In the first century, the historian Plutarch introduced a famous philosophical paradox. The paradox goes like this. A ship–“The Ship of Theseus”–was returning home to Athens from Crete. As it sailed, the wooden planks that made up its structure gradually decayed. The sailors kept the ship afloat by replacing the decaying planks, one by one, using fresh wood that they were carrying onboard. Eventually, the sailors replaced all of the wooden planks that made up the the ship’s original structure, so that the new form of the ship had no material in common with the old form. The question followed: was the ship the same ship through the change? If so, what made it the same ship, rather than a new ship, a different ship?

“For they took away the old planks as they decayed, putting in new and stronger timber in their places. The ship became a standing example among the philosophers of the logical question of things that grow: with one side holding that the ship remained the same, and the other contending that it was not the same.” — Plutarch, Theseus, 75 A.C.E.

Approximately 1500 years later, the philosopher Thomas Hobbes took the paradox further. He asked us to imagine the following. All of the old, decayed wood of the original Ship of Theseus is gathered up from scrap and used to build a new ship. There are then two ships: one ship that is spatially continuous with the original Ship of Theseus, whose material has been fully changed out, piece by piece, and another ship made from the scrap material of the original Ship of Theseus. Which of these ships is the true Ship of Theseus?

The “Ship of Theseus” problem frequently arises in the world of music fandom. Consider, for example, the 1970s soft rock group, the Little River Band, which produced famous hits such as “Reminiscing” and “Lonesome Loser“. To this day, the Little River Band remains together. But there are no current members of the band that were in the band when it was originally formed. All of the founding members, those who sang the hits as we are used to hearing them, have been swapped out. A “Ship of Theseus” question thus arises: is the band that currently goes on tour as “The Little River Band” the true Little River Band, or is it the equivalent of a cover band, singing the same songs, while only pretending to be the original? To add the Hobbesian twist, what if the original members of the Little River Band were to come together to form a new band, a cover band of the Little River Band. Would this new cover band be the true Little River Band, since it contains the founding members? Or would it be a mere replica, since it is not continuous with the original?

You’re probably asking yourself what relevance this paradox has to finance, or to anything. But now here’s a question for you. Suppose that we have an index of stocks that represents the equity market of a given country, an index that we use, without further questioning, to draw conclusions about important topics such as the country’s valuation and expected future performance. What would happen if, like planks on the Ship of Theseus, or members of the Little River Band, most or all of the individual companies in the index were to be removed, replaced with new companies? Would the index remain the same index? Or would it become a different index?

The question of “sameness” and “difference” is inherently metaphysical, and therefore has no answer. But there is a more practical question that we as investors have to be concerned with. That question is this. Given radical changes in the constituents of an index, is it appropriate to use the index’s historical metrics–its historical earnings, growth rates, valuations, profit margins, returns on equity, and so on–to draw conclusions about what the index’s future performance is likely to be?

Ireland: The Perfect International Value Play?

Looking out over the long-term, it’s going to be very difficult for US investors to receive the “normal” 10% nominal annual equity returns that they have received historically. Literally everything will have to go right. Profit margins and returns on equity will have to stay elevated, contrary to the tendency of mean-reversion. Multiples will also have to stay elevated, which means that interest rates will have to stay low. But low interest rates are a consequence of weak economic growth and weak inflation. How are companies going to consistently produce strong earnings per share (EPS) growth–the kind that would be needed to underpin 10% total returns for shareholders over the long-term–in an environment of weak economic growth and weak inflation?

Up to now in the current recovery, and really over the last 10 years, profit margin expansion and share buybacks have been the primary drivers of EPS growth for U.S. equities. They are the reasons that strong EPS growth has been possible amid the persistent softness in economic growth and inflation (softness that has depressed the corporate top-line, but that has also provoked zero interest rates and an elevated P/E multiple). Can profit margin expansion and share buybacks continue to be robust drivers of EPS growth, indefinitely, even as shares become more and more expensive for corporations to buy back, and as the income imbalances between capital and labor, the rich and everyone else, get closer and closer to the limits of economic and societal stability? There are good reasons to think not.

