U.S. equity index funds have grown dramatically in recent decades, from a negligible $500MM in assets in the early 1980s to a staggering $4T today. The consensus view in the investment community is that this growth is unsustainable. Indexing, after all, is a form of free-riding, and a market can only support so many free-riders. Someone has to do the fundamental work of studying securities in order to buy and sell them based on what they’re worth, otherwise prices won’t stay at correct levels. If too many investors opt out of that work, because they’ve discovered the apparent “free lunch” of a passive approach, active managers will find themselves in an increasingly mispriced market, with greater opportunities to outperform. These opportunities will attract funds back into the actively-managed space, reversing the trend. Or so the argument goes.

In this piece, I’m going to challenge the consensus view. I’m going to argue that the trend towards passive management is not only sustainable, but that it actually increases the accuracy of market prices. It does so by preferentially removing lower-skilled investors from the market fray, thus increasing the average skill level of those investors that remain. It also makes economies more efficient, because it reduces the labor and capital input used in the process of price discovery, without appreciably impairing the price signal.

The Irrelevance of Passive Share: A Concrete Example

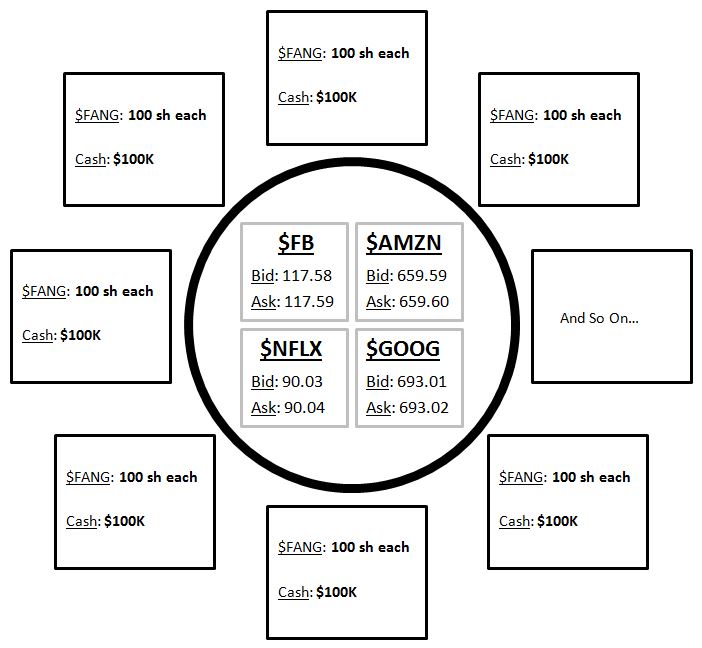

There’s an important logical rule that often gets missed, or at least misunderstood, in discussions on the merits of active and passive management. The best way to illustrate that rule is with a concrete example. Consider a hypothetical market consisting of 100 different individual participants. Each participant begins the scenario with an initial portfolio consisting of the following 5 positions:

- 100 shares of Facebook ($FB)

- 100 shares of Amazon ($AMZN)

- 100 shares of Netflix ($NFLX)

- 100 shares of Google ($GOOG)

- $100,000 in cash.

We assume that these financial assets represent all financial assets in existence, and that the market is closed, meaning that new financial assets cannot enter or be created, and that existing financial assets cannot leave or be destroyed. With each participant in possession of her initial portfolio, we open the market and allow trading to take place.

Now, in the first scenario, we assume that 10 out of the 100 participants choose to take a passive approach. These participants recognize that they lack the skill necessary to add value through trading, so they opt to simply hold their initial portfolios as received. The other 90 participants choose to take an active approach. They conduct extensive fundamental research on the four underlying companies, and attempt to buy and sell shares based on their assessments of value. Naturally, their assessments change as new information is received, and so the prices change.

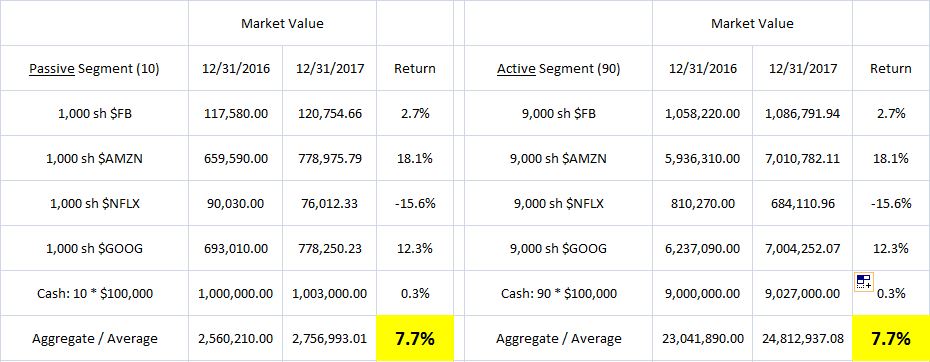

Suppose that we mark the price of each security to market on December 31, 2016 and then again on December 31, 2017.

(Note: these prices do not represent predictions or investment advice)

We use the prices to determine the aggregate and average returns of the passive and active segments of the market. The result:

As the table shows, the returns of the active and passive segments of the market end up being identical, equal to 7.7%. The reason the returns end up being identical is that the two segments are holding identical portfolios, i.e., portfolios with the same percentage allocations to each security. The allocations were set up to be the same at the outset of the scenario, and remain identical throughout the period because the two segments do not trade with each other. Indeed, the two segments cannot trade with each other, because the passive segment has decided to stay passive, i.e., to not trade.

To be clear, the individual members of the active segment do trade with each other. But their trades are zero-sum–for every share that an active investor buys, some other active investor is selling those exact same shares, and vice-versa. Consequently, the aggregate “position” of the active segment stays constant at all times. Because that position was initially set to be equal to the aggregate position of the passive segment, it stays equal for the entire period, ensuring that the aggregate returns will be equal as well.

