“You know, Paul, Reagan proved that deficits don’t matter. We won the mid-term elections, this is our due.”

“You know, Paul, Reagan proved that deficits don’t matter. We won the mid-term elections, this is our due.”

— Vice President Dick Cheney defending a second round of tax cuts against the objection of Treasury Secretary Paul O’Neill, shortly after the 2002 mid-term elections.

Over the last two decades, the Japanese economy has failed to generate healthy levels of inflation. Some might wonder why that’s a problem. It’s a problem because healthy inflation is the only reliable indication that an economy is fully utilizing the labor and capital resources available to it. The fact that Japan has had no inflation, or has even deflated, confirms that it has been operating below its potential, at the expense of the living standards of its population.

What should Japanese policymakers do to restore inflation to healthy levels? This question is extremely important, not only for the economic future of Japan, but for the economic future of the entire world. The causes of persistently weak inflation in Japan aren’t entirely understood, but it’s possible–and likely–that they are tied to the effects of slowing population growth, aging demographics, and a growing scarcity of worthwhile investment opportunities, ways to add real value to the economy by creating new capacities that consumers will genuinely benefit from and be eager to spend their incomes on. If that’s the case, then the entire world will eventually face the problems that Japan currently faces, as the entire world is on Japan’s demographic and developmental path.

For the past 2 years, Japanese policymakers have attempted to use unconventional monetary policy to stimulate inflation. The Bank of Japan (BOJ) has set an explicit 2% target for the inflation rate, and has effectively promised to purchase whatever quantity of assets it needs to in order to bring the inflation rate to that target. Unfortunately, asset purchases don’t affect inflation, and so the BOJ has essentially been wasting everyone’s time. In terms of the actual data, the policy has been a clear failure, with core Japanese YOY CPI running at a pathetic 0%, despite a two-year doubling of Japan’s already enormous monetary base.

The solution for Japan, and for any economy that is underutilizing its resources, is to implement an inflation targeting policy that is fiscal rather than monetary–what we might call “Fiscal Inflation Targeting.” In Fiscal Inflation Targeting, the legislature sets an inflation target–e.g., 2% annualized–and gives the central bank the power to change the rates on a broad-based tax–for example, the lower brackets of the income tax–as needed to bring inflation to that target. To address scenarios in which inflation chronically undershoots the target, the central bank is given the power to cut tax rates through zero, to negative values, initiating the equivalent of transfer payments from the government to the private sector. Crucially, any tax cuts or transfer payments that the central bank implements under the policy are left as deficits, and the ensuing debt is allowed to grow indefinitely, with the central bank only worrying about it to the extent that it impedes the ability to maintain inflation on target (via a mechanism that will be carefully explained later). Note that other macroeconomic targets, such as nominal GDP (nGDP), can just as easily be used in lieu of inflation.

A policy of Fiscal Inflation Targeting would be guaranteed to achieve its stimulatory goals. In terms of direct effects, tax cuts and transfers directly increase nominal incomes, and there is no level of inflation that cannot be achieved if nominal incomes are broadly increased by a sufficient amount. In terms of indirect effects, having such a powerful tool to use would dramatically increase the economic impact of the central bank’s communications. On the current approach, to stimulate at the zero lower bound, the central bank is limited to the use of balance sheet expansion, which works primarily by placebo, if it works at all. But in Fiscal Inflation Targeting, the central bank would have the equivalent of real drugs to use. Economic participants would therefore have every reason to trust in its power, and to act as if its targets would be consistently met.

The insight that fiscal policy should be used to manage inflation, in the way that monetary policy is currently used, is not new, but was introduced many decades ago by the founders of functional finance, who were the first to realize that inflation, and not the budget, is what constrains the spending of a sovereign government. Advocates of modern monetary theory (MMT), the modern offshoot of functional finance, notably Scott Fulwiller of Wartburg College, have offered policy ideas for how to implement a fiscally-oriented approach.

My view, which I elaborated on in a 2013 piece, is that the successful implementation of any such approach will need to involve the transfer of control over a portion of fiscal policy from the legislature and the treasury to the central bank. Otherwise, the implementation will become mired in politics, which will prevent the government’s fiscal stance from appropriately responding to changing macroeconomic conditions.

There are concerns that such a policy would be unconstitutional in the United States, since only the legislature has the constitutional authority to levy taxes. But there is no reason why the legislature could not delegate some of that authority to the Federal Reserve in law, in the same way that it delegates its constitutional authority to create money. In the cleanest possible version of the proposal, the legislature would pass a law that creates a special broad-based tax, and that identifies a range of acceptable values for it, to include negative values–say, +10% to -10% of earned income below some cutoff. The law would then instruct the Federal Reserve to choose the rate in that range that will best keep inflation on target, given what is happening elsewhere in the economy and elsewhere in the policy arena.

Ultimately, the chief obstacle to the acceptance and implementation of fiscal inflation targeting is the fear that it would lead to the accumulation of large amounts of government debt. And it would, particularly in economies that face structural weakness in aggregate demand and that require recurrent injections of fiscal stimulus to operate at their potentials. But for those economies, having large government debt wouldn’t be a bad thing. To the contrary, it would be a good thing, a condition that would help offset the weakness.

The costs of large government debt accumulation are not well understood–by lay people or by economists. In this piece, I’m going to try to rigorously work out those costs, with a specific emphasis on how they play out. It turns out that there is currently substantial room, in essentially all developed economies that have sovereign control over credible currencies, to use expansive fiscal policy to combat structural declines in inflation, without significant costs coming into play.

The reader is forewarned that this piece is long. It has to be, in order to make the mechanisms fully clear. For those that want a quick version, here’s a bulleted summary of the key points:

- Government debt accumulation increases the net financial wealth of the private sector. (Note: for convenience, from here forward, we will omit the “net” term, and use the terms “net financial wealth” and “financial wealth” to mean the same thing).

- Increases in financial wealth can lead to increases in spending which can lead to increases in inflation. The effects need not be immediate, but may only show up after conditions in the economy have changed such that the economy’s wealth velocity–the speed at which its total stock of financial wealth “circulates” in the form of expenditures–and its wealth capacity–its ability to store financial wealth without overheating–have risen and fallen respectively.

- From a policy perspective, the way to reduce an economy’s wealth velocity and increase its wealth capacity is to raise its interest rate. But when government debt is overwhelmingly large, interest rate increases tend to be either destabilizing or inflationary, depending on how the government funds the increased interest expense that it ends up incurring.

- The countries that are the best candidates for fiscal inflation targeting are those that have structurally high wealth capacities–those that are able to hold large amounts of financial wealth without overheating, and that are likely to retain that ability indefinitely into the future. Examples of such countries include the United States, Japan, the U.K., and the creditor countries of the Eurozone.

The piece is divided into two parts. I begin the first part by specifying what counts as a “cost” in an economic policy context. I then examine four myths about the costs of large government deficits: (1) That there can be no free lunch, (2) That large government deficits are unsustainable, (3) That large government deficits cause interest rates to rise, and (4) That large government deficits are necessarily inflationary.

In the second part, I explain the mechanism through which fiscal inflation targeting, and any policy approach that generates exceedingly large quantities of government debt, can sow the seeds of a future inflation problem. I begin by introducing the concept of “wealth velocity”, which is a modification of the more economically familiar term “money velocity”, and “wealth capacity”, which is a concept analogous to “heat capacity” in thermodynamics. I then explain how changes in wealth velocity and wealth capacity over time can cause a stock of accumulated government debt that wasn’t inflationary to become inflationary, and how the the ability of monetary policy to appropriately respond can be curtailed by its presence. I conclude the piece with a cost-benefit analysis of fiscal inflation targeting, identifying the countries in the world that are currently the best candidates for it.

