The growing popularity of passive investing provokes a series of tough questions:

- What necessary functions does active management perform in a financial system?

- What is the optimal amount of active management to have in such a system, to ensure that those functions are carried out?

- If the size of the market’s active share falls below the optimal level, how will we know?

- How much can active managers, as a group, reasonably charge for their services, without acting as a net drag on the system?

To answer these questions, I’m going to explore the curious case of Indexville, an economy whose investment sector has been designed to be 100% passive. As expected, Indexville lacks a number of features that are necessary for the optimal functioning of an economy. I’m going to try to build those features back into it, documenting the cost of doing so each step of the way. Ultimately, I’m going to run into a problem that ingenuity cannot overcome. That problem is the exact problem that active management is needed to solve.

A Journey Into Indexville

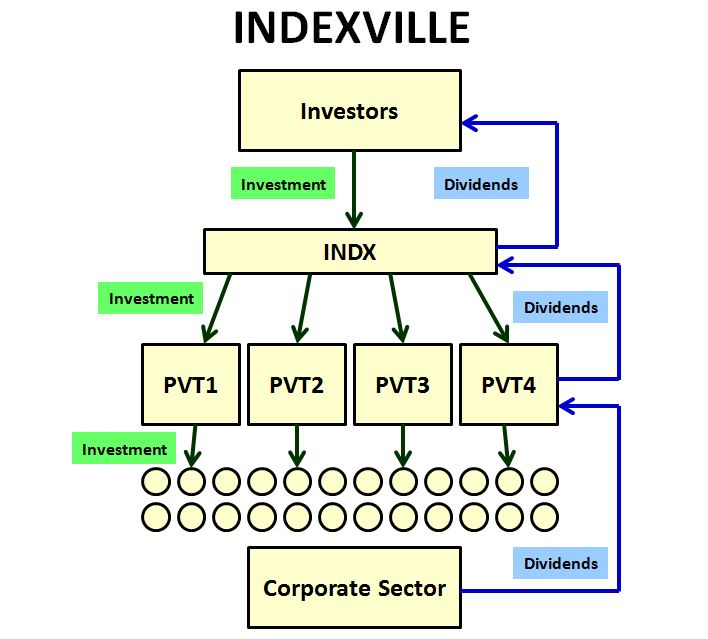

Indexville is an economy similar in its composition to the United States economy, with one glaring exception: the citizens of Indexville consider active management to be unproductive and immoral, and are therefore invested in Indexville’s corporate sector 100% passively, through a fund called INDX. The system works as follows:

When the citizens of Indexville earn excess cash, they have two options:

(1) Hold it in the bank, where it will earn a small interest rate set by the government–an interest rate of, say, 1% real.

(2) Purchase new shares of the economy’s sole investment vehicle, an index mutual fund called INDX.

When INDX sells new shares to investors, it invests the proceeds in one of four private equity funds–PVT1, PVT2, PVT3, and PVT4. These private equity funds, which are independently operated, compete with each other to provide equity financing to the corporate sector. The financing can take the form of either an initial investment, in which a new company is created, or a follow-on investment, in which an existing company is given additional funds for expansion.

If we wanted to, we could broaden the scope of the funds, allowing them to make debt investments in addition to equity investments, not only in the corporate sector, but in the household and government sectors as well. But we want to keep things simple, so we’re going to assume the following:

- All private sector investments in Indexville are made through the corporate sector, and the financing is always through equity issuance. There are no homeowners in Indexville, for example–everyone in Indexville rents out homes and apartments from corporations that own them.

- Direct investment in Indexville’s government sector is not possible. All federal, state and local Indexville paper is owned by the banking system, which is where the small amount of interest paid to cash depositors ultimately originates. If investors want a risk-free option, they already have one: hold cash.

For now, we assume that buying INDX shares is a one way transaction. The shares cannot be redeemed or sold after purchase. Redeeming them would require de-capitalizing the corporate sector, which is unrealistic. Trading them with other people is possible, but the option has been made illegal, consistent with Indexville’s moral ethos of total investment passivity: “Thou shalt not trade.”

Now, every existing company in Indexville was created through the above investment process, so INDX owns the entire corporate sector. That’s what allows us to say that all INDX investors are invested “passively” relative to that sector. Recall the definition we proposed for a passive allocation:

Passive Allocation: A passive allocation with respect to a given universe of assets is an allocation that holds every asset in that universe in relative proportion to the the total quantity of the asset in existence.

The total quantity of corporate assets in Indexville literally is INDX. Whatever the relative proportion between the quantities of the different assets inside INDX happens to be, every investor will own them in that relative proportion, simply by owning INDX shares.