Because long-term equity returns in the U.S. are likely to be sub-par, many investors have turned to foreign equity markets for better opportunities. Where is the value in the equity world right now? According to the Shiller CAPE, a popular technique for measuring value across economic cycles, the value is in Europe, specifically, the distressed countries of the Eurozone.

In my view, out of all of the countries of the Eurozone, the most interesting from an investment perspective is Ireland. As a country, it has all of the features needed for strong long-term equity performance, features that many of its cousins in the Eurozone lack: a productive, highly-skilled, flexible labor force, capital-friendly, pro-business government policies, and a young, growing population in a demographic sweet spot. To complete the investment case, Irish stocks are apparently very cheap, with the Irish index sporting a Shiller CAPE under 10.

It would seem, then, that Ireland is set up to produce spectacular returns. But there’s a problem. If you look closely at the actual names that make up the Irish index, you will be hard-pressed to find significant value. The following table shows the constituents of the ISEQ 20, Ireland’s benchmark, sorted by market cap weighting as of March 2014:

Most of these companies enjoy above-average valuations. That’s to be expected, as the companies are high-quality. Glanbia? Kerry Group? Smurfit Kappa? Aryzta? These are growing, thriving businesses. They deserve to be priced as such.

There are two potential cases of deep value in the index: The Bank of Ireland and the building material producer CRH. But these companies together only make up 29% of the index capitalization. The majority of the index–71%–is composed of companies that are not deep value. How can an index represent deep value when 71% of its constituents are not deep value? How can an index trade at a CAPE below 10 when 71% of its constituent companies sport CAPEs significantly higher than that number? Where exactly is the low CAPEness coming from?

Enter the Ship of Theseus paradox. It turns out that many of the companies presently in the ISEQ 20 are new entrants, having replaced the financial roadkill that died off in Ireland’s massive housing bubble and subsequent banking crisis–roadkill that includes Anglo-Irish Bank, Allied Irish Banks, and so on. That roadkill is gone, forever, having either been nationalized or diluted into oblivion. But, crucially, the earnings that it generated during the bubble, from 2004 to 2008, is still part of the ISEQ’s earnings per share during those periods, and is therefore getting credited in the CAPE calculation for the index.

The following table shows constituents of the ISEQ 20 as of March 2014 alongside the constituents as of January 2007.

As you can see, there has been substantial turnover in the index. The current ISEQ 20 has one major commercial bank, The Bank of Ireland, which represents ~9% of the index’s total capitalization and 0% of the index’s current earnings. The ISEQ 20 of 2007, however, had three major commercial banks, which together made up ~40% of the index’s total capitalization and an even greater share of its earnings at the time.

The Shiller CAPE is a tool for detecting hidden value. During cyclical weakness, a company’s classic trailing-twelve month (ttm) P/E ratio will be abnormally elevated by temporarily depressed earnings, and will therefore give an inaccurate picture of the company’s future earnings potential. To get around this problem, we use the Shiller CAPE, which compares the company’s price to the average earnings that the company generated over the previous 10 years. The 10 year average of earnings gives a more complete picture of the earnings that the company can be expected to produce in the future, when conditions return to normal.

At the index level, the same logic applies. We compare the price of the index with the average of the index’s earnings over the previous 10 years, to get an accurate picture of the earnings that the index can be expected to produce when conditions return to normal. In this case, however, there’s a really big problem. The index has undergone a radical makeover. It’s not the same index anymore.

Conceptually, it doesn’t make sense to expect a normalization in Ireland’s economic condition to catapult the ISEQ’s earnings back to the levels seen from 2004 to 2008, when the ticking time bomb of a highly-leveraged banking system was the engine of profit growth. Of the three banks that made up the majority of the index’s earnings at the time, two are no longer in the index, and the other is an unrecognizable version of its former self, having undergone a massively dilutive recapitalization.

The Shiller CAPE: The Dilution Distortion

It turns out that there is an even more significant illusion being produced here. To illustrate the illusion, I’m going to present calculations of the Shiller CAPEs of individual companies in the Irish index. Note that the data, the majority of which is taken from GuruFocus, may contain minor errors, specifically related to the capitalization and share count of the companies, given how complex the changes have been since the crisis. Regardless, the calculations are adequate to illustrate the underlying process at play.