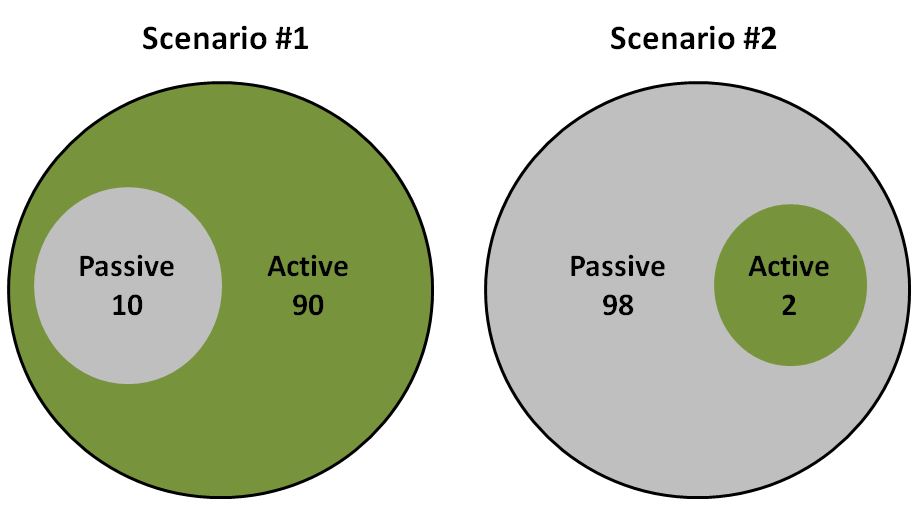

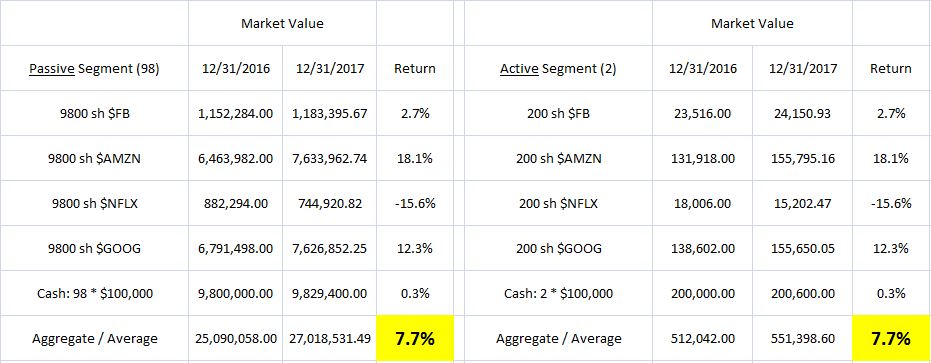

Now, the consensus view is that if too many investors try to free-ride on a passive strategy, that the securities will become mispriced, creating opportunities for active investors to outperform. To test this view, let’s push the scenario to an extreme. Let’s assume that in the second scenario 98 of the investors initially opt to remain passive, with only two opting to trade actively.

Will the decrease in the number of active investors–from 90 in the first scenario down to 2 in the second–make it any easier for those investors to outperform as a group? Not at all. The two investors that make up the active segment are going to have trade with each other–they won’t have anyone else to trade with. Regardless of how they trade, their combined portfolios will remain identical in allocation to the combined portfolios of the 98 investors that are passively doing nothing. The performances of the two segments will therefore remain the same, just as before. This fact is confirmed in the table below, which shows both segments again earning 7.7%:

The Law of Conservation of Alpha

The prior example illustrates a basic logical rule that governs the relationship between the aggregate performances of the active and passive segments of any market. I’m going to call that rule “The Law of Conservation of Alpha.” It’s attributable to Eugene Fama and William Sharpe, and can be formally stated as follows:

The Law of Conservation of Alpha (Aggregate): The aggregate performance of the active segment of a market will always equal the aggregate performance of the passive segment.

Importantly, this rule applies before frictions are taken out–management fees, transaction costs, bid-ask spread losses, taxes, and so on. Because the passive segment of a market tends to experience less friction than the active segment, the passive segment will typically outperform the active segment.

Now, the aggregate return of a group and the (asset-weighted) average return of each member of that group are essentially the same number. We can therefore reframe the rule in terms of averages:

The Law of Conservation of Alpha (Average): Before fees, the average performance of the investors that make up the active segment of a market will always equal the average performance of the investors that make up of the passive segment.

The terms “active” and “passive” need to be defined. An “active” allocation is defined as any allocation that is not passive. A “passive” allocation is defined as follows:

Passive Allocation: An allocation that holds securities in relative proportion to the total number of units of those securities in existence.

Crucially, the term “passive” only has meaning relative to a specific universe of securities. The person using the term has to specify the securities that are included in that universe. In our earlier example, the universe was defined to include all securities in existence, which we hypothetically assumed to be $10MM U.S. dollars and 10,000 shares each of four U.S. companies–Facebook, Amazon, Netflix and Google. In the real world, many more securities will exist than just these. If we were to define the term “passive” to include all of them, then a “passive” portfolio would have to include all equity shares, all fixed income issues, all money in all currencies, all options, all warrants, all futures contracts, and so on–each in proportion to the total number of units outstanding. And if we were to include non-financial assets in the definition, a “passive” portfolio would have to include all real estate, all precious metals, all art work, and so on–anything that has monetary value unrelated to present consumption. The problem of determining the true composition of the “passive” segment of the market would become intractable, which is why we have to set limits on the universe of securities that we’re referring to when we speak of a “passive” approach.

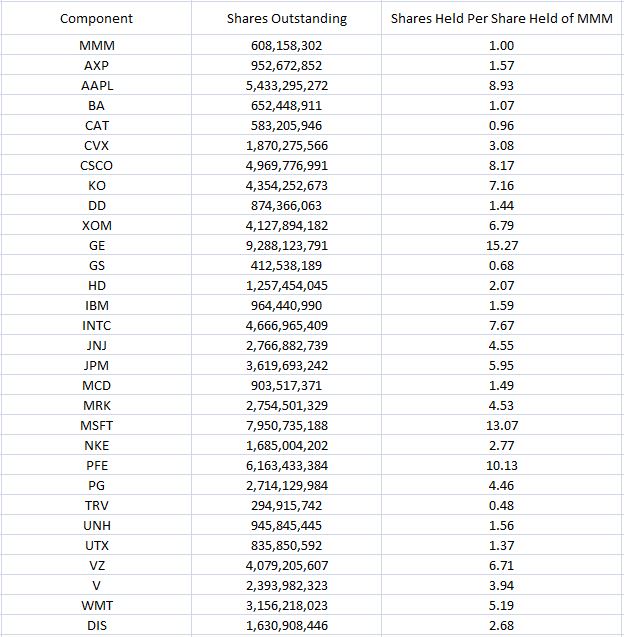

To illustrate how we would build a passive portfolio, let’s focus on the universe of the 30 companies that make up the Dow Jones Industrial Average (“The Dow”). To establish a passive allocation relative to that universe, we begin by quantifying the total number of existing shares of each company. We then arbitrarily pick a reference company–in this case, 3M ($MMM)–and calculate the respective ratios between the number of shares outstanding of each company and that company, $MMM. The ratios will determine the relative number of shares of each company that we will hold (see the right column below):

You can see in the chart that Home Depot ($HD) has 2.07 times as many shares outstanding as $MMM. So, in our passive portfolio, we hold 2.07 times as many shares of $HD as $MMM. And 6.79 times as many shares of Exxon-Mobil ($XOM). And 13.07 times as many shares of Microsoft ($MSFT). And so on.