Functional Finance and “Costs”: A Focus on the Well-Being of Persons

Suppose that to keep the economy on a 2% inflation target, a government would have to run a large deficit–say, 10% of GDP–in perpetuity. What would the cost of perpetually running such a deficit be? Answer: the eventual accumulation of a large quantity of government debt. But this answer begs the question. What is the cost of accumulating a large quantity of government debt? Why should such an accumulation be viewed as a bad thing? What specific harm would it bring?

To speak accurately about the “cost” of large government debt, we need to be clear about what kinds of things count as real costs. To that end, we borrow from the wisdom of the great economist Abba Lerner:

“The central idea is that government fiscal policy, its spending and taxing, its borrowing and repayment of loans, its issue of new money and its withdrawal of money, shall all be undertaken with an eye only to the results of these actions on the economy and not to any established traditional doctrine about what is sound or unsound. This principle of judging only by effects has been applied in many other fields of human activity, where it is known as the method of science as opposed to scholasticism. The principle of judging fiscal measures by the way they work or function in the economy we may call Functional Finance.” — Abba Lerner, “Functional Finance and the Federal Debt”, 1943.

In the context of economic policy, a real cost is a cost that entails adverse effects on the well-being–the balance of happiness and suffering–of real people, now or in the future. A good example of a real cost would be poverty brought on by unemployment. Poverty brought on by unemployment entails concrete suffering for the afflicted individuals.

Another good example of a real cost would be hyperinflation. Hyperinflation represents a nuisance to daily life; it undermines the enjoyment derived from consumption, forcing consumers to consume because they have to in order to avoid losses, rather than because they want to; it creates an environment in which financially unsophisticated savers end up losing what they’ve worked hard to earn; it makes contractual agreements difficult to clearly arrange, and therefore prevents economic parties from engaging in mutually beneficial transactions; it retards economic growth by encouraging allocation of labor and capital to useless activities designed to protect against it–e.g., precious metal mining. Each of these effects can be tied to the well-being of real people, and therefore each is evidence of a real cost.

In contrast, “not having our fiscal house in order” or “owing large amounts of money to China” or “passing on enormous debts to our children” are not real costs, at least not without further analysis. They don’t, in themselves, entail adverse effects on the well-being of real people, now or in the future. Their rhetorical force comes not from any legitimate harms they cite, but from their effectiveness in channeling the implied “moral guilt” of debt accumulation–its connection to short-termism, hedonism, selfishness, impulsiveness, recklessness, irresponsibility, and so on. In that sense, they are like the prevailing rhetorical criticisms of homosexuality. “But that’s gross!” is not a valid objection to consensual love-making activities that bring happiness to the participants, and that cause no harm to anyone else. Similarly, “But we’re spending money we don’t have” is not a valid objection to fiscally expansive policies that improve the general economic well-being without attaching adverse short or long-term economic consequences.

None of what is being said here is meant to deny, off the bat, that large government debt accumulation can bring adverse economic consequences. It certainly can. But to be real, and to matter, those consequences need to involve real human interests–they can’t simply be empty worries about how a government’s finances are “supposed to be” run.

Myth #1 — There Can Be No Free Lunch

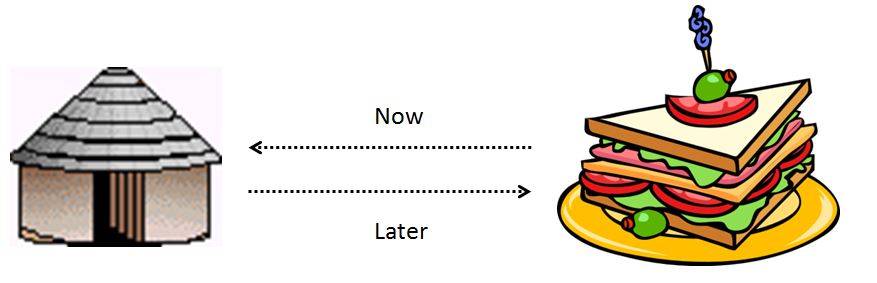

Imagine a primitive, specialized economy that trades not in money, but in promises. You are skilled at making food, and have extra leftovers from your recent meal to share; I am skilled at construction, and can build shelter–a hut–for you. Your present hut is currently adequate, but it will eventually fall apart and need to be rebuilt. So we make a deal. I will rebuild your hut, on your request, and, in exchange, you will give me your leftover food.

Importantly, there’s a time lag between the delivery of my end of the deal and the delivery of your end. You have food right there, ready to give, and I am ready to take it, now. But the rebuilding of your hut is only going to take place later, when the need arises. It follows that in this trade, an actual good–food, right here in front of both of us–is being exchanged for a potential good, a promise to do something at some point in the future, on request.

Now, let’s suppose that my appetite for food is enormous, and that I enter into similar deals with other people, in order to get food from them. As I go on accumulating more and more hut-building debt, I think to myself, “This is great. I can eat as much as I want, and I don’t have to actually do any work.” Using this tactic, will I be able to secure a “free lunch” for myself–literally, a lunch that I will never have to repay?

The obvious answer is no. The people that are accepting my promises as compensation aren’t idiots. They are accepting them in order to one day use them. If I issue more promises than I can reasonably make due on, then when the owners of those promises eventually come to me wanting to use them, wanting me to rebuild their huts, I’m not going to be able to deliver what I owe. I won’t have sufficient time or resources to rebuild the shelters of all of the people that I’ve made promises to. That’s where the perceived “free lunch” will fall apart. For some, my lunches won’t have been free lunches–they will have been stolen lunches, lunches that I wrongly took without the prospect of repayment, and that I am sure to be retaliated against for having taken.

Our natural inclination is to extend this intuition to the operation of specialized economies that trade in money. Suppose that there is a disabled homeless man that cannot find gainful employment, a way to contribute. It’s not his fault–his circumstances are such that there just isn’t anything useful that he can do for anyone, no value that he can add to anyone’s life that would make anyone want to pay him anything. That said, he has certain needs–food, shelter, clothing, medical attention, and so on. From a general humanitarian perspective, we want those needs to be met.

As a society, how might we ensure that his needs are met? The “fiscally honest” way would be to require anyone that earns income to give a portion of that income to the government through taxes, and to then have the government disburse the proceeds to him, and to others like him, to spend on basic necessities. In imposing this requirement, we would be confiscating a portion of their potential consumption, which they’ve earned through their productive contributions, and which they own in the form of the money they are holding, and transferring that consumption to him.

But is that the only way to ensure that his needs are met? What if instead of taking money from income earners, and giving it to him and to others like him, we were to simply create new money–print it up from nothing? In printing new money and giving it to him, we would be giving him the ability to purchase the things he needs, without having to take away anyone else’s money–the undesirable part of the process that we would surely avoid if we could.

Our prior intuition, that there are no free lunches, enters the picture here, and causes us to search for a hidden cost in the approach–a consequence that we haven’t properly acknowledged or accounted for. Surely, things can’t be that easy, that we would be able to use money creation to entirely circumvent the need to actually part with the things that we give away to others. In terms of what that cost actually is, we normally assume it to be inflation. In creating new money and spending it, we reduce the value of existing money. In this way, we take wealth from those that are holding it in the form of money, and transfer it to those that aren’t.

But there’s a mistake in this thinking. The seeds of the mistake were identified long ago, by two philosophers who are far more famous for other ideas: the British philosopher David Hume and the German philosopher Arthur Schopenhauer.