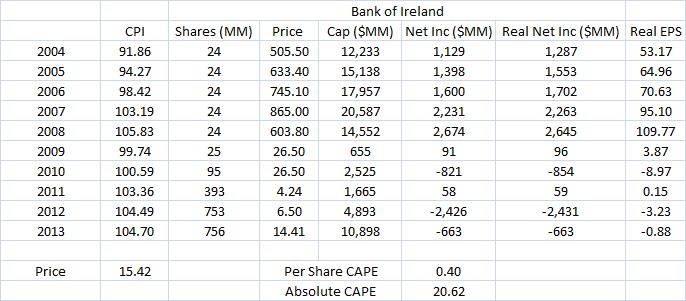

Consider the Bank of Ireland, whose CAPE calculation is shown in the table below:

Notice the column “Shares (MM).” As you can see, there’s been a huge explosion in the shares outstanding of the Bank of Ireland, obviously related to the massively dilutive recapitalization that the bank was forced to undergo in conjunction with the financial crisis.

Let’s think about how this dilution might impact the CAPE. In an extreme dilution, a company’s share price will fall by orders of magnitude–appropriately. In the case above, the price fell from over 900 to 15. In the CAPE calculation, the appropriately-collapsed price will be compared with the company’s past earnings per share, earnings that were earned when the share count was orders of magnitude smaller than it currently is. The dilution-depressed current price per share will thus get measured against an artificially inflated past earnings per share, a number that in no way reflects the company’s future earnings potential. Users of the metric will therefore walk away with a completely false picture of the company’s valuation.

It turns out that there is an additional illusion associated with the dilution. One would expect the crisis that caused the dilution to have produced a period of negative earnings that will get averaged into the Shiller CAPE, negating at least a portion of the artificial earnings excess of the boom. To be sure, in the case of the Bank of Ireland, those negative earnings did come through. Crucially, however, they were “registered” during the same reporting period as the dilution. The losses were therefore diluted over an artificially large number of shares, producing a relatively small per share loss (relative to the large per share gains that were enjoyed during the boom).

To make the point more clear, let’s get specific. To arrive at a per-share basis, the $1B to $2.5B that the Bank of Ireland earned each year in the pre-crisis period is being divided by the pre-dilution number of shares, approximately 24 MM. But then, after the crisis, the subsequent $4B loss is being divided by the post-dilution share count, a number ranging from 100 MM to 750MM. The result is what you see above. The Bank of Ireland appears to have earned $50 to $100 dollars per share per year during the boom times, and to then have lost only around $20 per share during the entirety of the bust. When you average these per-share numbers together to compute the average earnings, you get a deceptively high average, and therefore a deceptively low Shiller CAPE.

Now, to eliminate this distortion, what I’ve done in the table is calculate the CAPE on an absolute basis in addition to on a per-share basis. Instead of comparing the price per share to the average real earnings per share over the last 10 years, the “Absolute CAPE” compares the current market capitalization to the average real net income over the past 10 years, with both numbers unadjusted for share count. On this absolute basis, the CAPE for the Bank of Ireland rises from a ridiculously cheap 0.40 to a seemingly expensive 20.62.

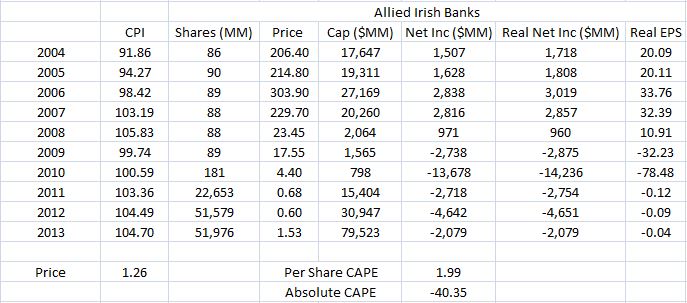

The same distortion emerges to an even greater degree in the case of Allied Irish Banks, whose CAPE calculation is shown in the table below:

Uncorrected for the dilutive distortion, Allied Irish shows a CAPE of 1.99. But the absolute CAPE is actually steeply negative, indicating that, on an absolute basis, the bank lost more money in the crisis than it earned during the boom. Is that surprising? It shouldn’t be–over the long-term, bubble-bust finance is not a good business. You eventually get completely wiped out.