Now, to be fair, the investors in INDX are not passively allocated relative to the entire universe of Indexville’s financial assets, which includes both equity and cash. Though such an allocation might be possible to achieve, it would clearly be impossible to maintain in practice. Anytime anyone spent any money, the spender would decrease his cash, and the recipient would increase it, throwing off any previously passive allocation that might have existed.

The word “passive” can take on another important sense in these discussions, which is the sense associated with a “passive ethos”, where investors refrain from placing trades for speculative reasons, and instead only trade as necessary to carry out their saving and consumption plans, or to transition their portfolios to a state that matches their risk tolerances as they age. This is the sense of the term found in the advice of the gurus of “passive” investing–Jack Bogle, Burton Malkiel, Eugene Fama, and so on. Indexville investors follow that advice, and fully embrace a “passive ethos.”

Returning to the structure of Indexville, the excess profits of the individual companies in Indexville are periodically distributed back up to their respective private equity funds as dividends, and then back up to INDX, and then back up to the investors. These dividends represent the fundamental source of INDX investor returns. Without the potential to receive them, shares of INDX would be intrinsically worthless.

Instead of relying on equity issuance, corporations in Indexville have the option of funding new investment out of their own profits. When they choose to do that, they reduce the dividends that they are able to pay to the private equity funds, which in turn reduces the dividends that the private equity funds are able to pay to INDX investors. But the reduction is compensated for in the long-term, because the new investment produces real growth in future profits, which leads to real growth in future dividends paid.

Cost #1: Conducting Due-Diligence on New Investment Opportunities

To make sound investments–whether in new companies seeking initial capital, or in existing companies seeking follow-on capital–the private equity funds have to conduct appropriate due-diligence on candidate investment opportunities. That due diligence requires research, which costs money–the funds have to hire smart people to go and do it.

Where will the money to pay these people come from? Unfortunately, Indexville’s passive structure has no magic bullet to offer here–the money will have to come from the only place that it can come from: out of investor returns, as fees. It will get subtracted from the dividends paid to the private equity funds, and therefore from the dividends paid to INDX, and therefore from the dividends paid to investors.

What we’ve identified, then, is the first unavoidable cost of a 100% passive system:

Cost #1: The need to pay people to conduct appropriate due-diligence on new investment opportunities, so as to ensure that INDX investor capital is allocated productively and profitably, at the best possible price.

Note that Cost #1 is not driven by a need to put a “trading” price on already-existing companies. The trading prices of such companies do not matter to INDX investors, since INDX already fully owns them, and has no one to sell them to but itself. Nor do the prices matter to the economy, because the physical capital that underlies them has already been formed. The price that people decide to trade that capital at does not affect its underlying productivity.

The need that gives rise to Cost #1 is the need to determine whether a company is an appropriate target for new investment–taking new investor funds, new economic resources, and putting them into a startup, or a struggling company–and whether the investment will produce a better return than other available opportunities, given the proposed price. Mistakes made in that determination have a direct negative impact on investor performance, and lead to suboptimal allocation of the economy’s labor and capital resources.

Let’s ask: what is a reasonable estimate of the total expense associated with Cost #1? How much should we expect it to detract from INDX’s returns? The answer will depend on how much new investment the private equity funds engage in. Recall that most of the investment in Indexville will be carried out by already-existing companies, using retained profits as the funding source. The cost of the research done in association with that investment is already reflected in the net profits of the companies.

The U.S. has roughly 5,000 publicly-traded companies. To be conservative, let’s assume that Indexville’s corporate sector is similarly sized, and that 1,000 companies–20% of the total–seek new funding each year, either in initial public offerings or, more commonly, in follow-on offerings. We want Indexville’s capital to be allocated as productively as possible, so we assign two extremely talented analysts to each company, at an annual cost of $300,000–$200,000 in salary, and $100,000 in capital investment to support the research process. For a full year, the analysts spend the entirety of every workday researching their assigned individual company, rigorously weighing the investment opportunity. The resulting cost:

1000 * 2* $300,000 = $600,000,000.

The U.S. equity market is valued at roughly $30T. Expressed as a percentage of that overall total, the annual cost of investment due diligence in Indexville amounts to 0.002% of total assets.

Of course, we want to have the benefits of aggressive competition in Indexville. So we multiply that cost by 4, to reflect the fact that each of the four funds will carry out the research program independently, in competition with each other. To be clear, then, the four funds will each have 2,000 analysts–8,000 in total–who each spend an entire year effectively researching one-half of a single investment opportunity, at a cost of $300,000 per analyst per year. The total annual expense: 0.008% of total marketable assets.

