In this piece, I’m going to show that the profit margin expansion seen in the U.S. corporate sector over the last two decades has been driven largely by gains in the financial and technology sectors. I’m then going to examine arguments for and against the sustainability of this shift.

Profit Margin Contributions By Sector

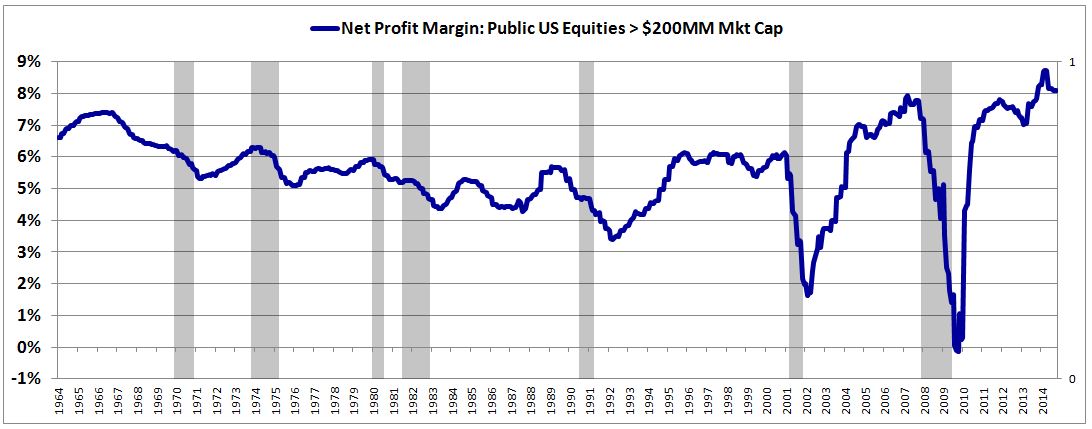

The following chart shows the aggregate net profit margin of publically-traded U.S. equities with market capitalizations greater than $200MM from January 1964 to October 2014. Recessionary periods are shaded in gray.