There are similar distortions associated with the way in which troubled company’s tend to exit the index. Troubled companies often get delisted and removed from an index before all of their losses have been taken, allowing the index to escape from the losses scot-free, even though the corresponding gains were registered without hindrance. Worse yet, with some types of indices, even when the troubled company does remain in the index to register its losses, the publishers of the index don’t count the losses in the index earnings, because the losses represent one-time, non-recurring events.

I would have included a CAPE analysis of Anglo-Irish Bank, but they represent a prime example of an exit distortion, having been nationalized in 2009. From 2004 to 2008, they earned a profit typical of the other banks, on the order of around $1B per year. But then, in 2010, well after they had been nationalized and removed from the ISEQ, they took a cool $15B impairment loss, a loss that, if registered in the index, would have more than wiped out any profit that they contributed during the boom. How convenient. The ISEQ is able to count Anglo-Irish’s highly artificial profits earned during the boom, but then when the bust comes along, and it’s time for Anglo-Irish to drop its turd, the bank is already long gone from the index. Its turd gets dropped in a black hole, leaving the ISEQ’s earnings unaffected.

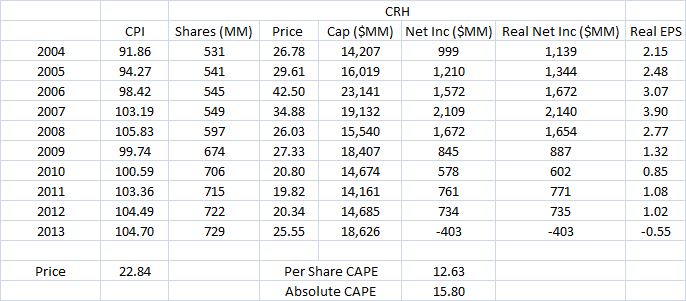

Now, let’s look at the CAPEs of some of the larger non-financial companies in the ISEQ. First, CRH:

As the table shows, there’s clearly some value in CRH. But it’s nothing to write home about. Notice that the company enjoyed the same dilutive effect that the banks enjoyed, albeit to a much smaller degree. The absolute CAPE is 3 points higher than the per share CAPE, owing to the fact that the share count has increased by almost 50% over the period.

CRH is easily the cheapest non-financial stock in the Irish stock market, and yet it’s CAPE isn’t even below 12. We should therefore be extremely suspicious when we see the Irish stock market as a whole register a CAPE below 10. Trivially, a country cannot have a CAPE lower than the CAPE of its cheapest current constituent. If it does, then something has necessarily gone wrong in the analysis.

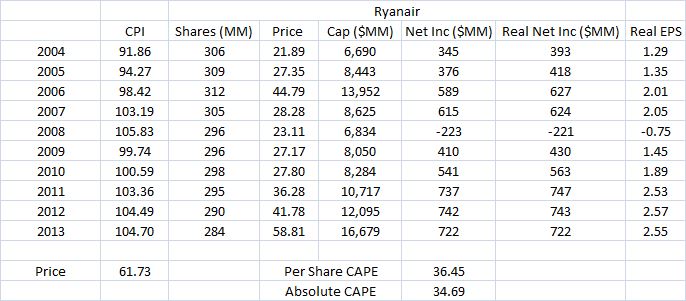

Here is the CAPE for Ryanair, Ireland’s premier airline, which makes up about 9% of the ISEQ:

Ryanair sports a CAPE of 36.45–hardly a case of deep value. Notice that its per share CAPE is actually higher than its absolute CAPE. The reason is that it’s been shrinking its shares, rather than growing them.