Consistent with Indexville’s emphasis on engineered competition, an advisory board for INDX has been created. Its responsibility is to evaluate the long-term investment performances of the four private equity funds, and adjust the amount of future funding provided to them accordingly. Funds that have made good investments get a larger share of the future investment pie, funds that have made bad investments get a smaller share. Similar adjustments are made to manager pay. Managers of strongly performing funds see their pay increased, managers of poorly performing funds see their pay decreased.

What will the advisory board cost? Assuming 50 people on it, at an annual cost of $500,000 per person, we get $25MM, which is 0.00008% of assets–in other words, nothing.

Cost #2: Determining a Correct Price for INDX Shares

When investors buy new shares in INDX, they have to buy at a price. How is that price determined? Recall that Indexville’s corporate sector is entirely private. There is no market for the individual companies. Nor is there a market for INDX shares. It follows that the only way to value INDX shares is to calculate the value of each underlying company, one by one, summing the results together to get the total. That’s going to cost money.

So we arrive at the second unavoidable cost of a 100% passive system:

Cost #2: The need to pay people to determine the values of the individual companies in the index, so that new shares of the index can be sold to investors at fair prices.

Cost #1 was a worthwhile cost. The underlying work it entailed was worth doing in order to maximize INDX shareholder returns and ensure efficient capital allocation in Indexville’s economy. Cost #2, in contrast, is a net drag on the system. It has no offsetting benefit, and can be avoided if the participants embrace a cooperative mentality.

Suppose that a mistake is made in the calculation of INDX’s price, and an investor ends up paying slightly more for INDX shares than he should have paid. The investor will see a slight reduction in his returns. That reduction, of course, will occur alongside a slight increase in the returns of existing investors, who will have taken in funds at a premium. In the end, the aggregate impact on the returns of the system will be zero, because price-setting is a zero-sum game.

Now, the direct, short-term impact of pricing mistakes may be zero-sum, but the long-term effect can be negative, particularly if the mistakes cause people to alter their future behaviors in undesirable ways. If consistent inaccuracies are tolerated, people might try to find ways to “game” them. They might also become disgruntled, and cease to participate in the investment process. If that’s what’s going to happen, then we’re not going to have much of a choice: we’re going to have to spend the money needed to make sure the price is as right as it can be, for every new share sale, every day. The cost will come out of everyone’s return, reflecting the drag on the system brought about by the non-cooperative mentality.

Given that Indexville’s corporate sector is roughly the same size as the public market of the United States, the task of accurately calculating the fund’s price will entail valuing roughly 5,000 individual companies. The proposed plan is as follows. As before, we hire two highly talented analysts for each company. We give each analyst the singular responsibility of building a valuation estimate for the company, and adjusting the estimate on a daily basis to reflect any new information that becomes available. The basic instruction to each analyst is:

- Develop an estimate of the company’s future cash flows, and discount those cash flows at a required real rate of 6%, which is what Indexville investors consider to be a fair return. Focus on getting the cash flows right. Your pay will be tied to how well you do that.

- Where there is uncertainty, identify the different possibilities, and weigh them by their probabilities. Do not let the desire to be right in your past analysis influence your future analysis–instead, respond to the facts as they present themselves, with a singular focus on truth, i.e., “what is actually going to happen?”, rather than “what do I personally want to happen?” If necessary, examine past valuation work done on similar companies, especially work done by top-performing analysts, and use their insights to help you triangulate towards a reasonable number.

- Try to be consistent. Don’t dramatically change your valuation estimates from day to day unless something relevant and impactful has taken place–e.g., the company has released an earnings report with important new information in it.

To get to a price for the INDX, we take the two valuation estimates produced for each company and average them together. We then sum the resulting averages, arriving at a total market capitalization for the fund. We then divide the fund’s market capitalization by its number of shares, arriving at a final price. That price is the price at which we sell new shares to investors, with the sales, occurring each day, at the end of the day.

How much will this project cost annually?

5,000 * 2 * $300,000 = $3,000,000,000

But let’s assume that we really want to get the final numbers right, to ensure fairness for all Indexville investors. So we double the effort. We put four analysts on every company, instead of two. The result:

5,000 * 4 * $300,000 = $6,000,000,000

So, $6,000,000,000. Relative to the (assumed) total market capitalization of Indexville’s universe of companies, $30T, the cost represents 0.02% of assets.

Now, you might think that an actual market’s estimate of corporate value will be more accurate than the estimates of these 20,000 analysts. But you have no evidence of that. What would evidence even look like? Markets don’t publish their “future cash flow estimates”, nor do they reveal their “discount rates.” These artifacts can only be arrived at tautologically, by extracting them together from the price. And either way, it doesn’t matter. As long as the citizen’s of Indexville believe that the estimates of the 20,000 analysts are accurate, and maintain their trust in the system, actual inaccuracies will not affect anything, because price-setting, again, is a zero-sum game.