Beginning with Hume,

“It is also evident, that the prices do not so much depend on the absolute quantity of commodities and that of money, which are in a nation, as on that of the commodities, which come or may come to market, and of the money which circulates. If the coin be locked up in chests, it is the same thing with regard to prices, as if it were annihilated; if the commodities be hoarded in magazines and granaries, a like effect follows. As the money and commodities in these cases never meet, they cannot affect each other.” — David Hume, Essays, Moral, Political, Literary, “Of Money“, 1741

Hume’s point was that a simple increase in the stock of money is not enough to cause an increase in prices. To be inflationary, increases in the money stock have to lead to increases in spending. If they do not lead to increases in spending, then they will not affect the balance of supply and demand–the balance that determines the trajectory of prices.

Schopenhauer summed up the second seed of the mistake in the following quotes:

“People are often reproached because their desires are directed mainly to money, and they are fonder of it than of anything else. Yet it is natural and even inevitable for them to love that which, as an untiring Proteus, is ready at any moment to convert itself into the particular object of our fickle desires and manifold needs. Thus every other blessing can satisfy only one desire and one need; for instance, food is good only to the hungry, wine only for the healthy, medicine for the sick, a fur coat for winter, women for youth, and so on. Consequently, all these are only relatively good. Money alone is the absolutely good thing because it meets not merely one need considered concretely, but all needs considered abstractly.” — Arthur Schopenhauer, The World as Will and Representation, Volume I, 1818.

“Money is human happiness in the abstract: he, then, who is no longer capable of enjoying human happiness in the concrete devotes his heart entirely to money.” — Arhtur Schopenhauer, Counsels and Maxims, 1851.

The mistake is to assume that anyone who exchanges the output of her time, labor, and capital for money does so because she eventually wants to use that money to consume the output of the time, labor, and capital of someone else. If money had no value outside of its use in consumption, then this assumption might make sense. It would be irrational for an individual to work for money that she wasn’t ever going to spend–she would essentially be working for free. But in an economic system where money is the primary mode of trade, it acquires intangible value–value unrelated to the actual purchase of any concrete good or service. It comes to represent abstract, psychological goods: happiness, accomplishment, success, optionality, ability, power, safety, security, status, respect, and so on. A person may have accumulated enough of it to meet her actual future consumption needs many times over, but she will still seek more of it, in pursuit of those goods.

Suppose that Warren Buffet were to make a series of bad investments that were to cause the monetary market value of his wealth–currently, $72.3B–to permanently shrink by 99.9%, leaving “only” $72.3MM to his name. The loss would not in any way affect his consumption or the consumption of his heirs, for neither he, nor they, are likely to put either amount to consumptive use. But still, he would be extremely upset by it, and would go to great lengths to avoid it. Why? Because money holds intangible value to him, value that is unrelated to its actual use in funding his current and future consumption expenditures.

Behaviorally, he has been trained, from his youth, his days as a much poorer man, to respect money, and to never let it be wasted or left on the table. It is something that is supposed to be cared for, nurtured, grown over time–not shrunk. To lose so much of it would therefore be frustrating and unpleasant for him, even if the loss made no difference to his lifestyle.

Why does Buffet care about money? What value does it bring him?

- Success, Achievement, Scorekeeping. Money is the way that success and achievement are measured, kept score of–in Buffet’s case, success and achievement at the game of investing, a game that he enjoys playing, and that he wants to win at. Money is the reward that makes investing a serious game, a game of real significance, that brings pleasure when played well.

- Power, Freedom. The knowledge that he can do and have any possible thing that he wants, whenever he wants it, in whatever quantity he wants it–up to infinity. That knowledge brings satisfaction, even if the underlying capacity will never be put to use.

- Safety, Security. The knowledge that his wants and needs will never go unmet, that his standard of living, and those of the people he cares about, will never fall to unwanted levels, that the causes he believes in will always have an able advocate in him. That knowledge makes it easier for him to enjoy the things that he actually does partake in, removing the possibility–and therefore the fear–that his ability to partake in them might one day be compromised.

- Social Status. The respect of other people, who admire it as an amazing accomplishment, who rightly interpret it as a sign of his acumen and his value to society, and–let’s be honest–who want to be close to him because of that. If its value were to fall dramatically, he would lose some of that admiration, that respect, that special attention that he gets from the world. As a human being with pride, he would surely suffer at the loss.

Many successful individuals in our society that have accumulated large amounts of wealth, Buffet included, have pledged to give it all to charity. But notice that the pledges are always pledges to give it all to charity at death, never to give it all to charity right now. But why not give it all to charity right now, keeping only what is necessary to fund future consumption? Because to do so would require parting with the intangible goods that it confers right now, and that it will continue to confer up until death.

From a Humean perspective, then, Warren Buffet’s $72.3B might as well be “locked up in chests”–it does not circulate in expenditures, and therefore does not affect prices. That is precisely where the potential “free lunch” of a government deficit lies. If money is printed anew and given to Warren Buffet, in exchange for work that he does for others, the money will go into his piggy bank, where it will have no effect on anything. The work done will therefore have been provided at no cost to anyone–no cost to Buffet, no cost to the recipients, and no cost to the collective. It will have been paid for by the intangible goods that attach to money, goods that the government can create for free.

Now, Warren Buffett is an extreme example. But any person who puts income into savings, never to be consumed, is operating on the same principle. And a large number of the participants in our global economy–who collectively control enormous amounts of wealth–do just that. They put their income into savings, which they never end up consuming. The fact that they do this is the reason that a significant portion of the world cannot find gainful employment, a way to contribute. It’s also the reason that a free lunch is on the table, a free lunch that could solve the unemployment problem, if only policymakers knew that it was there to be taken.

Let’s make the point more precise. There are two things that a person can do with income. First, spend it–use it to consume the economy’s output. Second, save it. There are two ways that a person can save income. First, by holding it as money (or trading it for an existing asset, in which case the seller of the asset ends up holding it as money). Second, by investing it–and by “investing it” I mean investing it in the real economy, using it to fund the construction of a new economic asset–a home, a factory, etc.–that didn’t previously exist.

Inflation occurs in environments where excessive demand is placed on the economy’s labor and capital resources–demand for which there is insufficient supply. From the perspective of inflation, the only income that directly matters is income that is spent or invested–income that is used to put demand on the economy’s labor and capital resources. Income that is held as savings does not put demand on those resources, and therefore has no effect on prices. It follows that if a government creates new money to finance a deficit, delivering that money as income to someone in the form of a tax cut, a transfer, or a direct payment in exchange for goods and services provided, and if the receiver of the income is not inclined to spend or invest it, but instead chooses to hold it idly in savings, in pursuit of the intangible goods that savings confer, then a free lunch is possible. Everyone can benefit, without anyone having to sacrifice.

Now, free lunches aren’t on the table everywhere. But in the economies of the developed world, where there are large output gaps and large overages in the demand for savings relative to the demand for investment, free lunches are on the table. Unfortunately, many policymakers don’t understand how they work, and therefore haven’t been able to take advantage of them.

Myth #2 — Large Government Deficits Are Unsustainable

If a government runs a large deficit in perpetuity, the debt will grow to an infinitely large value, a value that the government won’t realistically be able to pay back. But there’s nothing wrong with that. Government debt is supposed to grow to infinity, along with all other nominal macroeconomic aggregates. It isn’t supposed to ever be paid back.

In essentially every country and economy that has ever existed, nominal government debts have grown indefinitely. They have never been fully paid back, only refinanced or defaulted on. The following chart shows the gross nominal debt of the U.S. Federal Government from 1939 to present (FRED: Gross Federal Debt, log scale). As you can see, there was never a sustained period in which any substantial portion of it was paid down:

What matters is not the nominal quantity of debt that a government owes, but the ratio of that quantity to the economy’s nominal income, which is the income stream from which the government draws the tax revenues that it uses to service the debt. That income stream also grows to infinity, therefore its ratio to government debt can stabilize at a constant value, even as the government continues to run deficits year after year after year.