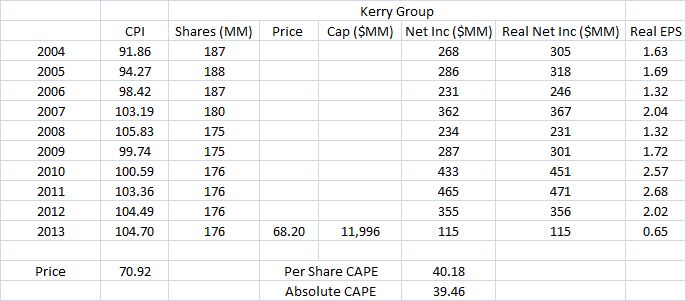

Here is the CAPE for Kerry Group, a food producer in the ISEQ:

Again, a very high CAPE, on par with the CAPE levels that you might see in a growing U.S. company. The per share CAPE is roughly the same as the absolute CAPE because there’s little change in the share count.

U.S. Banks: Similar CAPE distortions?

The U.S. banking sector is often cited as the cheapest sector of the U.S. equity market. It may be the cheapest sector–I’m not going to argue that point. But the CAPE should not be what leads us to this conclusion. The CAPE is not a conceptually valid way of measuring value in a post-crisis environment where share counts have appreciably changed.

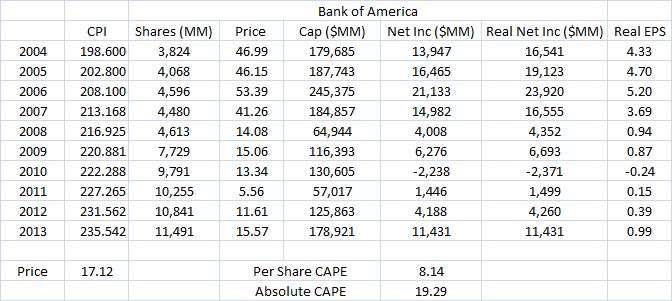

The same distortion that we saw in the CAPEs of the Bank of Ireland and Allied Irish is present in the CAPEs of America’s junky financial analogues. Consider, for example, the CAPE of Bank of America ($BAC), calculated below:

As you can see, $BAC suffered significant dilution in the crisis aftermath, simultaneous with its post-crisis writedowns, creating a distortion in its per share CAPE. The per share CAPE comes in at 8.14, when the absolute CAPE is 19.29.

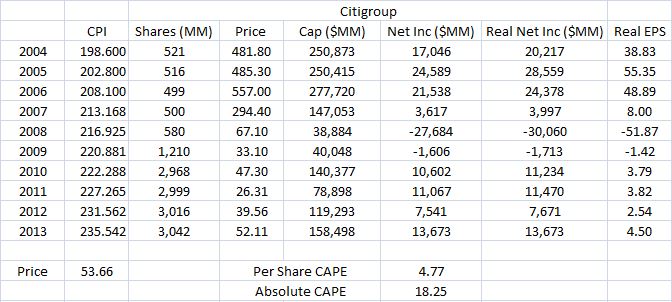

The following table shows the CAPE calculation for another junky financial, Citigroup ($C):

Again, the same distortion is present, to an even greater degree, given the greater dilution. The per share CAPE is 4.77, whereas the Absolute CAPE is 18.25.

Energy Companies: A More Benign Distortion

It turns out that the Shiller CAPE also creates distortions in the valuation of energy companies. The reason is that energy companies generate earnings off of a depreciating asset base. The appropriate way to value them is not to look at their past earnings, generated on assets that are now used up, but to conduct a discounted cash flow analysis of the future earnings that they will generate on their current asset base, as that base depletes away.

Consider, as an example, the case of Total, the integrated French oil company. The following table shows Total’s Shiller CAPE:

As you can see, Total trades at a very attractive CAPE relative to the market. It also trades at an attractive ttm P/E ratio–and always has. The reason that it trades at an attractive CAPE and ttm P/E ratio is that its past earnings are not directly relevant to its current value. What is relative to its current value is the ratio of its price to the discounted sum of its future earnings, earnings that will be generated as its finite oil reserves are drilled out of the ground and sold. How plentiful are those reserves? What is their quality? How expensive will drilling them out of the ground be? From a valuation perspective, these are the questions that matter.

