In this piece, I’m going to introduce a simplified model of a fund market, and then use the model to illustrate certain important concepts related to the impact of the market’s ongoing transition from active to passive management. Some of the concepts have already been discussed in prior pieces, others are going to be new to this piece.

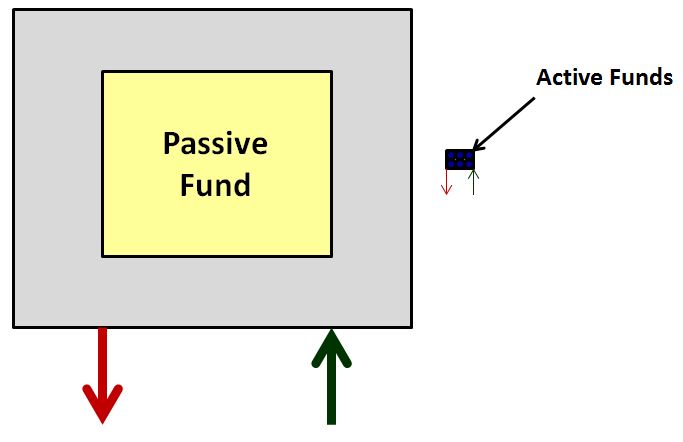

Consider, then, a hypothetical equity market that consists of shares of 5,000 publicly-traded companies distributed across 1,000 funds: 1 passively-managed index fund, and 999 actively-managed funds.

The market is characterized by the following facts:

- Share ownership by individuals is not allowed. The only way to own shares is to invest in a fund, and there are no funds to invest in other the 1,000 funds already specified. All shares in existence are held somewhere inside those funds.

- The passive fund is required to target a 100% allocation to equities over the long-term, holding shares of each company in relative proportion to the total number of shares in existence.

- The active funds are required to target a 95% allocation to equities over the long-term. They are free to implement that allocation in whatever way they want–i.e., by holding shares of whatever companies they prefer. The 95% number is chosen because it leaves the active funds with enough cash to trade, but not so much cash as to appreciably detract from their returns. Note that from here forward, when we refer to the “returns” of the active funds, we will be referring to the returns of the portion of the funds that are actually invested in the market, not the overall returns of the funds, which will include the returns of a certain amount of cash held for the purposes of liquidity.

- The passive fund and the group of 999 active funds each represent roughly half of the overall market, a fact represented in the identical sizing of the grey boxes in the schematic above.

- Each active fund charges an annual management fee of 1%. The passive fund is publicly-administered and charges no fees.

We can separate the market’s valuation into two dimensions: (1) absolute valuation and (2) relative valuation.

(1) Absolute Valuation: Valuation of the aggregate market relative to cash.

(2) Relative Valuation: Valuation of companies in the market relative to each other.

If we know these two dimensions, then, assuming we know the fundamentals of the underlying companies (earnings, dividends, etc.), we can infer the exact prices of all shares in the market.

Importantly, the two dimensions of the market’s valuation are controlled by two distinct entities:

- The fund investors control the market’s absolute valuation through their net cash injections and withdrawals (see green and red arrows, respectively). They cannot control the market’s relative valuation because they cannot trade in individual shares.

- The active funds control the market’s relative valuation through their buying and selling of individual shares. They cannot control the market’s absolute valuation because they are not allowed to try to increase or decrease their long-term allocations to equities.

The passive funds control nothing, because they have no freedom in any aspect of their market behaviors. They must deploy 100% of any funds they receive into equities, and they must buy and sell shares so as to establish positions that are in exact relative proportion to the supply outstanding.

Absolute Valuation: Driven by Net Cash Inflows and Outflows from Investors

Suppose that an investor sends new cash into a fund–either the passive fund or one of the 999 active funds–and that everything else in the system remains unchanged. The receiving fund will have an allocation target that it will have to follow. It will therefore have to use the cash to buy shares. But the receiving fund cannot buy shares unless some other fund sells shares. That other fund–the selling fund–will also have an allocation target that it will have to follow. It will therefore have to use the cash from the sale to buy shares from yet another fund, which will have to use the cash from the sale to buy shares from yet another fund, which will have to use the cash from the sale to buy shares from yet another fund, and so on. Instead of sitting quietly in the hands of the fund that it was injected into, the cash will get tossed around from fund to fund across the market like a hot potato.

How long will the tossing around of the hot potato (cash) last? At a minimum, it will last until prices rise by an amount sufficient to lift the aggregate equity capitalization of the market to a level that allows all funds to be at their target equity allocations amid the higher absolute amount of cash in the system. Only then will an equilibrium be possible.