Note that this formula doesn’t specify the absolute number of shares of each company that we would need to hold in order for our portfolio to be “passive.” Rather, it specifies the relative ratio of number of shares of each company that we would need to hold. In practice, we will choose the absolute number of shares that we hold based on the amount of wealth that we’re trying to invest in the passive strategy.

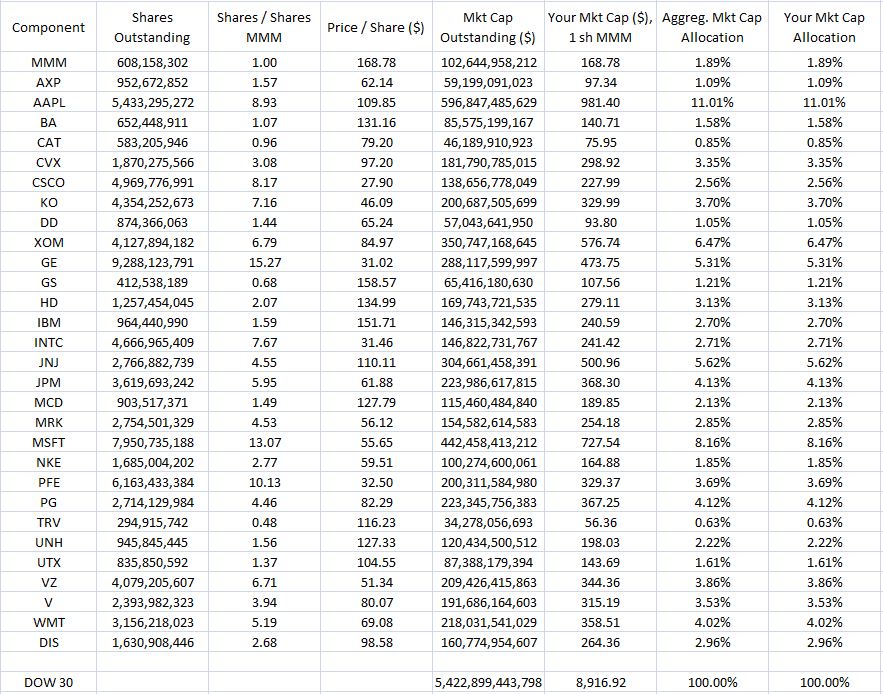

Now, mathematically, if we hold a share count of each security that is proportionate to the total number of shares in existence, we will also end up holding a market capitalization of each security–share count times price–that is proportionate to the total amount of market capitalization in existence. This will be true regardless of price, as illustrated in the table below:

The table assumes you hold 1 share of $MMM, and therefore, by extension, 1.57 shares of American Express ($AXP), 8.93 shares of Apple ($AAPL), 1.07 shares of Boeing ($BA), and so on. The prices of these securities determine both your allocation to them, and the aggregate market’s allocation to them, where “allocation” is understand in terms of market capitalization. In the table above, the allocations–for both you and the market–end up being 1.89% to $MMM, 11.01% to $AAPL, 1.58% to $BA, and so on.

Obviously, prices will change over time. The changes will cause changes in the aggregate market’s percentage allocation to each security. But you won’t need to worry about those changes, because they will pass through to your allocation as well. The price changes will affect your allocation in the exact same way that they affect the aggregate market’s allocation, ensuring that the two allocations remain identical in market capitalization terms–provided, of course, that you remain passive and refrain from trading.

A passive strategy is special because it is the only type of strategy that can remain in place in the presence of price changes without requiring investor action. No other investment strategy is like that–value, momentum, pre-defined allocation, etc.–these strategies all require periodic “rebalancing” in order to preserve their defining characteristics. A value portfolio, for example, has to sell cheap stocks that become expensive, and buy expensive stocks that become cheap, otherwise it will cease to meet the definition of “value.” A momentum portfolio has to sell high-momentum stocks that lose momentum, and buy low-momentum stocks that gain momentum, otherwise it will cease to meet the definition of “momentum.” A 60/40 stock/bond portfolio has to sell the asset class that appreciates the most, and buy the asset class that appreciates the least, otherwise it will cease to be a 60/40 portfolio, and will instead become a 63/37 portfolio, or a 57/43 portfolio, and so on. A passive portfolio, in contrast, can completely ignore any and all price changes that occur–it will remain “passively” allocated, i.e., allocated in proportion to the overall market supply, no matter what those changes happen to be.

Accounting Complications: A Solution

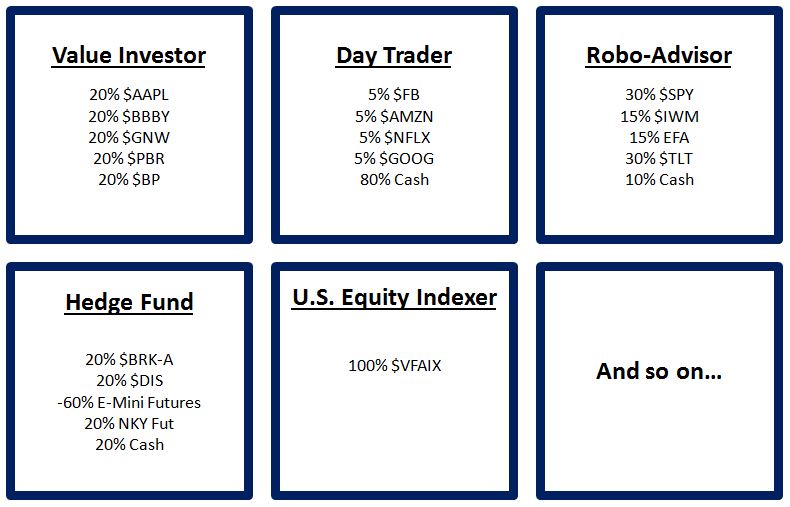

When we try to apply The Law of Conservation of Alpha to actual market conditions, we run into accounting complications. For an illustration, consider the following sample of portfolios in the market:

How exactly would one go about applying the Law of Conservation of Alpha to these portfolios? Recall the law itself:

The Law of Conservation of Alpha (Average): Before fees, the average performance of the investors that make up the active segment of a market will always equal the average performance of the investors that make up of the passive segment.