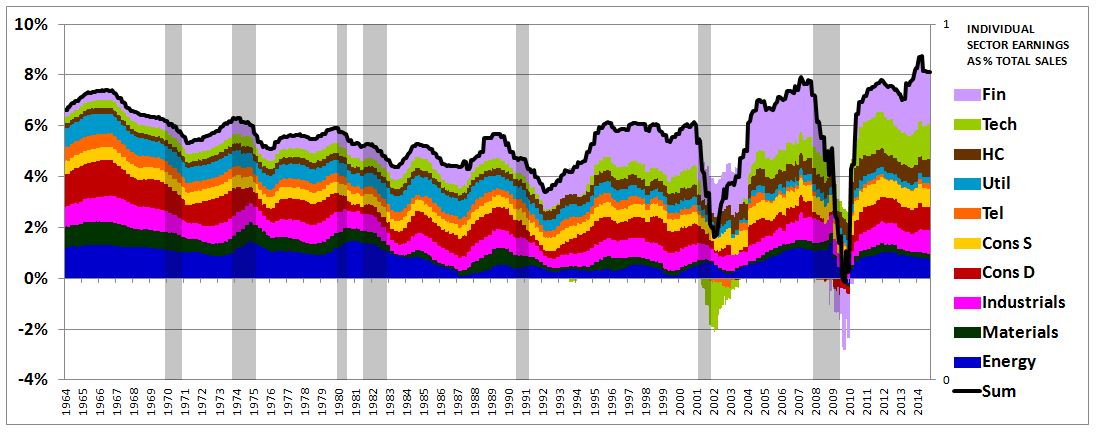

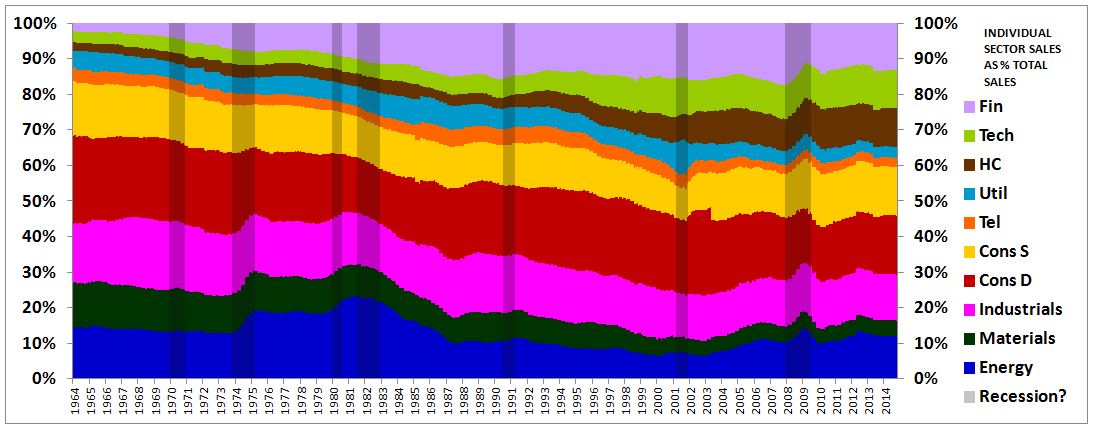

The next chart separates out the contribution to the aggregate profit margin by sector. For each sector, the colored area represents the individual earnings of the sector divided by the total revenues (sales) of all sectors. Note that the sum, the black line, is just the aggregate profit margin shown in the previous chart.