Let d refer to the size of the primary government deficit (before interest expense is paid) as a percentage of GDP, let i refer to the average annual interest rate paid on the outstanding government debt, and let g refer to the economy’s nominal annual GDP growth, given as a percentage of the prior year’s GDP. We can write a differential equation for the rate of change of the debt-to-GDP ratio over time. Setting that rate equal to zero and solving, we get the following equation for the debt-to-GDP ratio at equilibrium:

(1) Debt / GDP = d / (g – i)

When we say that a deficit is sustainable, what we mean is that running it in perpetuity will produce a Debt-to-GDP ratio that stabilizes at some value, rather than a debt-to-GDP ratio that grows to infinity. Per equation (1), any government deficit, run in perpetuity, will be sustainable, provided that the economy’s equilibrium nominal growth rate g exceeds the equilibrium interest rate i paid on the debt.

To illustrate the application of equation (1), suppose that to keep the economy on a 2% inflation target, with 4% nominal growth, a government would have to run a primary deficit of 5% of GDP in perpetuity. Suppose further that the nominal interest rate that the central bank would have to set in order to control inflation under this regime would be 1%. At what value would the Debt-to-GDP ratio stabilize?

To answer the question, we note that d is 5%, g is 4%, and i is 1%. Plugging these values into the equation, we get,

(2) Debt / GDP = 5% / (4% – 1%) = 5% / 3% = 166%

Now, let’s increase the interest rate i from 1% to 3%. Plugging 3% into the equation, we get,

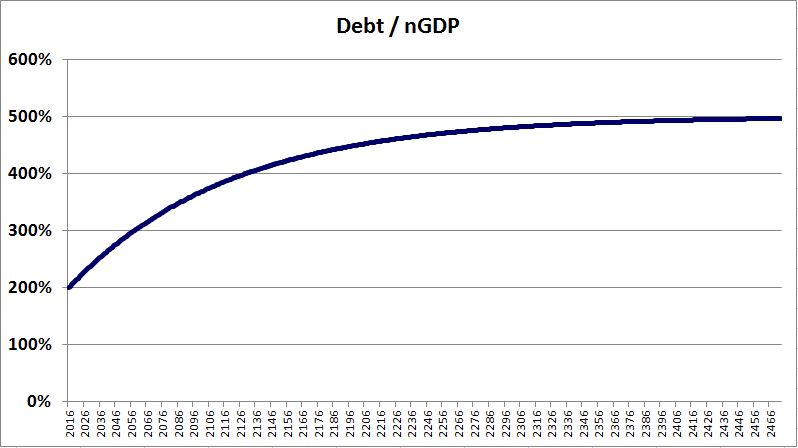

(3) Debt / GDP = 5% / (4% – 3%) = 5%/1% = 500%

As you can see, the Debt-to-GDP ratio is extremely sensitive to changes in the interest rate paid on the debt, particularly as that rate gets closer to the economy’s nominal growth rate.

The following chart shows the amount of time that it would take to get to the 500% Debt-to-GDP equilibrium, assuming a 200% Debt-to-GDP starting point (roughly, Japan’s current ratio, in gross terms).

As you can see, it would take a very long time–more than 400 years. Just to get to 300% Debt-to-GDP would take over 50 years. It’s misguided, then, for policymakers to worry about the sustainability of deficits that will only need to be run, in worst case scenarios, for a decade or two.

Now, in countries such as Greece and Ecuador, where the government debt is denominated in an external currency, large accumulation of government debt can be dangerous. The interest rate paid on the debt is set directly by lenders in the market, and therefore the equivalent of a fiscal “bank run” can develop, in which lenders, concerned with rising debt, demand higher interest rates in order to lend, which causes deterioration in the fiscal budget, which increases concern among lenders, which leads them to demand even higher interest rates in order to lend, which causes further deterioration, and so on.

Fortunately, the countries outside of the Eurozone that currently need fiscal stimulus–the U.S., Japan, and the U.K.–have sovereign control over the currencies that their debts are denominated in. They can therefore set the interest rates on their debts as low as they want to, short-circuiting any attempted run on their finances. Of course, the consequence of setting interest rates too low might be an inflation–a “run” in a different form–but a direct run, occurring in the form of lenders refusing to lend, can always be stopped. This point will be addressed in further detail in subsequent sections.

Myth #3 — Large Government Deficits Lead to Rising Interest Rates

It’s often assumed that if a government accumulates debts in large amounts, that the interest rate that the market will demand in order to lend to that government will rise, not only in nominal terms, but in real terms. This assumption is based on two feared dynamics:

- Positive Feedback Loop: Rising debt implies rising default risk, which causes lenders to demand higher interest rates in order to lend, which worsens the fiscal picture, which increases the default risk, which causes lenders to demand even higher interest rates in order to lend, and so on.

- Excessive Supply: The government has to find people willing to hold its debt in asset portfolios. As its debt increases, finding the needed quantity of willing holders becomes more difficult. Higher interest rates then have to be offered in order to attract such holders.

These concerns are refuted by actual experience. With the exception of Greece, a country tied down to an external monetary standard from which it is expected to eventually exit, the countries with the highest debt levels in the world relative to GDP–the U.S., Japan, the U.K., and the rest of the Eurozone–are able to borrow at the lowest interest rates in the world. This relationship isn’t a recent phenomenon–it was observed in past eras as well. The U.S. and the U.K. accumulated very large government debts relative to GDP in the 1940s. But interest rates during that decade stayed very low–indeed, at record lows–and remained low for more than a decade afterwards.

High debt levels relative to GDP and low interest rates are often observed together because they share a number of the same potential causes. Persistently weak nominal economic growth, for example, calls for policymakers to lower interest rates. It also demands more fiscal stimulus, fueling a faster increase in government debt. The debt-to-GDP ratio itself grows faster because the growth in the denominator of the expression stalls, as debt continues to be added on to the numerator.

Those who fear that large government debt accumulation will put upward pressure on interest rates do not fully understand how interest rates work. Interest rates in a given currency are ultimately determined by the issuer of that currency. The mechanisms can be different in different types of systems, but the issuer usually controls the interest rate by expanding or reducing the quantity of loanable funds in the system, which moves the interest rate down or up in accordance with the dynamic of supply and demand. If the issuer wants to, it can go so far as to create and lend out money directly, at whatever rate it wants, to whomever it wants.

Rising interest rates, then, are not a meaningful risk for a government that owes debt in a currency that it issues. The government itself gets to determine what its interest rate is going to be. In practice, the government is going to set interest rates at the minimum level that keeps inflation on target. Fortunately, in an economy that is suffering from structural weakness in aggregate demand, that level will tend to be very low, allowing for the servicing of a large debt.

The best way to illustrate these points is with a concrete example. Suppose that in watching the national debt expand indefinitely, lenders in the U.S. were to become afraid of an eventual government default–not immediately, but at some point in the future. This highly irrational fear would initially manifest itself as a refusal to hold long-dated U.S. treasury securities. The yields on those securities would therefore rise. But who cares? The U.S. government does not need to borrow at the long-end of the curve. It can borrow at the short-end–indeed, it should borrow at the short-end, to save itself money. When it borrows at the long-end, it has to pay term-premium to lenders, compensation for requiring them to commit to the loan for an extended period of time. Paying this premium would make sense if the commitment were of value to the U.S. government–if it created space that made it easier for the U.S. government to find lenders willing to refinance its debt, when the debt comes due. But the commitment obviously doesn’t have that value, because the U.S. government doesn’t need to find lenders willing to refinance its debt–it effectively has the power to lend to itself.

If the fear of default were to grow acute, it would manifest itself in the form of a refusal on the part of investors to hold short-dated U.S. treasury securities. The yields on those securities would therefore rise. What happens next would depend on whether banks retained confidence in the government’s willingness and ability to make good on the securities.