Cost #3: The Provision of Liquidity

Up to this point, we’ve identified two costs that investors in Indexville will have to bear, given that they don’t enjoy the benefits of active management.

- The first was the cost of conducting due-diligence on new investment opportunties. Actual cost: 0.008% of assets.

- The second was the cost of valuing existing companies in the fund so as to determine a fair sale price for new shares. Actual cost: 0.02% of assets.

Both costs proved to be extremely small. Clearly, then, a large active segment is not needed to solve them, especially not at typical active fee levels, which can be anywhere from 25 to 100 times higher.

Unfortunately, there’s a huge problem with Indexville’s system that we haven’t addressed: the problem of liquidity. An investor can convert cash into INDX by purchasing shares, but what if an investor wants to go the other way, and convert INDX shares back into cash? In its current configuration, Indexville doesn’t offer the option to do that.

Unlike money, or even a debt security, an equity security is intrinsically illiquid. It has no maturity date, and offers no direct method of redemption. The cash that went into purchasing it is effectively gone. The only way to directly get that cash back is to have the corporate sector liquidate–a solution that is not realistically possible, and that would require investors to take losses if it were.

What is the real cost of the illiquidity of an equity security? Answer: the inconvenience imposed on the owner. The owner has to factor the cost of the illiquidity into his pricing of the security. If he is making an investment in a new company, and is taking a full equity stake in it, he will have to require a higher future return–higher not to make the overall deal any better for him, but simply to compensate him for the significant drawback associated with losing his ability to access his money. The higher return hurdle that he will be forced to place on the process will disqualify investment prospects that would otherwise be beneficial to everyone, if they were liquid. Similarly, if he is making an investment in an existing company owned by someone else, he is going to have to demand a lower price for his stake. That lower price will come at the existing owner’s expense, rendering the issuance less attractive to the existing owner, and causing him to not want to take in funds and make investments that would otherwise be beneficial to everyone, if liquidity existed.

The cost of illiquidity is real, and therefore it’s important that we find a way to make INDX liquid. So here’s a simple proposal: we give investors an option to sell–not to other people, but to INDX directly, in a mutual fund redemption process. Every day, at the end of the day, we pair buyers and sellers of the fund, exchanging the incoming cash and the existing shares between them. If you are seeking to buy, I pair you with a seller. You take his shares, he takes your cash. And vice-versa. This won’t cost us anything extra, because we already know the fair value of the fund from the prior calculations that we paid for. Investors will then have liquidity.

Indexville’s citizens are likely to be averse to this suggestion, because it enables the toxic practice of market timing. But there are legitimate, non-speculative reasons why an investor may want to sell shares. For example, the investor may be entering a later of phase of her life, and may want to withdraw the funds to spend them down. Either that, or she may simply prefer a more liquid allocation, and be willing to give up some return in exchange for it. Some other investor may have similarly legitimate reasons for wanting to buy new shares–the investor might be in a younger phase of life, and have a greater need to save, or want more growth. What is the harm in pairing the two together, exchanging the shares and cash between them? The exchange may be zero-sum in terms of how the future returns get divided, but it will be positive sum in terms of its overall impact–both investors will end up winners. This contrasts with a scenario where the two investors trade for speculative reasons, because one thinks the price is going to rise, and the other thinks the price is going to fall. That trade will be zero-sum. One trader is going to be right, and the other trader is going to be equally wrong.

Let’s assume that we’re able to convince the citizens of Indexville that there are legitimate uses for liquidity, and that everyone will ultimately benefit from the introduction of a sale option in INDX shares. We’re still going to run into a problem. How will the fund deal with periods in which there is more buying than selling, or more selling than buying? In those periods, excess buyers and sellers will end up leftover, with orders that cannot be met. What will the fund do with them?

If there is more buying than selling, the fund can always issue new shares. But the private equity firms may not need new funds. There may not be any attractive investment opportunities–with returns of 6% or better–for them to deploy the funds into. If we allow new shares to be created at 6%, when there are no 6%-or-better investments for the funds to invest in, we will be harming existing shareholders, diluting their stakes in exchange for nothing.

If there is more selling than buying, the situation becomes more complicated. One option is to take the cash dividends of other investors, and give those dividends to the sellers, in exchange for their stake. On this option, the existing investors will effectively be “reinvesting” their dividends. But they may not want to do that. And even if they do want to do it, the dividend payments in a given quarter may not be enough to fully meet the selling demand. Another option would be for INDX to borrow cash to pay exiting shareholders. On this option, the remaining investors will essentially be levering up their stakes. Again, they may not want to do that. And even if they do want to do it, the option of borrowing for that purpose may not be something that the banking system in Indexville is willing to make available.