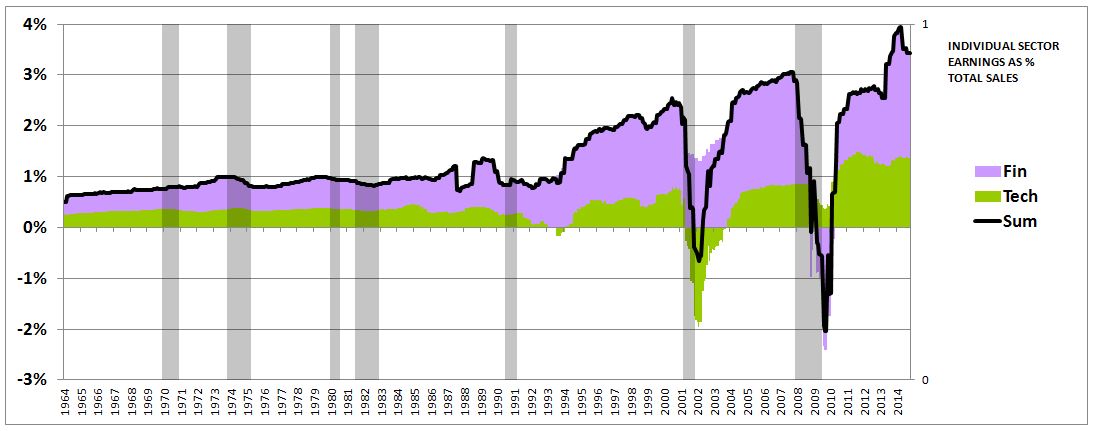

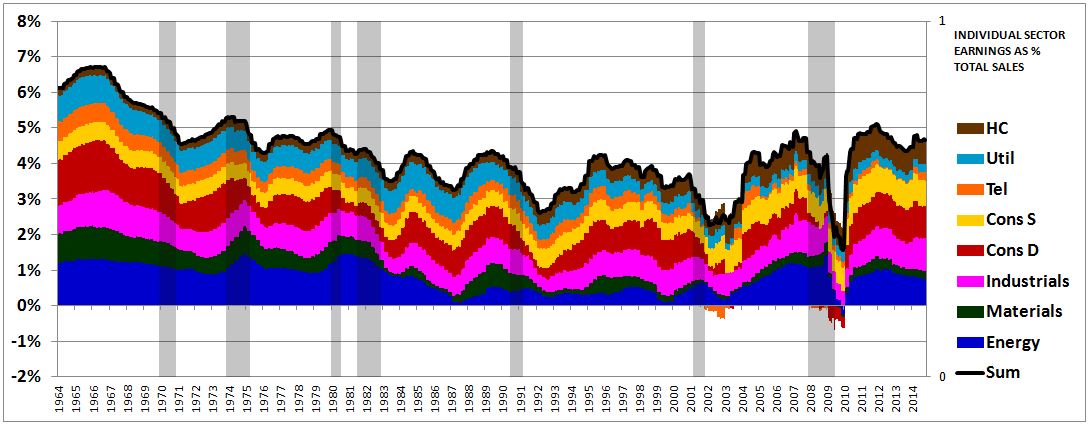

Notice the rising contribution from the financial sector (light purple) and the technology sector (olive green), and the falling contribution from the other sectors in aggregate:

In January of 1964, financial and technology sector earnings contributed 0.49% to the aggregate profit margin, which was 6.60% at the time. Today, they contribute almost seven times that amount, 3.42%, to an aggregate profit margin of 8.09%.