Suppose that banks were to retain that confidence. The rise in short-dated treasury yields would then create an immediate arbitrage opportunity for them to exploit. Recall that the Federal Reserve sets the cost of funding for banks by manipulating the aggregate supply of excess reserves available to be lent between individual banks overnight to meet reserve requirements, and by setting the rate on loans made directly to banks for that purpose, through the discount window. This cost of funding is essentially the short-term interest rate for the U.S. economy. If the yield on short-term treasury securities were to spike to yields substantially above that rate, then banks could borrow at the rate, use the borrowed funds to buy short-term treasury securities, and collect the spread as profit. Assuming that the U.S. government were able and willing to make good on the securities, this profit would accrue completely risk-free–with zero credit risk and zero duration risk.

It’s tempting to think that if banks were to try to exploit this arbitrage, stepping in and buying high-yield treasuries, that they would have to curtail their loans to the rest of the private sector, to make regulatory space for the loans that they are effectively making to the government. But this is wrong. With respect to regulatory capital ratios, treasury securities have a zero risk weighting. Banks have regulatory space to borrow to buy them in whatever quantity they want, without having to alter any other aspect of their balance sheets or their operations.

But even if banks were unwilling to hold treasury securities, the U.S. government’s ability to borrow would still remain unconstrained. For the Federal Reserve could solve the problem by directly purchasing the securities in the market, pushing up on their prices and down on their yeilds. Surely, banks and investors would be comfortable holding the debt of the U.S. government if they knew that the Federal Reserve was in the secondary market, willing to buy them at any price.

To take the example to the maximum extreme, even if banks and investors had become so afraid that they were uncomfortable buying discounted debt that the Federal Reserve was willing to buy from them in the secondary market at par, Congress could simply modify the Federal Reserve Act to allow the Federal Reserve to buy securities directly from the treasury, lending to the treasury directly, without using the secondary market as a conduit.

The point, then, is this. Governments control the interest rates of currencies they issue. The path may be cumbersome, but if a government owes debt in a currency that it has the power to issue, then it can set the interest rate that it pays on that debt as low as it wants, including at zero, which is the interest rate that it pays when it finances itself by issuing money proper. A situation in which rising interest rates force a currency-issuing government to default is therefore completely out of the question.

Myth #4 — Large Government Deficits Are Necessarily Inflationary

It’s true that large government deficits, and the large equilibrium government debts that those deficits produce, can lead to inflation. But, as we will explain in the next section, the path is not direct.

As Hume explained in an earlier quote, inflation requires excessive spending–demand that exhausts the economy’s capacity to supply for it. Large government deficits can certainly be used to finance excessive spending on the part of the government, and such spending can certainly be inflationary. But it’s not the deficits themselves that produce the inflation, it’s the excessive spending on the part of the government.

Similarly, large government deficits can be used to finance tax cuts and transfers that increase private sector income, leading to excessive private sector spending and eventual inflation. But again, it’s not the deficits themselves that produce the inflation, it’s the excessive private sector spending. In cases where deficit-financed tax cuts and government transfers are put in place, but do not lead to excessive private sector spending, either because the proceeds are saved, or because there is an output gap, the result will not be inflation.

In summary, large government deficits, run for indefinite periods of time, can provide free lunches, are sustainable, do not lead to rising interest rates, and are not inherently inflationary. The implication, then, is that a policy of fiscal inflation targeting need only focus only on its target, the inflation rate, and that the quantity of government debt that it leaves behind can be ignored. This implication is true in most cases, but it’s not true in all cases. The debt that the policy accumulates can, in theory, become a problem in the future. It’s importantly that we explain how it can become a problem, so that the risks of the policy are not misunderstood. The sections that follow are devoted to providing that explanation.

Stock and Flow: The Inflationary Mechanism of Government Debt

To better understand the inflationary dynamics of government debt, we need to make a distinction between “stock” and “flow.” Stock refers to the amount of something that exists; flow refers to the amount of something that moves in a given period of time.

Imagine a collection of bees swarming around in a cage. The number of bees in the cage is a stock quantity. The number of bees that manage to escape from the cage each hour is a flow quantity.

We define money as “legal tender”–whatever must be accepted, by law, to repay debts, public and private. We define financial wealth as money, or anything that can be readily converted into money in a market, considered in terms of its current market value, minus whatever liabilities are tied to it. Because financial wealth can be readily converted into money, we can treat it as the functional equivalent of money.

In an economic context, financial wealth has a stock aspect and a flow aspect. The stock aspect is the total amount of it that exists. The flow aspect is the total amount of it that circulates in the form of expenditures in a given period of time. Note that by “expenditure” we mean the exchange of money for real goods and services. The trading of money for other forms of financial wealth is not included, though such trading may occur as part of the process of an expenditure (e.g., I sell a stock in my portfolio to raise money to buy a car).

When a government spends money on a purchase or project, it creates a one-time flow of spending. This one-time flow takes place regardless of how the spending is funded or financed. If the flow is inserted into an economy that does not have available resources from which to supply the added demand, the flow will tend to be inflationary.

By “paying for” the spending through taxation, a government can potentially reduce private sector spending flows, “making room” in the economy for its own spending to occur without inflation. But not all taxation reduces private sector spending flows equally. When taxes are levied on individuals that have a low marginal propensity to spend, the spending flows of the private sector tend to not be substantially affected. To quote Hume, the taxed money is money would that have remained “locked up in chests” anyways. Taxing it therefore does not free up resources for the government to use. It is only when taxes are levied on individuals that have a high marginal propensity to spend that taxation reliably frees up resources and offsets the inflationary effects of government spending.

When a government chooses not to “pay for” its spending through taxes, and instead finances its spending with debt or money creation, a stock effect is added to the one-time flow effect of the spending. Because the spending is never redeemed in taxes, new forms of financial wealth–debt securities and money proper–end up being permanently added to the system as residuals. The residuals are left without any individual liabilities to offset them. Of course, they are offset by the liability of government debt, a liability that the private sector bears collective responsibility for. But, crucially, individuals in the private sector do not view government debt as their own personal liabilities, and therefore do not count it in tallies of their own personal net worth. Consequently, the net financial wealth of the private sector, as tallied by the individuals therein, increases.

Now, when you increase the stock of something, you tend to also increase its flow, all else equal. If you increase the stock of bees in a cage, and you change nothing else, you will tend to also increase the number of bees that fly out of the cage as time passes. To illustrate, suppose that there are 1,000 bees in a cage. Suppose further that the statistical probability that a given bee will escape in an hour is 0.2%. How many bees will escape each hour? The answer: 1,000 * 0.2% = 2. If you hold that probability constant, and you double the number of bees in the cage to 2,000, how many bees will escape each hour? The answer: 2,000 * 0.2% = 4. So we see that with the escape probabilities held constant, doubling the stock doubles the flow.

A similar concept applies to financial wealth. If the net stock of financial wealth in an economy is increased, and if the probability that a given unit of financial wealth will be spent per unit time remains constant through the change, then the amount of financial wealth that circulates in the form of expenditures per unit time–aggregate demand–will rise.

That’s where the true inflationary effect of government debt accumulation lies. Government debt is an asset of the private sector. When it is held by the central bank, it takes the form of money in the hands of the private sector (the money that the central bank had to create to buy those securities). When it is held directly by the private sector, it takes the form of government debt securities. Thus, when government debt is increased, the private sector gains an asset (money or debt securities) without gaining any liabilities (at least not any that it views as such). It follows that when government debt is increased, the total net financial wealth of the private sector is increased. Increases in net financial wealth tend to produce increases in spending, and excessive spending can generate inflation.