The intrinsic value of an asset is the discounted sum of its future cash flows. If you have a company with recurring cash flows generated off of a surviveable asset base, then it makes sense to use trailing metrics like the CAPE, the ttm P/E ratio, and the ttm dividend yield to approximate the value. But if you have an energy company with an asset base that depletes every time product is pumped out and sold, an asset base that is difficult and costly to replace through new discovery, then these metrics will not provide an accurate picture of the value.

Discounted at 10%, the net present value of Total’s proven oil and gas reserves is $47B. The company trades at a market capitalization of $139B, with an enterprise value, including net debt, that is even higher. On those numbers, Total is hardly a case of deep value. To the contrary, it appears to be overvalued–by at least 200%. Before we jump to that conclusion, however, let’s consider a few points:

- 10% may be too large of a discount rate to apply to the assets in the present interest rate environment. Of course, lowering the discount rate won’t fully alleviate the apparent overvaluation. Even at a 0% discount rate, the net present value of Total’s oil and gas assets is only $105B (and that’s before the recent oil price drop).

- Total is an integrated company, and generates profit from refining and marketing in addition to production. The profits associated with its refining and marketing arms have to be included in the valuation analysis, just as its net debt has to be included.

- Proven reserves are often only a conservative estimate of the quantity of oil and gas that an energy company has access to and will be able to produce and sell over time. Given that the company trades at a 50% premium to its undiscounted proven oil and gas reserves, the market probably expects Total’s unproven reserves to be significant, possibly even larger and more valuable than its proven reserves.

The point, however, is that an analysis of the cash flow that will be generated out of Total’s current oil and gas assets, and not an analysis of the cash flow that it generated last decade, off of assets that have long since been converted into carbon dioxide, is what will determine the price that oil and gas investors will be willing to pay to own the company, and the price that they should be willing to pay. That’s why Total trades at depressed P/E and CAPE multiples. P/E and CAPE multiples simply are not relevant considerations in the oil and gas valuation process.

Reasons to Be Skeptical of European Value

If you examine the indices of the country’s in Europe that are allegedly offering investors deep value, you will notice that these indices are heavily allocated to financials and to energy as sectors. In cases such as Ireland where the indices are not heavily allocated to the financial and energy sectors, there’s little deep value to be found.

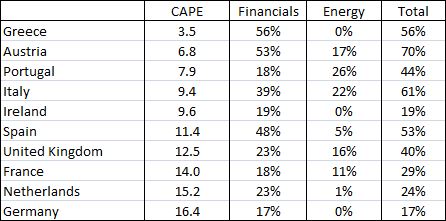

The following table shows the CAPEs of important European countries, borrowed from Star Capital’s fantastic interactive website, alongside the country allocations to the financial and energy sectors in the respective MSCI indices.

As we see, the countries have low CAPEs, but they also have lopsided allocations to the financial and energy sectors. In fact, there’s an apparent pattern: the higher the allocation to the financial and energy sectors–especially the financial sector–the lower the CAPE.

The heavy exposure to the financial sector substantially increases the risks of distortion, particularly given the credit bubble and subsequent crisis that Europe experienced. Greece, with a whopping 56% allocation to financials, and an unrecognizably low CAPE of 3.5, is particularly suspect in that respect. Where is its ultra-low CAPE coming from? My guess: not from healthy business selling at attractive prices, but from crashed-out zombie banks that are distorting the index.

Of all of the regions in the world, Europe offers what is clearly the worst fundamental backdrop for investment. The continent is overregulated, with inflexible labor laws and a generally business-unfriendly political climate, at least in certain countries. The continent’s household, corporate, and financial sectors are heavily-indebted. The population is in clear demographic decline. The different countries that make up the continent have different cultural and competitive dynamics, yet are all trapped in a single currency union. The exchange rates between the countries are therefore unable to naturally adjust so as to bring payment balances into line.

As if these structural headwinds weren’t enough, the monetary authority in Europe is a joke. It has no ability to do anything to stimulate the European economy except talk. The northern bloc won’t allow it to do anything more. How long have we been attending to these meetings, listening to Mario Draghi tell us about the things that he might one day do? At every meeting, the date of eventual action is pushed off to the next meeting, or beyond. Nothing ever happens.