Look closely at the U.S. Equity Indexer’s portfolio. The single position is expressed passively through an S&P 500 mutual fund, $VFIAX. We might therefore call it “passive.” But it clearly isn’t “passive” with respect to the overall universe of existing securities, as there are many more securities in the world than just the equities contained in the S&P 500.

Of course, if we limit our universe to S&P 500 equities, then the U.S. Equity Indexer’s portfolio is passive (relative to that universe). According to the Law of Conservation of Alpha, the portfolio’s performance will match the average performance of active managers that play in that same universe, i.e., active managers that own stocks in the S&P 500. The problem, of course, is that the investment community cannot be cleanly separated out into “active managers that own stocks in the S&P 500.” Many of the managers that own stocks in the S&P 500 universe, such as the Value Investor shown above, also own securities that do not fall into that universe. In aggregate, their portfolios will not be identical to the S&P 500 in terms of allocation, and therefore the performances will not match.

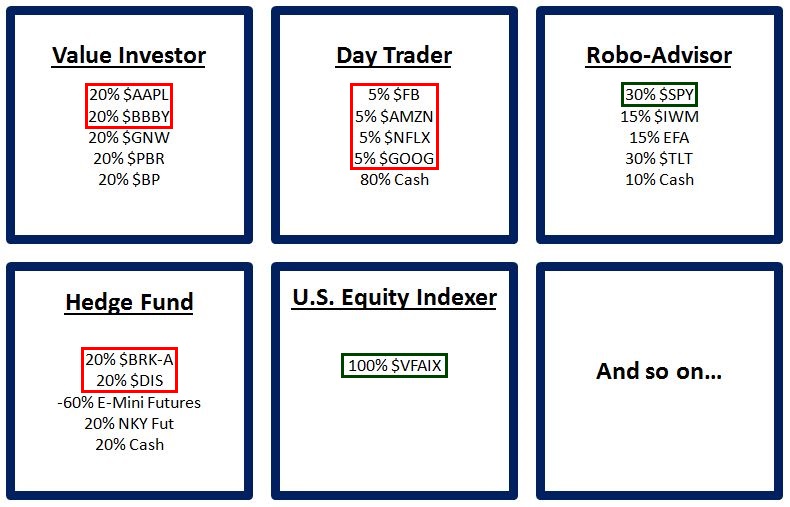

Fortunately, there’s a way around this problem. If our universe of concern is the S&P 500, then, to apply The Law of Conservation of Alpha to that universe, we identify all portfolios in the market that hold positions in S&P 500 constituents, long or short. Inside each of those portfolios, we group the positions together, bracketing them out as separate entities with their own separate performances–“S&P 500 component funds” whose returns can be evaluated independently. To illustrate, the S&P 500 component funds for the above portfolios are boxed in the image below:

To be clear, what we’re doing here is taking the securities in each portfolio that fall inside the S&P 500, and conceptually bracketing them out as separate vehicles to be analyzed–separate S&P 500 component funds to be tracked. Some of the S&P 500 component funds in the group–for example, that of the U.S. Equity Investor who holds $VFIAX, and that of the Robo-Advisor who holds $SPY–are passively allocated relative to the S&P 500. The allocations of those funds are identical to the allocation of the S&P 500, which is why we’ve boxed them in green. Similarly, other S&P 500 component funds–for example, that of the Day Trader whose only S&P 500 holdings consist of Facebook, Amazon, Netflix, and Google, in equal market cap proportion–are actively allocated relative to the S&P 500. The allocations of those funds actively deviate from the allocation of the S&P 500, which is why we’ve boxed them in red.

We can reframe the Law of Conservation of Alpha in terms of component funds as follows:

The Law of Conservation of Alpha (Average, Component-Basis): For a given universe of securities, the average performance, before fees, of all active component funds associated with that universe will always equal the average performance, before fees, of all passive component funds associated with that universe.

Put simply, what the law is saying is that if we properly identify and delineate the active and passive component funds of a given universe in every portfolio, summing the active together and the passive together, the respective allocations to each security of the active and passive sums will be equal at all times. It follows that the aggregate returns of the active and passive sums will be equal, before fees.

The Impact of Net Fund Flows

Consider the Vanguard S&P 500 index fund, $VFIAX. What happens when it receives a net cash inflow? The answer: it ceases to be allocated passively relative to the S&P 500. It ends up owning cash, a security not contained in the S&P 500. To become passive again, it has to go into the market and trade that cash for S&P 500 shares, in exact proportion to the amount in existence. Until it does that, it will technically be in an active stance.

By coincidence, when it goes into the market, it may end up making the purchases from other S&P 500 index funds that are experiencing equivalent net cash outflows. If that happens, then the transactions will be a wash for the passive segment of the market, and can be ignored.

If, however, there aren’t matching S&P 500 index fund outflows for it to pair up with and offset, then it will have to transact with the active segment of the market. It will have to go into the market and buy shares from the active segment, becoming the active segment’s counterparty. Whenever the two segments of the market–active and passive–become counterparties to each other, the previous logic ceases to apply. It becomes possible for the active segment of the market to outperform the passive segment, in what might seem like a contradiction of The Law of Conservation of Alpha.

Importantly, The Law of Conservation of Alpha is only meant to apply once a passive portfolio has already been established. If a passive portfolio is in place, and stays in place continuously for a period (because the passive investor refrains from trading), then the performance of the passive portfolio during that period will match the aggregate performance of the market’s active segment during that period. The performances need not match in periods before the passive portfolio is established, or in periods after the passive portfolio has been lost through cash inflows and outflows.