In the next two sections, I’m going to introduce two related concepts that will be useful in our efforts to understand the inflationary potential of government debt. Those two concepts are: wealth velocity and wealth capacity.

Wealth Velocity: A New Equation of Exchange

Readers with a background in economics are likely to be familiar with the equation of exchange:

(4) M * V = P * Q

The equation of exchange translates money stock into money flow, using the ratio between them, money velocity. Here, M is the money supply (the total stock of money in the economy), V is the money velocity (the percentage of the money stock that is spent–i.e., that flows–in a given year, or equivalently, the probability that a given unit of money will be spent in a given year), P is the price index (the conversion factor between nominal dollars and real things), Q is real output (the flow of real things). Note that P * Q is the total nominal spending in the economy. The equation tells us, trivially, that the total amount of money in the economy, times the probability that a given unit of money will be spent in a given year, gives the total amount of spending in a given year, on average.

The problem with the equation of exchange is that the stock quantity that has the deepest relationship to the flow of spending is not the total stock of money proper, but the total stock of net financial wealth in the economy–money plus everything that can be easily converted into money, considered in terms of its marketable monetary value, minus the monetary value of all debt obligations. (Note: for convenience, we have often been omitting the “net” term, using the terms “net financial wealth” and “financial wealth” to mean the same thing: money plus marketable assets minus debts.)

The best way to write the equation of exchange, then, is not in terms of M, the total stock of money in the economy, but in terms of W, the total stock of financial wealth in the economy:

(5) W * Vw = P * Q

Here, Vw is the wealth velocity–the corollary to the money velocity in the original equation of exchange. We can define it as the percentage of financial wealth in existence that gets spent each year, or equivalently, as the probability that a unit of financial wealth will be spent in a given year. The equation tells us, again trivially, that the total quantity of financial wealth in the economy, times the probability that a given unit of financial wealth will be spent in a given year, gives the total amount of spending that will occur in a given year, on average.

When financial wealth is injected into the private sector through a government deficit, some or all of the wealth may accumulate idly as savings. Wealth velocity–Vw in the equation–will then go down, fully or partially offsetting the increase in W, the stock of wealth. That’s how large government debt accumulation can occur over time without inflation. The wealth is continually injected via debt accumulation, but the injections coincide with reductions in the velocity of wealth, such that total spending does not increase by a sufficient amount to exceed the productive capacity of the economy and produce inflation.

The problem, of course, is that conditions in the economy can change over time, such that the wealth velocity increases, reverting to its pre-injection value, or rising to some other value. The prior stock of wealth that was injected, which had been “quiet” because it was being held idly, may then start circulating, and contribute to an inflation.

Wealth Capacity: An Analogy from Thermodynamics

In thermodynamics, there is the concept of “heat capacity.” The heat capacity of a substance specifies the amount that its temperature will increase when a given amount of heat is added to it. If its temperature will only increase by a small amount in response to a given injection of heat, then we say that it has a high heat capacity. If its temperature will increase by a large amount in response to a given injection of heat, then we say that it has a low heat capacity.

Water has a high capacity. You can add a relatively large amount of heat to a unit of water, and yet its temperature will not increase by very much. Iron, in contrast, has a low heat capacity. If you add the same amount of heat to a unit of iron, its temperature will increase significantly. Intuitively, we can think of the temperature increase as the heat “overflowing” from the iron, which is a poor store of heat. The heat does not “overflow” from water to the same extent, because water is a good store of a heat.

If the reader will allow us to be somewhat sloppy, we can extend the thermodynamic concept of “heat capacity” to economics, naming the analogous property “wealth capacity.” At a given interest rate, how much financial wealth can an economy store without overheating? The answer, which is determined by the wealth velocity that will manifest at that interest rate, and the total productive capacity of the economy, specifies the economy’s wealth capacity. Importantly, an economy’s wealth capacity is specified as a percentage of its potential GDP, which then incorporates productive capacity into the expression. So, at a given interest rate, an economy might have a wealth capacity of 50% of potential GDP, or 100% of potential GDP, or 200% of potential GDP, and so on.

If an economy has a wealth capacity that exceeds its current quantity of wealth, then it can hold additional financial wealth, and therefore its government can accumulate debt without inflation occurring. Conversely, if an economy has a wealth capacity equal to or less than its current quantity of financial wealth, then it will not be able to hold additional financial wealth, and therefore government debt accumulation, which involves the injection of financial wealth, will be inflationary.

To make the same point that we made with wealth velocity, wealth capacity is not static, but changes in response to changing macroeconomic conditions. The risk, then, is that a large injection of wealth will be made, and the economy will appear to be able to absorb it, without inflation. But over time, as macroeconomic conditions change, the wealth capacity may fall, such that the prior injection, which pushed up the stock of wealth, contributes to an inflation. That’s why the question of the appropriate level of government debt in an economy is not simply a question of how much financial wealth it can store right now, but a question of how much financial wealth it will be able to store over the long-term, under the different conditions that it will come to face.

The Factors that Influence Wealth Velocity and Wealth Capacity

Though they are not perfect inverses, wealth velocity and wealth capacity are inversely-related to each other. All else equal, high wealth velocity is associated with low wealth capacity, and low wealth velocity is associated with high wealth capacity.

The following factors influence an economy’s wealth velocity and wealth capacity:

Confidence. The value of the money that a country issues rests on the confidence that the money will serve as an effective store of value. As that confidence breaks down, whether in the face of mismanagement or conflict, individuals will be less willing to hold the money, more inclined to spend it in a rush, invest it in real assets, or transfer it abroad. Thus, as confidence in a country’s money breaks down, its wealth velocity will tend to rise, and its wealth capacity will tend to fall. The same is true in the other direction. As a country’s money becomes more credible, more like a reserve currency that the world trusts as a long-term store of value, individuals will be more willing to hold it. The country’s wealth velocity will then fall, and its wealth capacity will rise.

Location of Homestead. Do the owners of a country’s financial wealth–the stock of money and marketable securities contained in the country’s economy–live and spend the bulk of their money in that country? Or do they live and spend the bulk of their money in some other country? Are they holding wealth in that country because that country is where their responsibilities–financial and otherwise–are located? Or are they holding wealth in that country because they see an opportunity for a “hot money” profit? If the former, there will be a greater willingness on the part of the owners of the economy’s financial wealth to hold it, rather than deploy it into consumption or investment, given that the safety and security that comes with holding it will will actually be relevant to the owners’ lives. It follows that the economy will have a lower wealth velocity and a higher wealth capacity (h/t to @Chris_Arnade for this insightful observation).

This point is important, so let me give an example. Suppose that I am a Japanese businessman that owns a significant quantity of financial wealth. Regardless of what happens to the yen’s exchange rate to other currencies, psychologically, I measure the entire financial world in terms of yen. I fund my lifestyle with yen, all of my debts are in yen. Having a substantial quantity of yen in savings therefore provides me with a special type of insurance. It helps ensure that I stay rich, by my own measure of “richness.” It helps ensure that I retain the ability to fund my lifestyle, and meet my debts. The fact that there are many people like me, controlling large amounts of Japanese financial wealth, makes it easier for the Japanese government to inject large quantities of yen and yen-denominated securities into the Japanese economy, and find people willing to hold them rather than spend them, even at low rates of return, so that inflation stays low.

But if I am a wealthy Japanese businessman holding my financial wealth in the form of Uruguayan peso, I do not get the same insurance. Having a substantial quantity of Uruguayan peso in reserve does not reduce the likelihood that I might one day lose the ability to fund my yen-denominated lifestyle, or pay my yen-denominated debts–at least not to the same extent. And so if the owners of Uruguay’s financial wealth are all people like me, people speculating from abroad, the Uruguayan government will not be able to inject large quantities of new peso and peso-denominated securities into the economy at low rates of return, and have people like me continue to hold them. We will want to trade them for higher yielding assets in the Uruguayan economy–that’s why we’re involved with Uruguay in the first place, to get a return. If the prices of those assets get pushed up to unattractive levels in response to the wealth injection, we–or those wealthy foreigners that end up holding our pesos after we sell them–will opt to create new assets in the Uruguayan economy through investment, rather than hold Uruguayan money without compensation. The result will be inflationary pressure.