Apart from forced dividend reinvestment and forced leveraging, the only other way for INDX to get the cash needed to pay the exiting investors would be to have the corporate sector liquidate, i.e., sell itself. But, again, assuming that all of the capital that went into the funds and companies has been deployed, who exactly are the companies going to sell themselves to? INDX is the only possible buyer, and it has no cash. It’s trying to get cash, to redeem the investors that want to sell it.

A final option would be for INDX to change its price. Instead of having investors exchange shares at a price associated with an implied rate of return of 6%, it could raise or lower the price–i.e., decrease or increase the implied rate of return–in order to discourage buying or selling and balance the demand. Unfortunately, that won’t work. Indexville’s investors are entirely passive. They make investment decisions based on their personal savings and consumption needs, not based on valuation arbitrage, which they do not understand. INDX can raise its price to infinity, or drop its prize to zero–either way, the buying and selling demand of the system will not change. The only thing that will change is that certain unlucky people will end up getting screwed–denied the “fair value” return that they deserve, 6%.

With the above options ruled out, INDX’s only remaining option will be to simply say no:

“We’ve received your sale order. Due to market conditions, we are not currently able to execute it. However, we’ve placed your name in a queue. Currently, you are number 47 in the queue, with $400MM worth of selling demand in front of you. Once we’ve found buyers to take on that selling demand, any subsequent buy orders will be routed through you.”

The problem with this option, of course, is that it represents a loss of investor liquidity. Investors will only have guaranteed immediate liquidity if they are lucky enough to be going against the prevailing investment flows. Otherwise, they will have to wait.

But would that really create a problem? It would certainly create a problem if Indexville’s investors were inclined to trade for speculative reasons. The mere perception of impending excess buying or selling demand would incent them to buy or sell, reflexively exacerbating the ensuing flow imbalance. But Indexville’s investors are not like that. Consistent with Indexville’s passive ethos, they only make trades for legitimate personal reasons–because they have savings to invest, or because they need to draw down on their savings in order to fund their lifestyles.

In certain situations where a large imbalance naturally develops in the economy’s saving preferences, the answer is, yes, it would create a problem. One can imagine, for example, a scenario in which the average age of Indexville’s citizenry increases dramatically, resulting in a large population of older people with a preference for redeeming shares, and only a small population of younger people with a preference for purchasing them. In such a scenario, the older generation will lose its liquidity. But as long as Indexville’s economy remains capable of producing what its citizens want and need, any ensuing problem will be illusory–a problem that results entirely from the accounting artifacts–“shares”, “cash”, etc.–that are being used to divide up the economy’s purchasing power. Policy intervention could easily solve it–for example, by having the government print cash and purchase the shares from the older generation at fair value.

Now, everything I’ve just said is based on the assumption that Indexville’s investors are fully passive, that they do not respond to valuation arbitrage. If that’s not true, i.e., if they have even the slightest of speculative instincts, then the problems with the above proposal will compound. Assuming that Indexville’s economic condition is similar to the current economic condition of the United States, the discount rate at which prices for the fund have been set, 6%, will be too high relative to the small interest rate, 1%, that can be earned on the alternative, cash. The economy will not have a sufficient quantity of investment opportunities, with returns of 6% or better, in order to meet that saving demand. INDX will therefore see a persistent excess of buying–especially if the buyers are reflexively aware that the economy’s strong saving demand will guarantee them future liquidity, should they ever want to sell.

But if Indexville’s investors are active, and respond to valuation arbitrage, then a previously discarded solution will work just fine. All that INDX will have to do to balance the flows is change the price at which purchase and sale orders are executed. If there is too much buying demand, raise the price–the lower implied return will lead to a reduction in buying demand. If there is too little buying demand, lower the price–the higher implied return will increase the buying demand. Of course, to embrace this solution, Indexville’s investors are going to have to abandon the notion that anything other than a 6% return is “unfair.” If there is strong demand for saving in the economy, and if the private equity funds cannot find sufficient investment opportunities with a return above 6% to deploy that saving into, then lower returns will simply have to be accepted.

In the above case, there are tools that the government can use to create higher returns for investors. But those tools come with separate costs. It doesn’t make sense for the society to offer to bear those costs simply to improve the average investor’s lot. The right answer is for investors to accept lower rates of return, which is fair compensation for their investment contributions, given the economy’s reduced need for them.

Returning to the assumption that Indexville’s investors are completely passive and insensitive to arbitrage, there will be no way to address flow imbalances other than by make people wait their turn. The cost of that approach is lost liquidity.

Cost #3: the cost of providing liquidity in situations where the legitimately passive buying and selling flows going into and out of the index fail to balance out.

Unfortunately, there is no amount of money that Indexville can spend to cover that cost, i.e., to provide the desired liquidity. For Indexville to have it, some investor somewhere will have to agree to go active.