Changes in Sectoral Revenue Contributions

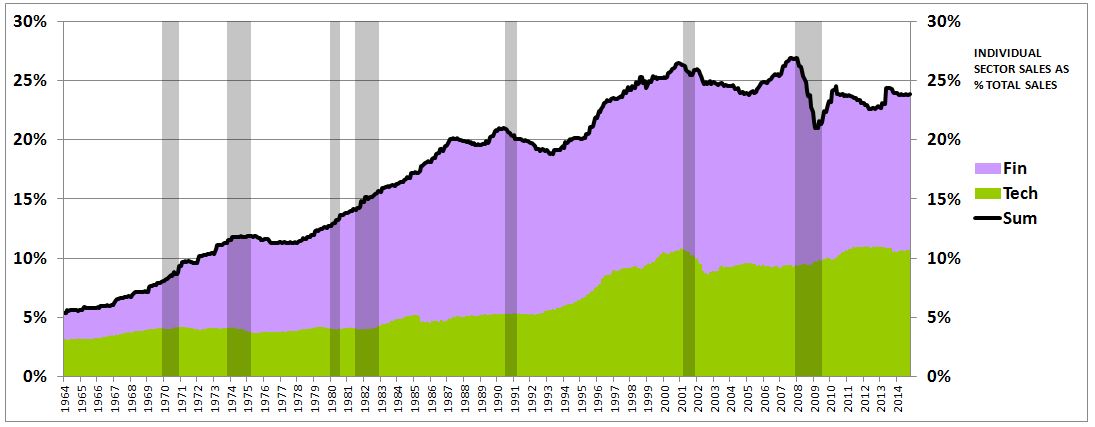

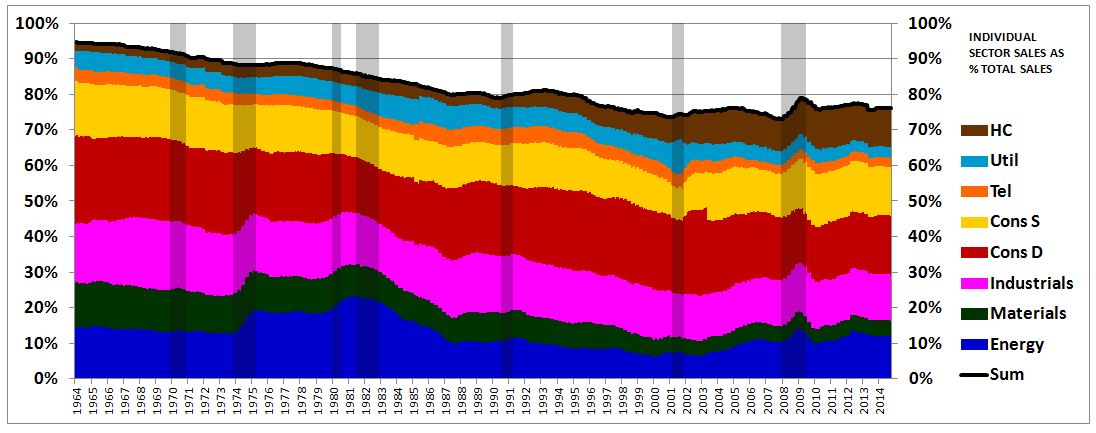

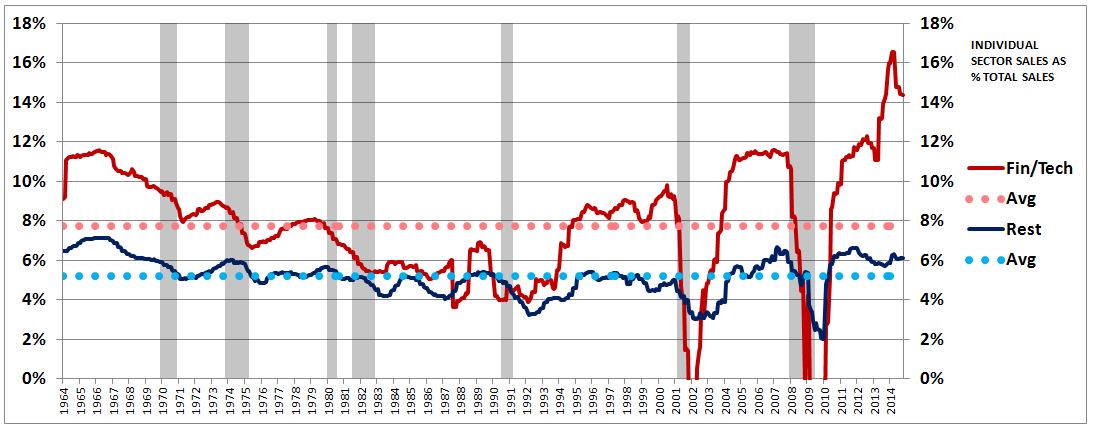

A better way to think about what has happened here is to think in terms of sectoral revenue contributions: revenues of individual sector as a percentage of the total revenue of all sectors. The following chart shows the evolving revenue contributions of each sector, from January of 1964 to October of 2014.

As the chart illustrates, the revenue contribution of the combined financial and technology sectors–the amount of total revenues that are revenues from those sectors–has increased substantially over time. In January of 1964, the revenue contribution was 5.41%. Today, it is 23.83%–almost a quarter of the total.

This change in revenue contribution matters because technology and financial sector revenues tend to be earned at higher profit margins than the revenues of other sectors: historically, 7.74% for technology and finance, versus 5.19% for the rest. And so if the revenue contribution from the financial and technology sectors has increased, then we should expect the “normal” profit margin of the aggregate corporate sector–if there is such a thing–to have increased as well. The targeted “mean” in a “mean reversion” will have shifted upward, rendering the ensuing picture less bearish.

(Note: the revenue contribution of healthcare, shown in brown, has also increased substantially over time. But, to the surprise of many, current healthcare profit margins, at 6.2%, are below their own historical average, and only slightly above the historical average of the aggregate corporate sector. They are not appreciable contributors to current profit margin elevation).