Distribution of Financial Wealth. An economy’s wealth capacity will tend to be higher, and its wealth velocity lower, if the distribution of financial wealth within it is narrow rather than broad. The reason is obvious. As an individual’s level of financial wealth increases, her propensity to put additional financial wealth that she comes upon into consumptive use goes down. It follows that an economy in which the financial wealth is narrowly distributed among a small number of wealthy people will have a lower propensity to consume additional financial wealth, and therefore a higher financial wealth capacity and lower wealth velocity, than an economy where the financial wealth is broadly distributed among the entire population.

Target of the Financial Wealth Injection. When a government deficit is used to inject financial wealth into an economy, into whose hands is that wealth injected? Is it injected into the hands of wealth-lacking people who need it to fund their desired lifestyles, and are eager to spend it? Or is it injected into the hands of wealth-saturated individuals that do not need it to fund their desired lifestyles, and who not are eager to spend it? The velocity of the wealth–the speed at which it will circulate–will obviously be higher under the former than the latter.

Tendency of Financial Wealth to Collect in Spots. When wealth is injected and spent, does it continue to move around the economy in a sustained cycle of spending, or does it eventually collect idly in a certain spot, where it gets hoarded? If it continues to move around, then the wealth capacity will be low; if it tends to collect idly in a certain spot–e.g., in the corporate sector, where it gets hoarded as profit after the first expenditure–then the wealth capacity will be high.

Consumptiveness. The consumptiveness of an economy refers to the extent to which the individuals that make up the economy are inclined to consume incremental income rather than hold it idly. All else equal, an economy with higher consumptiveness will have a higher wealth velocity and a lower wealth capacity. An economy’s consumptiveness is influenced by a number of factors, to include its history, its culture, its demographics, the prevailing sentiment among its consumers, and so on.

Investment Risk Appetite. The simple fact that an economy likes to save does not mean that it will have a high wealth capacity. For there are two ways to save. One can save by holding money idly (or trading it for existing securities, in which case someone else, the seller of those securities, ends up holding it idly), or one can save by investing it in the creation of new assets–new projects, new technologies, new structures, and so on. The distinction between saving by holding and saving by investing is important because saving by investing involves spending that puts demand on the economy’s existing labor and capital resources. It can therefore contribute to inflation and economic overheating, even as it increases the economy’s productive capacity.

The term “investment risk appetite” refers to the inclination of an economy to save by investing, rather than by holding. An economy with high investment risk appetite will have a lower wealth capacity than an economy with low investment risk appetite. As with consumptiveness, an economy’s investment risk appetite is influenced by a number of factors, to include its history, its culture, its demographics, the sentiment and prevailing outlook of its investors, and so on.

In contrast to consumption, the risk that investment will produce inflation is alleviated by the fact that investment adds new assets, new resources, new productivities that the economy can use to supply the additional consumption demand that will be created. But investment does not deliver those assets, resources, and productivities immediately–there is a time delay. Moreover, the investment may not be adequate, or appropriately targeted, to supply the additional consumption demand that will be created. And so inflation and economic overheating are still possible.

The final factor that influences wealth velocity and wealth capacity is the interest rate, a factor that policymakers have direct control over. Higher interest rates are associated with lower wealth velocity and higher wealth capacity, and lower interest rates are associated with higher wealth velocity and lower wealth capacity. We discuss this relationship further in the next section.

Interest Rates: The Economy’s Inflation-Control Lever

If pressed, those that are concerned about the risks of large government debt accumulation will usually accept the point that governments can inject financial wealth–new money and debt securities–into the economy without creating inflation, provided that the recipients of that wealth choose to hold it idly rather than convert it into some kind of spending. But they point out that the simple possibility that the injected financial wealth could be spent, and produce inflation, is reason enough not to make the injection. To make the injection would be to give the recipients the power to spend, and therefore the power to consume at the expense of other savers, who would lose out in the resulting inflation.

The problem with this point is that economic participants already have the power to consume at the expense of savers. They can accelerate their consumption, by spending more of what they earn, or by borrowing. The acceleration will stimulate inflation, which will occur at the expense of those that have chosen to save. So the inflation risk introduced by government debt accumulation, and associated private sector wealth injection, is a risk that already exists at the current level of government debt, and that would exist at any level of government debt.

For an economy that contains a given quantity of financial wealth, the amount of inflation that it experiences will be determined by the balance of “holding money idly” vs. “deploying money into consumption and investment” that takes place within it. That balance can shift at any time. Fortunately, governments have a tool that they can use to manage the balance, so as to control inflation. That tool is the interest rate. The interest rate is the expense that individuals must pay in order to borrow money to consume and invest. Conversely, the interest rate is the reward that individuals receive in exchange for holding money idly, rather than deploying it into consumption or investment. When individuals hold money idly, they take it out of circulation, where it cannot contribute to inflation.

When an economy is suffering from too much activity, the government will set the interest rate at a high level, providing generous compensation to whoever willingly agrees to hold money idly. When an economy is suffering from too little activity, the government will set the interest rate a low level, removing the reward–or worse, imposing a punishment–on whoever chooses to hold money idly.

In terms of the risks of large government debt accumulation, the primary risk is that the debt will make it more difficult for policymakers to change interest rates in response to changing economic conditions–changing wealth velocities and wealth capacities. When interest rates are increased in the presence of an overwhelmingly large government debt, the interest expense that the government incurs on that debt increases. If the increased expense is funded with tax increases and spending cuts, the economy will suffer a destabilizing effect, both economically and politically. If the increase is funded with additional debt, the result will be added inflationary pressure, because government debt accumulation entails additional private sector wealth injection.

To come back to the example of Japan, right now, Japan is underutilizing its labor and capital resources, a fact demonstrated by its 0% inflation rate. In terms of stimulus, Japan would benefit from a large fiscal deficit, run over the next several years, if not for longer. But conditions in the Japanese economy might one day change, to where the population’s propensity to consume and invest, rather than hold savings idle, meaningfully increases. If that propensity does change, and if Japan has an enormous government debt to finance when it does, then controlling inflation with interest rate increases could become difficult, if not impossible. I explore this scenario in a later section.

Asset Prices: A Second Inflation-Control Lever

It turns out that there is an additional channel through which interest rates can influence inflation. Interest rates–in specific, the interest rate paid on cash (money and very short-term low-risk debt securities)–affects the prices of all existing assets. Rising interest rates make the return on cash more competitive with the return on existing assets, and therefore tend to cause the prices of those assets, in cash terms, to fall. Conversely, falling interest rates make the return on cash less competitive with the return on existing assets, and therefore tend to cause the prices of those assets, in cash terms, to rise.

Crucially, the quantity of financial wealth in an economy includes not just money proper, but all forms of financial wealth contained within it–debt securities, equity securities, real estate, collectibles, and so on. When the prices of these assets rise, the stock of financial wealth in the economy rises–not only in a gross sense, but in a net sense, because the liabilities that the assets match to don’t increase in the same way. The increase in the stock of financial wealth has the potential to lead to an increase in its flow–spending.

The pass-through from asset values to spending tends to be weak with respect to debt and equity securities, because those securities tend to be owned by small, wealthy segments of the population that have a low marginal propensity to spend, and because changes in the prices of the securities aren’t interpreted or trusted to be permanent. But in asset markets where ownership is more evenly distributed across the population, and where the upward price trend is interpreted to be more stable and reliable–in housing markets, for example–the pass-through can be significant.