Market-Making and Active Management

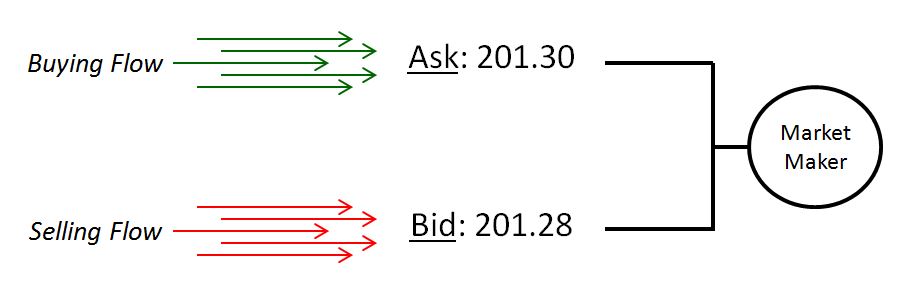

When you place an order in the market to buy a share of stock, how do you place it? If you’re like most people, you place it either as a market order, or as a limit order above the lowest ask price. You do that because you want the order to execute. You want to buy now. If you thought that a better time to buy would come later, you would just wait.

Instead of insisting on buying now, why don’t you just put a limit order in to buy below the prevailing price, and go on about your business? Because you’re not stupid. To put in a limit order below the market price, and then walk away, would be to give the rest of the market a 100% free put option on the stock, at your expense. If the stock goes higher, the gains will end up going to someone else. If the stock goes lower, you will end up buying it, and will get stuck with the losses. Why would you agree to a let someone else have the gains on an investment, while you take the losses?

But wait. There was a limit order to sell that was just sitting there–specifically, the order that you intentionally placed your buy price above, so as to guarantee an execution. Where did that order come from? Who was the person that just stuck it in there, and walked away? What was his thinking?

The person who put that order in, of course, was the market-maker–the person who does the work necessary to create a liquid market. Market orders do not come into the system at the same time. Someone therefore has to bridge them together. That is what a market-maker does. When no one else is around, he puts a bid order in to buy at some price, and an ask order in to sell at some price, slightly higher. He then waits for those that want to trade now to come in and take his orders. In each round-trip transaction, each buy followed by a sell, he earns a spread, the spread between his bid and ask.

The following equation quantifies his revenue:

Revenue = 1/2 * Volume * Spread

So that is his revenue. What is his cost?

His first cost is the cost of doing the work necessary to find out where the right price for the market is. To ensure that he earns the spread, he has to identify the balancing point for the market, the general level at which the buying flow and the selling flow will roughly match. That is the level around which he has to place his orders, so that roughly the same number of people buy from him as sell to him. If he fails to target that level correctly–i.e., if he places his bid and ask orders at levels where the flows will become imbalanced–he will end up accumulating unwanted inventory.

His second cost is the cost of being wrong on the correct market price. If he is wrong, and ends up accumulating unwanted inventory, he will have to either hold that inventory indefinitely, or liquidate it, both of which will occur at a cost. To mitigate the impact of that cost, the market-maker will have to do at least a minimal amount of work to assess the value of what he is offering to hold. He has to know what it’s actually worth, in some fundamental sense, in case he gets stuck holding it.

For market-making to be profitable, the revenue earned has to exceed the costs. There will inevitably be risk involved–one can never be sure about where the balancing point in the market is, or about what the inventory being traded is actually worth from a long-term perspective, or about the magnitude of the losses that will have to be taken if it has to be liquidated. The associated risk is a risk to the market-maker’s capital. For market-making to be attractive, that risk requires a return, which ends up being the total round-trip volume times the spread minus the costs and the trading losses, divided by the amount of capital deployed in the operation.

What Indexville needs is for an active investor to step up and become a market-maker for INDX, so that temporary imbalances in the quantities of buyers and sellers can be smoothed out. The market-maker needs to figure out the patterns that define INDX transactions: When does there tend to be too much buying? When does there tend to be too much selling? If the market-maker can correctly answer those questions, he can bridge the excesses together, eliminating them through his trades. That is what it means to “provide liquidity.”

Given that Indexville’s investors are passive and unresponsive to arbitrage, a potential market-maker won’t even have to worry about what the right price point for INDX shares is. All that will matter is the future trajectory of the flow imbalances, which is entirely set by non-speculative preferences. If the market-maker can accurately anticipate that trajectory, he will be able to set the price wherever he wants, earning as much profit as he wants, without having to unbalance his own holdings.