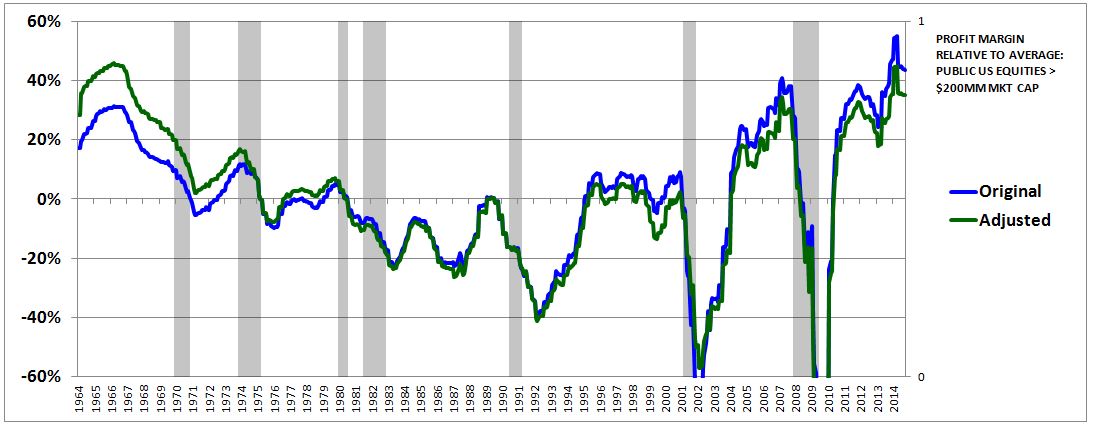

It turns out that we can correct for this shift, creating an “adjusted” profit margin that accounts for the effects of changing sectoral revenue contributions. What we need to do is take the average historical revenue contribution of each sector, and compute what the aggregate profit margin would have been, at each point in time, if each contribution had been equal to its individual historical average.

The following table shows the historical average revenue contributions of each of the 10 GICS sectors:

So, historically, energy revenues have represented 12.78% of total revenues, materials revenues have averaged 7.80%, health care revenues have averaged 5.46%, and so on. What we want to know is, what would the profit margin of the aggregate corporate sector have been at each point in history if the revenue contribution of each individual sector had been equal to its average? This “adjusted” profit margin will filter out changes that have been driven solely by shifts in sector size and contribution, and will thus provide a more accurate picture of the aggregate profit margin to use when making historical comparisons.

At this point, Bulls are probably hoping that I pull out a chart showing that when profit margins are properly adjusted in this way, that they end up not being historically elevated. Sorry, not quite. As the chart below shows, the adjustment doesn’t make much of a difference.

The unadjusted profit margin (blue) is 45% above its historical average, versus 35% for the adjusted profit margin (green). Relative to the respective averages, the adjusted profit margin is only about 10% “less elevated” than the unadjusted profit margin. This difference is worth something, no question–but it’s not enough to eliminate profit margin concerns outright.

The reason that the adjustment doesn’t make the kind of difference that we might otherwise expect is that the profit margins of the financial and technology sectors have themselves expanded dramatically in recent years. The truth is that profit margin increases within the financial and technology sectors, rather than increases in their contribution to total revenue, have been the primary drivers of the aggregate profit margin increase.

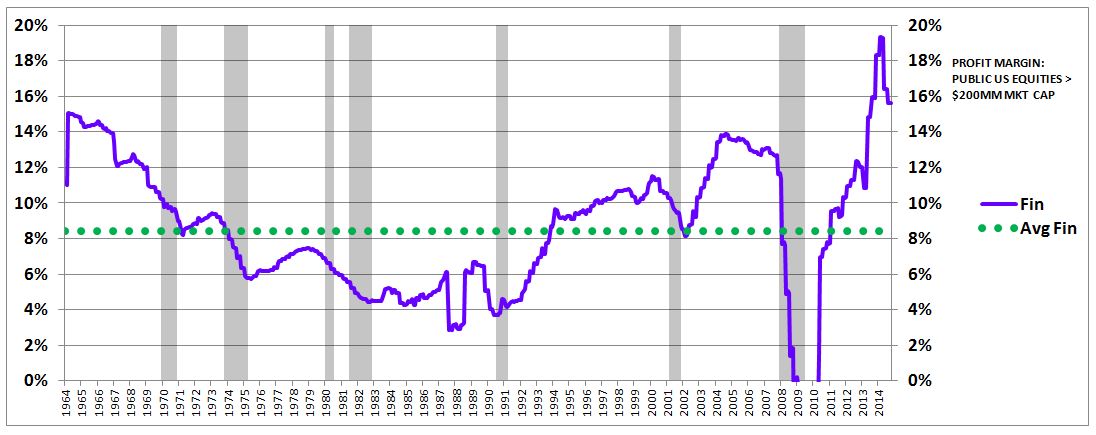

The following chart shows the profit margins of the combined finance and technology sectors (red) alongside the profit margins of the combined other sectors (blue):

As you can see, profit margins in finance and technology have exploded. Combined, they are running at almost twice their historical averages–86% above, to be precise. The profit margins of the combined other sectors are hardly elevated at all–only around 18% above their historical averages.