Markets love monetary policy, but in truth, monetary policy has little to offer in a situation like this, where households and corporations are deleveraging, and where the population and the workforce are shrinking. In addition to supply-side labor reforms, what Europe needs is aggressive fiscal policy. Fiscal policy has the ability to directly and reliably increase aggregate demand. If aggregate demand is strong, real investment will start making economic sense (it doesn’t make economic sense right now). Real investment will therefore increase, creating new sources of employment and income, fueling further increases in aggregate demand, incentivizing additional real investment, and so on, in a virtuous cycle. For such a cycle to reliably take hold in a world that faces the kinds of headwinds that Europe faces, there needs to be an aggressive commitment on the part of policymakers to take whatever fiscal actions are necessary to keep aggregate demand strong–to intentionally and unapologetically run the economy hot, even if this means dropping freshly printed euros from a helicopter in the sky.

On that front, Europe could not possibly be worse off. The weaker countries that need aggressive fiscal stimulus have no ability to borrow in their own currencies. To conduct fiscal expansion, they have to get the permission of a separate country, Germany, a country with an obsessive fear of inflation and government debt, that does not have to share in any of their pains.

We can celebrate the fact that Mario Draghi said something, and that markets around the world rallied, but we should not let superficial price action blind us to the fact that the project of the Eurozone is an unsustainable mess. The union is going to have to eventually dissolve, or at least undergo a substantial makeover. Such a change is sure to bring turmoil to European financial markets, whether it comes next year, 5 years from now, or 20 years from now. European investors deserve to be appropriately compensated for the risk.

Are they being appropriately compensated? It’s not clear. From a Shiller CAPE standpoint, it looks like they are being compensated, but that’s likely to be a result of the high financial and energy sector exposures that European indices contain.

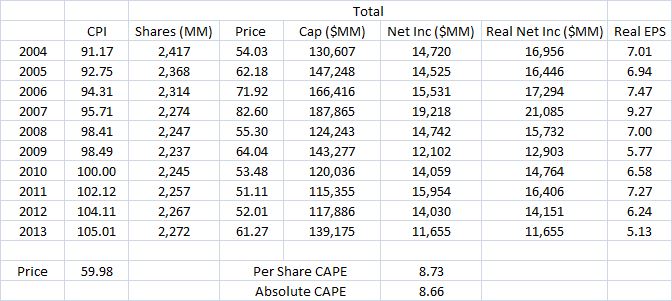

Interestingly, U.S. investors can find the “deep value” that allegedly exists in Europe right here at home, in their own backyards. All they have to do is go to the sectors that dominate European indices–financials and energy. If they want a low CAPE, they can buy low-quality U.S. banks that were forced to recapitalize in the credit crisis–$BAC and $C, for example–or large cap integrated oil companies that trade on the productivity of their underlying oil and gas assets, rather than on P/E ratios–$CVX and $XOM, for example. These companies sport Shiller CAPEs that are just as low as the deep value companies of Europe. There’s hardly a difference, for example, between the Shiller CAPE of a $BAC and that of a Banco Santander ($SAN), or the Shiller CAPE of a $CVX and that of an Eni Spa ($E). The numbers are essentially the same.

Solutions to the Problem

As a metric, the Shiller CAPE is still useful. It just needs to be employed with caution in countries that are coming out of large credit booms and busts, particularly those that have heavy exposure to financials, or that have had heavy exposure to financials in the past. I’m therefore going to conclude the piece with some proposals for how investors might be able to avoid, or at least work around, the CAPE distortions that these countries give rise to.

One way would be to get under the hood of the indices themselves–examining how they’ve changed over time, how much dilution has taken place, what specific crisis-related losses have and haven’t been counted in the earnings numbers, and so on–adding whatever adjustments may needed to allow for an accurate valuation analysis to take place. Unfortunately, this would be a difficult task. The data is hard to find, and would take a very long time to piece together.

Another approach would be to use indices that intentionally exclude financials, and possibly energy companies as well. Unfortunately, none of the major index publishers produce ex-financial or ex-energy indices–for Europe or for any country. Investors would have to build them directly, which would again be very complicated and time-consuming.

