to solvent but illiquid banks. The Fed of that era had come to embrace a perverse, moralistic belief that the underlying economy was somehow broken, damaged by promiscuous malinvestment associated with the prior expansion, and that it needed to be allowed to take the painful medicine that it had coming–even if this entailed massive bankruptcies and bank failures. The “cleansing” would be good in the long run, or so they thought.

The Fed’s refusal to lend to banks facing runs had nothing to do with any constraint associated with the gold standard. Indeed, the Fed at the time was flush with gold–it held a gold reserve quantity equal to a near-record 80% of the outstanding base money that it had created. For context, in 1896, the Treasury (which was then in control, prior to the creation of the Fed) let its gold reserves fall to 13% of its outstanding supply of base money.

Not only did the Fed have adequate reserves against which to lend to banks, it potentially could have conducted a large quantitative easing program–while on a gold standard. The risk, of course, would have been that an economically illiterate public might have tried to protect itself by redeeming gold en masse–then, the Fed would have had to stop, to avoid a contagious process of redemption and a potential default. This risk–that an economically illiterate public might panic and seek to redeem gold in numbers that exceed what the central bank has on hand–is the only risk that a central bank ever really faces on a gold standard. Either way, it wouldn’t have made too much of a difference, as the efficacy of QE is highly exaggerated. An economy in the doldrums can recover without it. But no economy can recover as long as its banking system is in an acute liquidity crisis. The Fed had ample power to resolve the liquidity crisis that the financial system was facing at the time, and a clear mandate in its charter to resolve it–but it chose not to, for reasons that had nothing to do with gold.

The second misconception pertains to the idea that US financial system was somehow on a gold standard after 1933. It was not. The gold standard ended in the Spring of 1933, when FDR issued executive order 6102. This order made it illegal for individuals within the continental United States to own gold. If gold can’t be legally owned, then it can’t be legally redeemed. If it can’t be legally redeemed, then it can’t constrain the central bank.

The gold standard that was in place from the mid 1930s until 1971 was figurative and ceremonial in nature. The Fed’s gold, which “backed” the dollar, could not be redeemed by the public, therefore the backing had no bite. It did not effectively constrain the Fed or the money supply. That much should obvious–if a gold standard had existed in the 1940s, and had constrained the Fed’s actions, the country would not have been able to finance the massive, record-breaking government deficits of World War 2. Those deficits were financed almost entirely by Fed money creation.

Now, to be clear, on a fiat monetary system, the market retains the ability to put the central bank “in check.” Instead of redeeming money directly from the central bank in gold, market participants can “redeem” money by refusing to hold it, choosing instead to hold assets that they think will retain value–land, durables, precious metals, foreign currencies, foreign securities, foreign real estate, etc. If this happens en masse, and if there is a concomitant monetary expansion taking place alongside it, the result will be an uncontrolled inflation. The probability that such a rejection will occur is obviously much less on a fiat system, where the option of gold redemption isn’t there to tempt things. But the theoretical power to reject the money as money, which is what the idea of gold redemption formalizes, is still there.

Conclusion

Contrary to the usual assumptions, the fiat monetary system that we currently use is not that different from the gold-based system in use in the early 20th century. All one has to do to get from such a system, to our current system, is (1) make everything electronic, and (2) delete the gold. Just get rid of it, let the central bank create as much base money as it wants, against nothing, or against gold that, by law, cannot be redeemed (the setup from 1933 to 1971).

The reason not to use monetary systems based on gold is that they are obsolete and unnecessary, with no real benefits over fiat systems, but with many inconveniences and disadvantages. In a fiat system, the central bank can create base money in whatever amount would be economically appropriate to create. But on a gold-based system, the central bank is forced to create whatever amount of base money the mining industry can mine, and to destroy whatever amount of base money a panicky public wants destroyed. There’s no reason to accept a system that imposes those constraints, even if they aren’t much of a threat in the majority of economic environments. If the goal is to constrain the central bank, then constrain it directly, with laws. Put a legal limit on how much money it can issue, or on what it can purchase. Alternatively, if you are a developing country that does not enjoy the confidence of the market, peg your currency to the currency of a country that does enjoy that confidence. There is no need for gold.