Will Indexville’s investors get bilked in this arrangement? No. If the market-maker imposes an unreasonably high spread–only offering to buy shares, for example, at an 8% implied return, and only offering to sell them, for example, at a 4% implied return–then other potential active investors will take note of his outsized profits, and enter the fray to compete with him, becoming market-makers themselves. They will jump in front of his bids and asks, forcing him to either compress his spread, or let them get the executions. They will also force him to do more research, because they will now be there to arbitrage his mistakes. Ultimately, the revenue that he is able to earn, and that the Indexville investment community will have to pay him, will converge on his cost of doing business, which is the cost of studying and understanding the market, figuring out what the underlying securities are actually worth, and risking the possibility of getting stuck with someone else’s illiquidity.

Notice that these are the same costs that, up to now, Indexville has had to pay separately, given that it has no active investors. When active investors enter to make a market, the costs no longer need to be paid separately–the active investors can provide the associated services, with the rest of the market compensating them in the form of market-making profits.

Enter Warren Buffett

In February of this year, Druce Vertes of StreetEye wrote an exceptionally lucid and insightful piece on the topic of Active Management. In it, he asked the following question: what would happen if everyone in the market except Warren Buffett were to go passive? He showed, correctly, that Buffett could still beat the market.

In the scenario, when the passive segment of the market wants to sell, Buffett is the only potential buyer. Buffett is therefore able to demand a low price, a discount to fair value. When the passive segment wants to buy, Buffett is again the only potential seller. He is therefore able to demand a high price, a premium to fair value. On each go-round, each shift from passive net selling to passive net buying, Buffett buys significantly below fair value, and sells significantly above it, generating the superior returns that he is famous for.

What is Buffet doing in this example? He is earning the outsized revenues that inevitably come when you provide liquidity to a market that needs it. Those revenues easily cover the cost of providing that liquidity, which is the cost of understanding the psychology of the passive investors, so as to anticipate their net flows, and also the cost of determining the fair value of the underlying securities, to know what prices he can prudently pay for them, in case he gets stuck holding them.

What Indexville needs, then, is a Warren Buffett. But how profitable can Buffett really be in Indexville? The passive investors in Druce’s example appear to be dumb money investors that simply want to time the market, with Buffett as their counterparty. Buffett, of course, is easily able to smoke them. In Indexville, however, things aren’t going to be anywhere near as easy. The only flows that Buffett will have at his disposal will be the minimal flows associated with a passive ethos. Investors in Indexville buy in for one reason and one reason alone: because they have excess savings to invest. They sell out, again, for one reason and one reason alone: because they’re at a point in their lives where they need the funds. There is no speculation, no market timing, no giving away free money to Warren Buffett. The profits that Buffett will be able to earn will therefore drop significantly. And the economy as a whole will be better off for it, because a massive amount of zero-sum friction will have been removed, released for productive use elsewhere.

The Value of Active Management

In the previous two pieces, we expressed the Law of Conservation of Alpha, attributable to William Sharpe:

The Law of Conservation of Alpha: Before fees, the average performance of the investors that make up the active segment of a market will always equal the average performance of the investors that make up the passive segment.

This law does not apply to cases where we define “passive” in a way that allows the passive segment to trade with the active segment. To account for such cases, we need a new law:

The Law of Conservation of Alpha, *With Liquidity: Before fees, the average performance of the investors that make up the active segment of a market will exceed the average performance of the investors that make up the passive segment, by an amount equal to the market-making profits that the active segment earns in providing liquidity to the passive segment.

With this law in hand, we are now in a position to answer the four questions posed at the outset.

First, what necessary functions does active management perform in a financial system?

Answer: The function of providing liquidity to the market, specifically to the passive segment, and to companies seeking funding. In seeking to fulfill that function profitably, the active segment ends up providing the other functions of ensuring that new investment capital is correctly allocated and that existing assets get correctly priced, functions that Indexville had to pay for separately, because it lacked an active segment.

The provision of this liquidity obviously comes at a cost, the cost of doing the work necessary to know how the flows of the passive segment are likely to unfold, and also the work necessary to ascertain the underlying value of the existing securities being traded and the new investment opportunities being pursued.

Second, what is the optimal amount of active management to have in a financial system, to ensure that those functions are carried out?

Answer: The amount needed to ensure that adequate liquidity is provided to the market, specifically to the passive segment of the market and to companies seeking funding, assuming that the passive segment is not structured to provide that funding (as it was in Indexville). If there is adequate liquidity, prices will tend to be correct; if they are incorrect, those participants that are causing them to be incorrect will be exposed to arbitrage by other participants, which will render their liquidity provision unprofitable.