A more practical approach would be to evaluate the countries using ttm valuation measures, as a sort of “second check” on the Shiller CAPE metric. The ttm P/E ratio is often criticized for only providing a picture of the last twelve months. But that’s actually an advantage in this context, as it eliminates “The Ship of Theseus” problem. When you look at the ttm P/E ratio for an index, you can be sure that the “E” that you are looking at in the denominator is associated with the same companies as the “P” that you are looking at in the numerator. As we saw in the case of Ireland, you cannot always be sure of this fact when you use the Shiller CAPE on an index.

One good valuation metric to use, backed up by significant academic research, is the ttm enterprise value to ebitda (EV/EBITDA) ratio. The advantage of ttm EV/EBITDA is that it includes net debt, which should be part of any valuation analysis, and also that it eliminates many of the non-recurring non-cash charges that tend to distort earnings, particularly around recessions. The disadvantage, of course, is that it doesn’t count depreciation, and therefore it causes companies that have high depreciation costs, such as energy companies, to look artificially cheap.

If strictly non-cyclical measures are preferred, two additional ttm metrics that can be used to “second check” the Shiller CAPE are the ttm price to sales (P/S) ratio and the ttm price to book (P/B) ratio. Like the P/E and EV/EBITDA ratios, these metrics only look at the prior year, and therefore avoid the “Ship of Theseus” problem. At the same time, they solve the problem of cyclicality, given that sales and book values do not significantly fluctuate across the business cycle.

The problem with P/S and P/B ratios is that they tend to be different for countries that have different sectoral compositions. Naturally, countries with higher allocations to high margin and high ROE sectors will tend to exhibit higher P/S and P/B ratios than those dominated by low margin and low ROE sectors. We don’t necessarily want to penalize them for that in the analysis. Additionally, for the P/B ratio, not all countries writedown their assets using the same standards. European companies, for example, did not take the “goodwill” writedowns that U.S. companies took during the crisis. For that reason, their P/B ratios tend to be lower, as explained in this analysis from KPMG.

A clean way around this problem would be to normalize the P/S and P/B ratios of different country indices to reflect the different sectoral compositions that those country indices exhibit and to reflect an application of the same writedown accounting standards. Then, an apples-to-apples comparison between countries would become possible. Unfortunately, such a project would be too difficult and too time-consuming to put into motion.

When we check Ireland’s CAPE against its ttm P/S and P/B ratios, we quickly notice that our prior suspicions were correct: Ireland is not a case of deep value. The country trades at a P/B ratio of 2.3 and a P/S ratio of 1.4, both of which register as expensive in comparison with the rest of the globe. To be clear, Ireland may still be an attractive long-term investment opportunity–it probably is, given its many strengths–but the reason has nothing to do with its apparent status as deep value.

Fortunately, when we check the CAPE of the more-distressed PIIGS countries–Portugal, Italy, Greece, and Spain–against their respective P/S and P/B ratios, the countries continue to register as cheap. It’s probably true, then, that the countries represent deep value–specifically, deep value concentrated in the financial sector, and to a lesser extent, the energy sector. With respect to Greece, however, the P/B and P/S ratios, at 1.0 and 0.5 respectively, are not as cheap as would be expected given the 3.5 CAPE, which is almost half that of the closest competitor. Something is likely wrong with that number.

A final solution would be to not discriminate at all on the basis of country borders. If we’re looking for international value, let’s look for international value, in whatever country it happens to be located. By looking strictly at individual companies, we can eliminate the need for indices altogether, bypassing the “Ship of Theseus” problems they create.

On that theme, there are a number of well-run international ETFs that take valuation factors with solid historical track records and apply them in foreign markets to locate attractive individual company opportunities. Examples include (1) Cambria’s $FYLD, an international version of the successful $SYLD, which invests in companies that have a high shareholder yield, (2) Invesco’s $IPKW, an international version of the successful $PKW, which invests in companies that are buying back significant quantities of their own shares, and (3) Valueshares’ $IVAL, a not-yet-launched international version of the recently launched $QVAL, which invests in companies that exhibit attractive ttm EV/EBITDA ratios and that pass various quality screens.