So there you have the exception to the rule. The performances of the active and passive segments of the market can deviate during those periods in which the passive segment is not truly passive. In practice, however, such deviations will be small, because index funds act reasonably quickly to preserve their passive stance in response to net inflows and outflows–too quickly for the index to move away from them in either direction. What they primarily lose to the active segment is the bid-ask spread. Each time they buy at the ask, and sell at the bid, they give half of the associated spread to the active segment of the market, which includes the market makers that are taking the other sides of their orders. The loss, however, tends to be miniscule, or at least easily offset by the other profit-generating activities that they engage in (e.g., securities lending), evidenced by the fact that despite having to deal with large flows, index funds have done a fantastic job of tracking their “pure” indexes. To offer an example, $VFIAX, the world’s largest passive S&P 500 index mutual fund, has tracked the S&P 500 almost perfectly over the years, which is why you only see one line in the chart below, when in fact there are two.

Now, to be clear, large net inflows and outflows into index funds can certainly perturb the prices of the securities held in those funds. And so if, tomorrow, everyone decided to buy $VFIAX, the prices of S&P 500 companies would surely get bid up by the move. But the situation would be no different if investors decided to make the same purchase actively, buying actively-managed large cap U.S. equity funds instead of $VFIAX. The perturbation itself would have nothing to do with the passive structure of $VFIAX, and everything to do with the fact that people are attempting to move funds en masse into a single asset class, U.S. equities. Relative to the universe of all securities, that’s a decidedly “not passive” thing to do.

The key difference between using $VFIAX to buy large cap U.S. equities, and using actively managed funds for the same purpose, lies in the effect on the relative pricing of S&P 500 companies. The use of $VFIAX does not appreciably affect that pricing, because an equal relative bid is placed on everything in that index. The use of actively managed funds, in contrast, does affect the relative pricing, because the relative bid on each company in the index will be determined by which names in the index the active managers who receive the money happen to prefer.

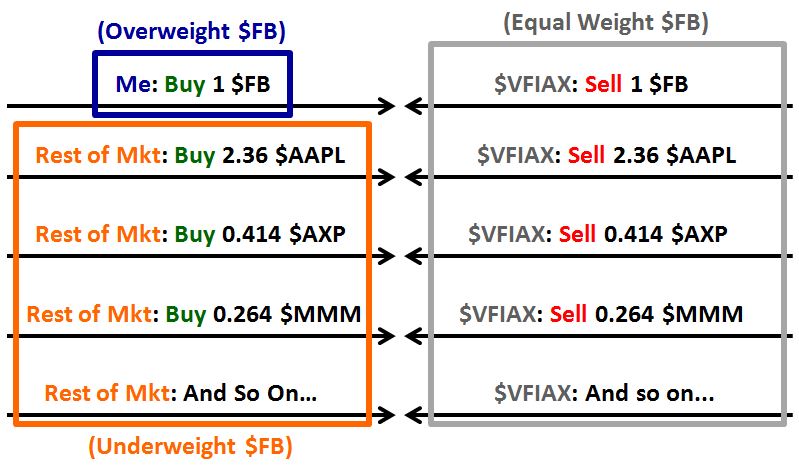

Intuitively, people tend to get hung up on the idea that index funds could somehow be counterparties to active managers, and yet continue to track the aggregate performances (before fees) of those same active managers. The hangup is best illustrated with an example. Suppose that I have perfect market clairvoyance, and know, with certainty, that $FB is going to double over the next year. Obviously, I’m going to go into the market and buy as much $FB as I can. Suppose that in the actual transaction that ensues, I end up buying $FB from an S&P 500 index fund–say, $VFIAX–that happens to be experiencing a redemption request, i.e., a cash outflow.

When I buy $FB from $VFIAX, and $FB goes on to double, I’m obviously going to end up outperforming the S&P 500. Who, then, is going to underperform the S&P 500? Secondary market transactions are zero-sum games for the participants, so if I’m going to outperform, someone will have to underperform. The temptation is to say that $VFIAX is going to underperform, since it’s the one that’s foolishly selling the undervalued $FB shares to me. But, to the extent that $VFIAX is maintaining a passive stance, it’s going to handle the cash outflow by also selling all other stocks in the S&P 500, in exact relative proportion to the number of shares that exist. For every 1 share of $FB that it sells to meet the redemption, it’s also going to sell 2.36 shares of $AAPL, 0.414 shares of $AXP, 0.264 shares of $MMM, and and so on, all in order to preserve its passive allocation relative to the S&P 500. To the extent that it successfully preserves that allocation, its performance will continue to track the S&P 500’s performance.

Who, then, will underperform the S&P 500, to offset my outperformance? The answer: the rest of the active market. When $VFIAX sells the 500 stocks in the S&P 500, and I preferentially buy all the $FB shares that it’s selling, the rest of the active market will end up not buying those shares. It will be forced to buy all of the other names in the S&P 500 that $VFIAX is selling, with $FB left out. The rest of the market will therefore end up underweighting $FB relative to the S&P 500, offsetting my overweight. When $FB goes on to double, the rest of the market will therefore underperform relative to the S&P 500, offsetting my outperformance.

The example demonstrates that in a liquid market, passive index funds can easily do what they need to do, making the transactions that they need to make in order to maintain their passivity, without perturbing relative prices. If I try to overweight $FB and underweight everything else, then, in a normal market environment, the price of $FB should get bid up relative to everything else. That’s exactly what’s going to happen in the above example, because I will be removing the selling pressure that the $VFIAX outflow is putting on $FB, without removing the selling pressure that the $VFIAX outflow is putting on everything else. The $VFIAX outflow is entirely transparent to the market’s relative pricing mechanism, leaving prices just as they would have been in its absence.

Now, to be clear, in an illiquid market, with large bid-ask spreads, all bets are off. As we noted earlier, when a passive index fund receives inflows and outflows, and has to transact with the active segment to maintain its passive stance, it loses the bid-ask spread. If that spread is large, then there’s a viable pathway for active managers–specifically market-makers–to outperform at the passive fund’s expense.

The Impact of New Share Issuance and Share Destruction through Buybacks

A separate source of performance divergence emerges in the context of new share issuance. Suppose that a fund is employing a passive index strategy relative to the total universe of publicly traded U.S. equities–all sizes: large, medium, small, and micro. A new company then conducts an initial public offering (IPO). That company will immediately be part of the universe of publicly-traded equities. To maintain its passive allocation relative to that universe, the index fund in question will need to obtain a proportionate number of shares of the company. There may be a delay–potentially a significant one–between the time that the IPO occurs and the time that the fund actually obtains the shares. That delay will create a window for the fund’s performance to deviate from the performance of the market’s active segment.