Trapped Monetary Policy: How Things Can Go Wrong

The best way to illustrate the risk of large government debt accumulation is to use an extreme example. So here we go. Suppose that Japan has implemented our recommended policy of 2% fiscal inflation targeting. Suppose further that conditions in Japan are such that to maintain the economy on a 2% inflation target, the country needs to run a 20% deficit with interest rates at 0%. Suppose finally that the long-term nominal growth rate under the given conditions will be 3%. Assuming that Japan starts with net government debt at its current value, roughly 134% of GDP, the debt would rise to roughly 500% by 2055 and 667% at equilibrium (20% / 3%), to be reached well over 100 years from now.

Now, let’s fast forward to 2055. By then, conditions in the Japanese economy may have changed. After 40 years of sustained 2% inflation, the cultural propensity of Japanese consumers to spend rather than save, and of Japanese savers to invest in the real economy rather than hold yen idle, may have increased. The demographic profile may have improved. Much of the financial wealth injected by the deficits may have “leaked”, through channels of consumption, investment, inheritance, and charity, from high net worth segments of the economy, where it was pooling, to lower net worth segments of the economy, where the marginal propensity to spend it will be higher.

In practice, these changes, if they were to occur, would be expected to occur gradually, allowing the central bank time to adjust fiscal and monetary policy so as to accommodate them. But to make the dynamic vivid, let’s assume, for the sake of argument, that the changes occur instantaneously, in the year 2055. To summarize the scenario, Japan runs a 20% deficit for 40 years, accumulates a government debt worth 500% of GDP, and then suddenly, the macroeconomic backdrop changes.

To frame the dynamic in terms of wealth velocity, the changes, when they occur, will cause the wealth velocity in Japan to increase significantly. The significant increase in wealth velocity will apply to a very large stock of financial wealth–500% of GDP–and will likely push the economy’s total spending to levels that will exceed its available labor and capital resources. The result will be inflationary pressure. To frame the dynamic in terms of wealth capacity, the changes, when they occur, will significantly reduce Japan’s capacity to store financial wealth. The country will no longer be able to hold money and government debt securities worth 500% of GDP at zero interest rates. The result, again, will be inflationary pressure.

How will the government deal with this pressure? Clearly, it will need to start by raising taxes and cutting spending, so as to bring its enormous 20% deficit down to something small. But that will only remove future injections of financial wealth; it will not reverse the prior injections, the potential circulation of which represents the primary inflationary threat. To reverse the prior injections, the government would have to run a surplus, and there is no way that surpluses sufficient to unwind more than 300% of GDP in added financial wealth could be run in any reasonable amount of time.

Ultimately, the only way to prevent the large stock of wealth from circulating and stirring up inflation would be through an increase in the interest rate. By increasing the interest rate, the BOJ would give Japanese wealth owners the needed incentive to hold the large supply of yen cash and debt securities that will need to be held. Without that incentive, the supply will be tossed around like a hot potato, fueling an inflation. (Note: the prices of the debt securities would fall in response to the interest rate increase, causing their yields to rise and making them more attractive to hold, and also lowering the total market value of financial wealth in the economy).

Let’s suppose that in order to manage the inflationary pressure, the BOJ would need to raise interest rates from 0% to 7%. At an interest rate of 7% and a total debt stock of 500%, the government’s added debt expense would amount to 500% * 7% = 35% of GDP. That’s an enormous expense. Where would the money to fund it come from?

The government could try to increase taxes or cut spending to make room to pay it, but the total size of the tax increases and spending cuts that would be necessary would be 35% of GDP–a number that would be extremely difficult to successfully draw in, and highly economically and politically destabilizing, if a way to draw it in were found.

It’s likely, then, that the Japanese government would have to borrow to pay the interest. But borrowing–by running a deficit–would entail the injection of a substantial quantity of new financial wealth–35% of GDP, if all of the interest were borrowed–into the already overheating private sector. That injection–which would accrue to the holders of yen cash and debt securities in the form of interest income–would represent an additional source of potentially unmanageable inflationary pressure, undermining the effort.

Now, to be fair, it’s possible that Japan could find some way to combine tax increases, spending cuts, and deficit borrowing to pay the interest expense. But we can’t ignore the inflationary effect of the market’s likely behavioral response to the difficulty. In practice, economic participants observing the country’s struggles would become increasingly averse to holding yen cash and yen-denominated debt securities. This aversion would eventually become reflexively self-fulfilling. Wealth velocity would then rise further, with wealth capacity falling further, adding further inflationary pressure. Investors would seek to transfer wealth abroad, causing the yen to depreciate relative to other currencies. The depreciation would make Japanese goods more attractive to the world, again, adding further inflationary pressure.

We can see, then, how an eventual bout of high inflation might become unavoidable, even as the central bank does everything in its power to stop it. The central bank’s preferred tool for combating inflation–the interest rate–would effectively be trapped by the enormous government debt. Its use in the presence of that debt would exacerbate the inflation, or destabilize the economy, or both.

This type of scenario is not purely theoretically, but has actually played out in economic history, most notably in France in the 1920s. In more benign contexts, there have been a number of examples of central banks that were forced to surrender to inflation, prevented by their heavily indebted sovereigns from setting interest rates at the levels needed to maintain control over it. A well-known example is the United States in the years shortly after World War 2, where the Treasury effectively forced the Federal Reserve to hold interest rates at zero, despite double-digit inflation.

In each of these cases, the inflation proved to be a short, temporary occurrence, rather than an entrenched, long-lasting phenomenon. Conveniently, the problem of the large government debt ended up correcting itself, because the inflation it provoked substantially reduced its value, both in real terms and relative to the nominal size of the economy and the tax base. The outcome may have been unfair to those savers who ended up holding money at deeply negative real interest rates, but it did not entail any larger humanitarian harms.

Essentially all of the known historical cases in which large government debt has led to inflation have involved war. One reason why we might expect that to be the case is that war temporarily disables substantial portions of the labor and capital stock of an economy, reducing its productive capacity. But there’s an additional reason. War is expensive, it requires the government to take on substantial quantities of debt. Those quantities are taken on to fund an urgent activity, and so they are allowed to accumulate even as they contribute to excessive inflation. Crucially, when the war ends, the accumulated stock of debt does not go away. It is left as financial wealth in the private sector. As people return home and begin life again, that wealth starts circulating in an inflationary manner–sometimes quickly.

Unlike in war, where government debt is taken on to fund an urgent activity, in fiscal inflation targeting, government debt is taken on in an effort to keep inflation on target, given structural weakness in aggregate demand. Policymakers therefore have space to respond to early signs of rising inflationary pressure–signs that the structural weakness is abating. If Japan were to implement fiscal inflation targeting, and needed to run a deficit worth 20% of GDP with rates at zero to achieve that target, the scenario would not play out as Japan running that deficit for 40 years without seeing any changes, and then suddenly seeing its wealth velocity rise dramatically and its wealth capacity fall dramatically. Rather, the country would run high deficits, macroeconomic conditions would gradually change, with wealth velocity gradually rising and wealth capacity gradually falling, the changes would show up in real-time measurements of inflation, and the central bank would respond, adjusting its fiscal stance, not in an emergency after an unmanageable debt has already been accumulated, but gradually, as the process moves along.

Fiscal Inflation Targeting: A Cost-Benefit Analysis

With the potential inflationary risk of large government debt accumulation now specified–inflation via the mechanism explained in the prior section–we are in a position to weigh the costs of fiscal inflation targeting versus its benefits, and to outline the characteristics that would make an economy with weak aggregate demand and abnormally low inflation a good candidate for the policy.