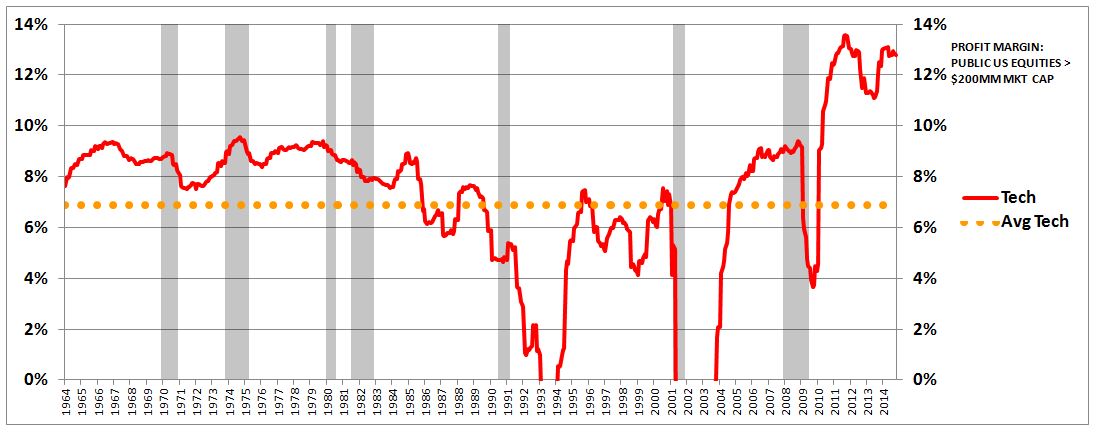

The following charts show the profit margins of the finance and technology sectors individually:

Notice that a large chunk of the move is recent–a phenomenon unique to this specific cycle–especially in the technology sector.

Explaining the Rise

It goes without saying that finance and technology, which together represent over 42% of current U.S. corporate earnings, are two sectors that we should keep a close eye on going forward. Changes within them have driven the profit margin expansion of the last several years, which itself has driven the bull market, having made possible a “goldilocks” scenario in which earnings have been able to grow robustly despite slow top-line growth and almost non-existent inflation. The slow top-line growth and almost non-existent inflation has pushed the Fed into an aggressively easy monetary stance that has served as fuel for persistent P/E multiple expansion, with more and more investors ditching the misery of zero-yield cash and bonds to join the market advance.

The finding that the profit margin expansion has been driven largely by changes inside the finance and technology sectors sheds doubt on other stories that have been offered as explanations. Weaker labor unions, increased access to cheap foreign workers, a rise in earnings taken in from abroad, lower corporate taxes, more effective corporate tax avoidance schemes, and so on–these explanations fail to make sense of the fact that profit margins haven’t increased nearly as much in sectors outside of finance and technology. Whatever the correct explanation for the current state of profit margins ends up being, it needs to be one that applies with some preference to finance and technology, which is where the most dramatic shift has taken place.

What, then, is the explanation for the rise? Why have profit margins in finance and technology increased so dramatically over the last several years? Will the increase hold up?

A Bullish Angle

On the finance front, bulls can make a compelling argument that the financial sector’s contribution to the profit margin increase is likely to be sustained. The increase in the financial sector share of total revenues has been driven by higher debt levels across the economy–that change will almost certainly prove to be secular. At the same time, the increase in profit margins within the financial sector has arguably been driven by the drop in short-term interest rates (funding costs for financial institutions), which is a change that is also likely to be secular. Note that the last time that financial profit margins were at their current levels was in the early 1960s, when short-term interest rates were low. The Fed tightening cycle that lasted from the late 1960s through the 1980s seems to have been what pulled them down, as they fell much more precipitously during that period than the profit margins of any other sector. They only began to regain their prior levels in the mid-to-late 1990s, as the Fed shifted to an easier monetary stance.