Whether this type of divergence will result in outperformance or underperformance for index funds will depend on how newly issued securities tend to perform during the periods between their issuances and their entries into the index funds. If, as a group, newly issued securities tend to perform better than the rest of the market during those periods, then index funds will underperform the market accordingly. If, as a group, they tend to perform worse than the rest of the market during those periods, then passive funds will outperform the market accordingly.

Most passive funds have lower-limits on the market capitalizations of securities they hold–they only take in new companies when those companies reach certain sizes and levels of liquidity. The temptation is to therefore conclude that such funds will tend to underperform the active segment of the market, given that they are only buying newly issued securities after those securities have appreciated substantially in price, with the appreciation having accrued entirely to the gain of the active segment of the market that holds them in their infancy. This conclusion, however, ignores all of the newly issued securities that perform poorly after issuance. Passive funds are able to avoid the losses that those securities would otherwise inflict.

In terms of the impact on index performance relative to the market, what matters is not how newly issued securities that successfully make it into indices perform relative to the market, but how all newly issued securities perform relative to the market, including those that never make it into indices. In theory, we should expect newly issued securities to be priced so that their average performances end up roughly matching the average performance of the rest of the market, otherwise capitalist arbitrage would drive the market to issue a greater or lesser number of those securities, forcing a price adjustment.

Now, share buybacks create a similar challenge, but in reverse. If a company buys back its shares and retires them, then, to stay passively-allocated, an index fund that holds the shares is going to have to adjust its allocation accordingly–it’s going to have to sell down the position, and proportionately reallocate the proceeds into the rest of the index. The period prior to that adjustment will represent a window in which the fund is officially no longer passively-allocated, and in which its performance will have the potential to diverge from the performance of the market’s active segment. Whether the divergence will amount to outperformance or underperformance will depend on how companies perform relative to the rest of the market shortly after share buybacks occur.

To summarize, net flows, new share issuance and share destruction through buybacks can, in theory, create divergences between the performances of the passive and active segments of the market. But there’s little reason to expect the divergences to have a sizeable impact, whether favorable or unfavorable. In terms of a concrete application of the Law of Conservation of Alpha, they can typically be ignored.

Flawed Comparisons: Apples to Apples, Oranges, and Grapes

The theory here is well-understood, but when we compare the average performance of active funds over the last 10 years to the average performance of index funds over the same period, we find that active funds have somehow managed to underperform their passive counterparts by more than their cost differentials. Given the Law of Conservation of Alpha, how is that possible?

The answer, again, relates to inconsistencies in how asset universes get defined in common parlance, particularly among U.S. investors. When investors in the United States talk about the stock market, they almost always mean the S&P 500. But active equity funds routinely hold securities that are not in that index–small-caps, foreign companies, and most importantly, cash to meet redemptions. In an environment such as the current one, where the S&P 500 has dramatically outperformed these other asset classes, it goes without saying that active funds, which have exposure to the asset classes, are going to underperform in comparison. But this result says nothing about active vs. passive, as the comparison itself is invalid.

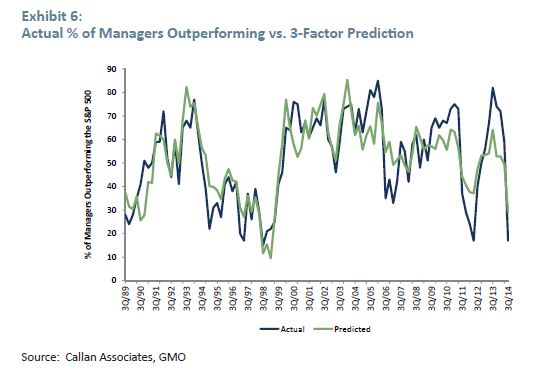

In a brilliant essay from last year, Neil Constable and Matt Kadnar of GMO proved the point empirically. They showed that the percentage of active large cap managers who outperform the S&P 500 is almost perfectly correlated with the relative outperformance of foreign equities, small-caps, and cash–the three main ex-S&P 500 asset classes that active large cap managers tend to own. The following chart, borrowed from their essay, illustrates:

If we clean up the discussion, and examine exposures on a component basis, we will find that the average active S&P 500 component fund in a portfolio–i.e., the average grouping of strictly S&P 500 companies inside a portfolio–performs the same, before fees, as the average passive S&P 500 index fund. This is always be true, no matter what the S&P 500 index or any other index happens to be doing.

But Who Will Set Prices?

Active investors set prices in a market. Passive investors can’t set prices, because they don’t trade securities on a relative basis. They hold all securities equally, in relative proportion to the total quantity in existence. They only make relative trades in those rare instances in which market activity forces them to–e.g., in response to new share issuance or share destruction through buybacks.

An efficient market needs active investors to be the ones setting prices, because active investors are the ones doing the fundamental work necessary to know what the securities themselves are actually worth. For this reason, we tend to be uncomfortable with the idea that a market could function properly if the majority of its investors decided to go passive. We worry that the active investors in such a market wouldn’t be able to control enough money and flow to effectively do their jobs.

Setting price in a market, however, isn’t about controlling a certain amount of money or flow. It’s simply about placing an order. If all other players in a market have opted to be passive and not place orders, then “price” for the entire market can effectively be set by the single individual investor who does place an order, no matter how small she may be in size.

Why Passive Investing Increases the Market’s Efficiency

The view that passive investing undermines market efficiency is intuitively appealing and therefore widespread. To quickly see the wrongness in the view, we need only ask ourselves the following question: is it any easier for a well-trained active stock-picker to beat the market today than it was in the early 1980s? By “well-trained”, I mean “well-trained” relative to the state of industry knowledge at the time. The answer, obviously, is no. It’s just as hard to beat the market today as it was back then–in fact, by the results alone, we might think that it’s actually harder. Yet the share of the market that is allocated passively has increased dramatically in the intervening period, a fact that is entirely inconsistent with the claim that passive indexing undermines market efficiency.

As it turns out, a much stronger argument can be made in favor of the view that passive investing increases market efficiency. Before I present the argument, let me first say a few things about the concept of “market efficiency.”

We define an efficient market as follows:

Efficient Market: For a given group of securities, a market is efficient with respect to that group if all securities in the group are priced to offer the same expected risk-adjusted future returns. In a broader sense, a market is unqualifiedly efficient if all of the securities traded within it are priced to offer the same expected risk-adjusted future returns.