At this point it’s important to note that self-described “passive” investors are themselves the ones that determine how much active management will be needed. If the segment of the market that is proudly calling itself “passive” right now is only going to embrace “passivity” while things are good, morphing itself into an active, speculative, market-timing operation as soon as things turn sour, then a large number of active investors will be needed to come bail it out. As a group, those active investors will get the opportunity to earn their fees and outperform. But if investors come to their senses, and take a long view similar to the one embraced in Indexville, then the market’s liquidity needs will be minimal, and a market with a small active segment will be able to function just fine.

Third, if the size of the market’s active share falls below the optimal level, how will we know?

Answer: The market will show signs of not having enough liquidity.

If there is an insufficient amount of active management in the system, then whenever the passive segment introduces a net flow, prices will take on wild swings, and will become substantially disconnected from fair value. The problem, however, will be self-correcting, because there will then be a greater financial incentive for investors to go active and take advantage of the lucractive reward being offered for providing liquidity. The active segment as a whole will see stronger performance.

Fourth, how much can active managers, as a group, reasonably charge for their services, without acting as a net drag on the system?

Answer: An amount equal to the excess profit that they are able to earn in providing liquidity to the market, specifically to passive investors and companies seeking funding.

The active segment needs to earn its fees. If it can’t earn its fees, then there will always be an arbitrage opportunity putting pressure on its size. Investors will be able to get higher returns by going passive, and that’s what they’ll do.

The only way the active segment, as a group, can earn its fees, is by providing liquidity to the market, specifically to the passive segment, and to corporations seeking new funding. Of course, the active segment can trade with itself, attempting to arbitrage its own mistakes in that effort, but for every winner there will be a loser, and the net profit for the group will be nothing. Any fees charged in the ensuing cannibalization will represent a loss to investors relative to the alternative–which is to simply go passive.

In terms of the larger benefit to society, the cannibalization may cause prices to become more “correct”, but how “correct” do they need to be? And why does their “correctness” require such an enormous and expensive struggle? Recall that in Indexville we were able to buy a decent substitute for the struggle–a 20,000-person army of highly talented analysts valuing the market–for a tiny fraction of the cost.

If we shrink down the size of the active segment of the market, it becomes easier for that segment to earn its fees through the liquidity that it provides–which it has to do in order to collapse the arbitrage, particularly if its fees are going to remain high as a percentage of its assets. That is the path to an equilibrium in which active and passive generate the same return, net of fees, and in which there is no longer a reason to prefer one over the other.

Summary: Putting Everything Together

The points that I’ve tried to express in this piece are complex and difficult to clearly convey. So I’m going to summarize them in bullet points below:

- The right size of the active segment of the market is the size that allows it to earn whatever fees it charges. If it cannot earn those fees, then there will always be an arbitrage opportunity putting pressure on its size. Investors will be able to get higher returns by going passive, and so that’s what they’ll do.

- The only way the active segment, as a group, can earn its fees, is by providing liquidity to the market, specifically to the passive segment, and to corporations seeking new funding. All other profits for the segment will be zero-sum.

- The question that determines the necessary amount of active management is this: how much natural passive flow is there in the system, i.e., non-speculative flow associated with people wanting to save excess income, or wanting to consume out of savings, or wanting to alter their risk allocations, given changes in their ages? Similarly, what is the natural corporate demand for funding? That flow, and that demand for funding, represents active management’s potential market for the provision of liquidity. Relative to the actual volume that takes place in the current market, it is minimal.

- If the investing ethos evolves such that market participants become decreasingly inclined towards active behaviors–i.e., if they learn their lessons, and stop making trades for speculative reasons, and instead take the sage advice of a Bogle, or a Malkiel, or a Fama to limit their interventions to cases where they have legitimate non-speculative reasons for modifying their portfolios–then the active segment will have to shrink dramatically from its current size. Either that, or it will have to shrink its fees.

- At some point in the above scenario–which, to be clear, is the Indexville scenario–the system will get to down to some bare-bones minimum level of active management, a level at which active managers, as a group, will be small enough to earn excess profits that are sufficient to cover the percentage-based fees they charge. Where is that minimum level? In my view, far away from the current level, at least at current fee rates. If I had to randomly guess, I would say somewhere in the range of 5% active, 95% passive. If we include private equity in the active universe, then maybe the number is higher–say, 10% active, 90% passive.

- On the other hand, if we assume that the trend towards “passive investing” is simply about investors in the current bull market falling in love with $SPY or $VFIAX given the recent performance of U.S. equities, rather than about investors actually committing to the advice of a Bogle, or a Malkiel, or a Fama–then the future liquidity that those investors will consume when they change their minds will provide opportunities for what we’re calling the “active segment” to step in and earn its fees. But this point will be purely definitional, because the investors we are calling “passive”, though technically passive relative to the S&P 500, will not have been genuinely passive at all, in terms of the spirit of what that term means. They will have been active investors operating in guise, who just-so-happened to have been using index-based instruments in their efforts.