On the technology front, bulls can make a similarly compelling argument that the revolutionary technology of the information economy, which has only been fully fleshed out in the last decade, has been the game-changer, having created an increasingly “winner takes all” environment in which it has become more and more difficult for potential new entrants to credibly compete with the first-mover. If they are right, then profit margin mean reversion–in the technology sector and in any other sectors that manage to piggy back on the dynamic–would seem to be less likely.

A Bearish Angle

Of course, bears can offer compelling counter-arguments to this optimism. On the finance front, they can point to the fate of the yield curve–which, assuming the Fed follows through on its normalization plans, does not look good.

When the Fed cuts rates for the first time, the long end of the curve usually stays put. People continue to expect an eventual return to normalcy, and price the long end accordingly. The result ends up being a steep curve that boosts financial sector profit margins. But when the Fed cuts rates and keeps them cut, for a period that seems to drag on forever, because the economy never seems to get hooked into the kind of genuine inflationary expansion that would justify a tightening cycle, the market eventually figures things out. Investors realize that long-term rates need to be lower, and pulls the long-end down accordingly, at the expense of financial sector profitability.

Eventually, the Fed will raise the short-end–if not simply out of a desire to restore some normalcy to monetary policy. When that time comes, the long end will again be slow to respond–this time slow in the opposite direction, slow to rise, given the anchoring and inertia of market participants who, by then, will have grown accustomed to the idea of secularly low interest rates. The result will be a yield curve that gets flatter and flatter with each hike, and a financial sector whose profit margins get squeezed. That seems to be exactly where we are currently headed, and it is not bullish.

In the most recent earnings data from banks, we’ve seen a consistently weak trend: flat YOY revenue growth and negative YOY EPS growth, brought on by increased competition, particularly among smaller banks, increased regulatory expenses, and reduced profitability due to a flattening yield curve. Loan growth, which would otherwise represent the bright spot, is not making up for the reduced profitability.

On the technology front, bears can make a similarly compelling argument. “Tech” is the most cutthroat and competitive of all sectors. Historically, it has produced subpar returns for investors (ranked number 6 out of 10 sectors), likely due to the way in which disruption and competition have worked to break down dominant positions within it. When we look at the seemingly impenetrable empires of the $AAPLs and $GOOGs and $MSFTs and $FBs of the world, it can be tempting to think that the truly massive levels of profitability they currently enjoy will be forever secure–but this kind of thinking is not supported by history.

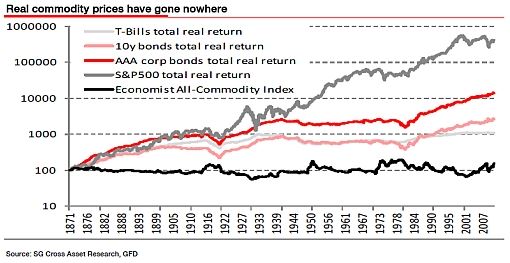

There’s a particularly interesting and relevant analogy that bears can raise in this context, one that involves a different sector: commodities. The historical evidence on the real return potential of spot commodities is overwhelming: there is no real return potential, spot commodities do not offer real returns. For proof, consider the following 130 year chart from Dylan Grice. Notice the black line languishing stupidly at the bottom:

But then again, over the last decade, we saw a massive boom in commodity prices around the world. As always happens, compelling stories emerged to explain why the boom had occurred and why it would almost certainly hold up–insatiable demand growth from China, India, and other emerging markets, an increasingly constrained supply that fails to grow, even in response to large price increases, and so on. If you had told people in 2007 or 2008, or in 2010 or 2011, that these were just stories, and that there would eventually be a painful reversion to the mean just a few years later, very few people would have taken you seriously. Nobody in the commodity complex at the time was seriously entertaining the possibility.

But now here we sit, in a healthy economic expansion, with oil trading below $45 (!!), the same inflation-adjusted price that it traded at 30 years ago, near the lows of the last oil downturn. A 30 year period of zero real returns for this and other spot commodities has once again vindicated the apparent lesson of history: that spot commodities do not produce real returns. Now, to be clear, I don’t expect profit margin bearishness to receive the same degree of vindication–but some caution and humility are certainly in order, given the possibility.