To use an example, the group of 500 securities that comprise the S&P 500 represent an “efficient market” to the extent that every security in that group–$AAPL, $FB, $MMM, $XOM, and so on–is priced to offer the same expected risk-adjusted future return as every other security in the group. More broadly, the collection of assets that comprise the overall asset universe–all stocks, bonds, all cash, all real-estate, everywhere–represent an “efficient market” to the extent that every asset in existence is priced to offer the same expected risk-adjusted future return as every other asset in existence–admittedly, a very high hurdle.

Empirically, the test for an efficient market is straightforward: can an investor consistently outperform the average of a market by selectively picking individual securities in the market to preferentially own? If the answer is yes, then, necessarily, the individual securities in the market are not priced to offer the same expected risk-adjusted future returns, and therefore the market is not efficient. It’s important to emphasize the word “consistent” here, as returns have a random component. An investor in an efficient market can always make a lucky pick. What an investor in an efficient market cannot do is reliably make such a pick over and over again.

The way that a market becomes efficient is through arbitrage. If, for example, a given individual security in a market is offering a more attractive risk-adjusted future return than all of the other securities, and if investors know this, then they will try to buy that security, selling the others as necessary to raise funds. But not everyone can own the security in question, and therefore its price in the market will rise. As its price rises, its expected risk-adjusted future return will fall, bringing that return into congruence with the rest of the market.

We can think of this process as happening in two specific stages: source mistake and corrective arbitrage.

- Source Mistake: The source mistake stage occurs when investors make trades that are fundamentally incorrect, e.g., when investors willingly buy securities at prices substantially above reasonable fair value, or willingly sell securities at prices substantially below reasonable fair value. An example: investors might grow psychologically anchored to the historical price level of a given stock, rigidly assessing the attractiveness of the stock’s current price relative to that level, without considering fundamental changes that might have recently taken place, such as important news that might have recently been released.

- Corrective Arbitrage: The corrective arbitrage stage occurs when other investors exploit the consequences of source mistakes for profit. To use the above example: a separate group of savvy investors might come to realize that investors in general are failing to adequately incorporate recent news into their bids and offers. Those investors might then implement strategies to take advantage of the source mistake–e.g., they might put in place systematic plans to quickly buy up companies after they release apparent good news, selling them as their prices rise, and quickly short companies after they release apparent bad news, covering them as their prices fall.

The ability of a market to attain efficiency depends on (1) the quantity and severity of source mistakes that its investors are committing, and (2) the amount and quality of corrective arbitrage that its investors are practicing in response to those mistakes. If source mistakes are prevalent and severe, and few people are practicing corrective arbitrage in response to them, then the market will be less efficient, easier for a given active investor to beat. If, however, source mistakes are rare and insignificant, and a large portion of the market is already attempting to arbitrage them, then the market will be more efficient, harder for a given active investor to beat.

Both stages are influenced by the skill levels of participants in the market. If you raise the skill level of the participants, you will reduce the quantity and severity of source mistakes that occur, and you will increase the amount and quality of the corrective arbitrage, making the more efficient and harder to beat. If you lower the skill level of the participants, you will do the opposite, making the market less efficient and easier to beat.

With respect to the potential impact of passive investing on market efficiency, the question that matters is this: does passive investing affect the “average” skill level of the active segment of the market? In my view, the answer is yes. It increases that skill level, and therefore makes the market more efficient.

How does passive investing increase the “average” skill level of the active segment of the market? The answer: by removing lower-skilled participants, either by giving those participants a better option–i.e., the option of indexing–or nudging the wealth they’re ineptly managing into that option, putting them out of business.

In a world without indexing, uninformed investors that want exposure to a given market–e.g., retail investors that want exposure to U.S. equities, or hedge fund managers that want exposure to Brazilian equities–have to go into the market themselves and make “picks.” Either that, or they have to “pick” managers to make “picks” for them. Their “picks”–whether of individual stocks or of individual managers–are likely to be uninformed and unskilled relative to the picks of those that have experience in the market and that are doing the fundamental work necessary to know where the value is.

The option of investing in a low-cost index is impactful in that it allows investors to gain their desired exposures without having to make what would otherwise be unskilled, uninformed picks. It allows them to own the market that they want to own, without forcing them to introduce their lack of skill into the market’s active segment. In this way, it increases the average skill level of the market’s active segment, making the market more efficient, more difficult to beat.

A similar point applies to the Darwinian pressure that indexing places on active fund management businesses. The growth in indexing has to come from somewhere. Where is it most likely to come from? The answer: from actively managed funds that are consistently underperforming. If you believe in skill, then you will probably agree that those funds are more likely to lack skill than funds that are consistently outperforming. In removing them, pressuring them out of business, indexing inadvertently increases the average skill level of the active funds that remain, again making the market more difficult to beat.

It’s important to remember, here, that secondary market trading and investing is a zero-sum game for the participants. For a given market participant to outperform, some other market participant has to underperform. Obviously, for a market participant with a given level of skill, the ease at which that participant will outperform will be a function of the quantity of unskilled participants that are there for the skilled participant to exploit. To the extent that the prevalence of indexing preferentially reduces that quantity, it makes outperformance more difficult.

To summarize the point, indexing preferentially removes inexperienced, uninformed investors from the market, giving them a superior option–superior for them, because if they were to get into the fray, they would likely underperform. It also preferentially undermines the businesses of low-skill managers that fail to produce adequate results and that lose business to index competition. In this way, indexing concentrates the active share of the market into a select group of highly-skilled managers. As an active market participant, you are no longer able to do battle with low-skill participants, and are instead forced do battle with them. Think: the Bridgewaters, Third Points, Appaloosas, Bauposts, and GMOs of the world, just as examples. If you think it will be easier to outperform in a market where these entities are your primary counterparties, as opposed to a market where their presence has been diluted by a flood of run-of-the-mill managers and retail investors that don’t know what they’re doing, you’re crazy.

Now, to be clear, the increased market efficiency that comes with the growth of indexing can only manifest itself in those specific areas of the market where indexing actually becomes popular–e.g., in the U.S. large cap equity space, where a staggering 34% of all shares are being held in index funds. It’s not, however, going to manifest itself in broader areas where passive approaches remain unpopular. Investors are quite willing to gain U.S. equity exposure passively through index funds such as $SPY and $VFIAX, but they don’t seem to be willing to extend the same passive discipline to the overall universe of assets. Doing so would require them to hold stocks, bonds, and cash from around the globe in proportion to the amounts outstanding. Who wants to do that? No one, and no one is going to want to do it in the future.

Going forward, then, we should expect lower-skilled players to remain active in the broader global asset allocation game–including through the controversial practice of market timing–creating opportunities for skilled investors to outperform at their expense. If there’s a place to stay aggressively active, in my view, it’s there–in global macro–definitely not in a space like large cap U.S. equities, where the passive segment is growing literally by the day.

The Grossman-Stiglitz Paradox and the Marketplace of Ideas Fallacy

In a famous paper published in 1980, Sanford Grossman and Joseph Stiglitz introduced what is called the Grossman-Stiglitz paradox. This paradox holds that market prices cannot ever be perfectly efficient, for if they were, then investors would lack a financial incentive to do the work necessary to make prices efficient.

I want to clarify how the point that I’m making fits into this paradox. To be clear, I’m not arguing that an entire market could ever go passive. If an entire market were to go passive, there would be no transactions, and therefore no prices, and therefore no market. To have a market, someone has to actively transact–i.e., put out a bid and an offer. That someone is going to have to at least believe that there is excess profit to be had in doing so.

What passive investing does is it shrinks the portion of the market that actively transacts. It therefore shrinks the portion of the market that sets prices. But it doesn’t eliminate that portion, nor does it eliminate the profit motive that would drive that portion. It simply improves the functioning of that portion, removing the unnecessary contributions of low-skilled participants from the fray.

I anticipate that a number of economists will want to resist this claim. They will want to argue that adding lots of participants to the messy milieu of stock-picking can increase market efficiency, even if the majority of the participants being added lack skill. The problem with this view, however, is that it conceptualizes the financial market as a “marketplace of ideas”–a system where, in evolutionary fashion, different ideas are continually presented, with good ideas filtering their way the top, and bad ideas filtering out. In such a system, the introduction of diversity of any kind–even if it involves a large number of bad ideas and only a small number of good ones–has a positive effect on the final product, because the good ideas get latched onto, and the bad ideas disappear without harm.

Unfortunately, that’s not how “prices” are formed in a market. Prices are formed through the individual transactional decisions of individual people. There is no sense in which the good decisions in this lot rise to the top, nor is there any sense in which the bad decisions filter out. All of the decisions impact the price, at all times. If the average skill that underlies the decisions goes down, then so too will the quality of the ultimate product–the price.

Why Passive Indexing Makes Economies More Efficient

Imagine a world in which 500,000 individuals opt for careers in the field of active investment management. In those careers, they continually compete with each other for excess profit, setting prices for the overall market in the process. Some of the participants turn out to have skill, some turn out not to have skill–but each extracts a fee, compensation for the labor expended in the effort. The benefit that the economy gets from the arrangement is a liquid market with accurate prices.

Eventually, indexing comes around to disrupt the industry. Of the 500,000 individuals that were previously managing funds, 499,500 go out of business, with their customers choosing the passive option instead. The remaining 500–which are the absolute cream of the crop–continue to compete with each other for profit, setting prices for the overall market.

Ask yourself, what real advantage does the first arrangement have over the second? Why does an economy need to have 500,000 people arbitraging the price of $AAPL, $GOOG, $FB, and so on, when 500 of the market’s most highly-skilled active investors could do the job just as well, producing a price signal that is just as accurate, without requiring the help of the rest of the pack? There is no advantage, only the disadvantage of the lost resources.

Free markets tend to naturally correct economic inefficiences. To have a very large number of highly-talented people duplicating each other’s arbitrage efforts is an inefficiency, particularly in secondary markets where the actual physical capital that underlies the securities has already been formed and will not be affected by the market price. Passive management represents its inevitable solution.

Conclusion: Can It Make Sense to Invest in an Active Manager?

We conclude the piece with the question: can it make sense to invest with an active manager? If by “active manager” we’re talking about a financial advisor, then the answer is obviously yes. A financial advisor can help otherwise financially uninformed clients avoid mistakes that have the potential to be far more costly than the fees charged, particularly if the fees charged are reasonable. They can also improve clients’ state of mind, by allowing clients to offload stressful decisions onto a trusted expert. But I’m directing the question more towards active fund managers–active stock-pickers that are trying to deliver better exposures to the market than an index fund can offer. Can it make sense to invest with those managers? In my view, the answer is also yes.

An analogy is helpful here. Like secondary-market investing, law is a zero-sum game. If you aggregate the individual performances of all civil attorneys, and you exclude cases where multiple attorneys work together in cases, the average win percentage of any given attorney will be 50%–in other words, average. Does it follow that if you could eliminate fees by using an “average” attorney, that you should do so? No, not at all. The legal universe as a whole cannot do better than the average attorney, and so if the universe of litigants as a whole can avoid fees in the conduct of its zero-sum business, then it should. But you, yourself, considered as an individual litigant seeking a claim in your favor, are not the universe of litigants. It’s perfectly conceivable that you–considered strictly as an individual case–might have the ability to find an attorney that is better than average. If you have that ability, then settling for the average would be foolish, especially if you have lot at stake.

With respect to a legal case, what you need to ask yourself is this: do you believe that you have the insight into attorney skill to pick an attorney that is better than the average attorney–and not only better, but better by an amount sufficient to justify the fees that you will have to pay for the service? Maybe, maybe not. It depends on how good you are at identifying legal skill, and on how much your preferred attorney wants to charge you. Depending on the price, betting on that attorney’s skill may be worth it.

The same is true in the arena of investing. Do you believe that you have the insight necessary to identify an active manager whose skill exceeds that of the aggregate market? More importantly, does your manager’s excess skill level, and the excess returns that will come from it, justify the fees that she’s going to charge? If the fees are north of 200 bps, then, in my view, with the exception of a select group of highly talented managers, the answer is no. Modern markets are reasonably efficient, and difficult to consistently beat. There are investors with the skill to beat them, but only the select few can do it consistently, and even fewer by such a large amount.

At the same time, many managers charge much lower fees–some as low as 50 bps, which is only 35 bps more than the typical passive fund. That differential–35 bps–is almost too small to worry about, even when stretched out over long periods of time. In my view, there are a number of active managers and active strategies that can justify it.