To illustrate, suppose that each fund in the system is required to target an allocation of 95% equity, and 5% cash. Consistent with that allocation, suppose that there is $95MM of aggregate market equity in the system, and $5MM of aggregate cash. (95MM/$100MM = 95% equity, and $5MM/$100MM = 5% cash, so there’s a sufficient supply of each asset for every fund to satisfy its allocation mandate.) Suppose that investors then inject $5MM of new cash into the system, raising the total amount of cash to $10MM. That injection will throw the funds’ allocations out of balance. As a group, they will find themselves under-invested in equity relative to their targets, and will therefore have to buy shares. They will have to persist in that effort until prices rise by an amount sufficient to increase the system’s aggregate equity market capitalization to $190MM, which is the only number that will allow every fund to have a 95% allocation to equity amid the higher amount of cash ($10MM) in the system. ($190MM/$200MM = 95% equity, and $10MM/$200MM = 5% cash, leaving a sufficient supply of each asset for every fund to satisfy its allocation mandate.)

When cash is removed from the system, the same process takes place in reverse–prices get pulled down by the selling until the aggregate equity market capitalization falls to a level that allows the funds to be at their allocation targets amid the lower absolute amount of cash in the system.

Now, the process by which investor flows drive valuations in our hypothetical market is subject to the same natural feedbacks seen in any real market. As prices go up, the market’s valuation and implied future return becomes less attractive, therefore fewer investors send cash in, more investors take cash out, and prices see downward pressure:

Prices Up –> Demand Down –> Prices Down (Negative Feedback)

Conversely, as prices go down, the market’s valuation and implied future return becomes more attractive, therefore more investors send cash in, fewer investors take cash out, and prices see upward pressure:

Prices Down –> Demand Up –> Prices Up (Negative Feedback)

As in any real market, there are situations in which this natural negative feedback can give way to a different kind of positive feedback, where rising prices reflexively lead to greater optimism and confidence, fueling increased buying, decreased selling, and therefore further price increases:

Prices Up –> Demand Up –> Prices Up (More) (Positive Feedback)

…and, conversely, where falling prices reflexively lead to greater pessimism and fear, fueling decreased buying, increased selling, and therefore further price declines:

Prices Down –> Demand Down –> Prices Down (More) (Positive Feedback)

I highlight the details here simply to point out that the feedback processes governing prices in our hypothetical market are no different from the feedback processes that govern prices in real markets. The only difference is in the artificial “fund” structure that we’ve imposed, a structure that helps us separate out and explore the different components of price formation.

Relative Valuation: Driven by Active Fund Preferences

Active funds are the only entities in the system that have the ability to express preference or aversion for individual shares at specific prices. They are therefore the only entities in the system with direct control over the valuation of individual shares relative to each other.

If an active fund skillfully arbitrages the prices of individual shares–buying those that are priced to offer high future returns and selling those that are priced to offer low future returns–it will earn a clear micro-level benefit for itself: an excess return over the market. But will its successful arbitrage produce any macro-level benefits for the larger economy?

To answer the question, imagine a society where coins are the primary form of money, and where people generally hold coins in their pockets. Suppose further that in this society, there are a select group of careless people who fail to buy new pants on a recurring basis, and who therefore end up with holes in their pockets. As these people walk around the society, they unknowingly drop coins on the floor, leaving coins laying around for other passers-by to pick up and profit from. A savvy individual recognizes the profit opportunity asssociated with the “mistakes” these coin-droppers are making, and develops a way to skillfully “arbitrage” them. Specifically, he builds a super-whamodyne metal detector, which he uses to go on sophisticated coin hunts throughout the society. With this super-whamodyne metal detector, he is able to pick up falling and hidden coins much faster than anyone else, and therefore generates an outsized profit for himself.

Clearly, his coin-hunting activities will generate a micro-level benefit for him. But, aside from possible street cleanliness (fewer coins laying around?), are there any compelling macro-level benefits that will be generated for the overall society? No. Any “profit” that he earns in finding a given coin will be the mirror image of the loss incurred by whoever dropped it, or whoever failed to pick it up in front of him. His effort will benefit him, but the benefit will always occur alongside corresponding losses or missed gains for others. The system as a whole will see no net gain. From a macro-level perspective, the resources expended in the effort to build the super-whamodyne metal detector, and lug it all around the society in search of treasure, will have been completely wasted.

We can think of market arbitrage in the same way. Some market participants make mistakes. Other market participants expend vast resources trying to arbitrage those mistakes, with an emphasis on getting their first, in order to capture the profit. No value is generated in the process; rather, value is simply transferred from the mistake-makers to the arbitrageurs, just as it was transferred from the coin-droppers to the coin-hunter. From a macro-level perspective, the resources expended in the effort end up being wasted.

Now, to be fair, this argument neglects the fact that prices in a market impact capital formation, which in turn impacts an economy’s resource allocation. When a money-losing, value-destroying business is given an undeservedly high price, it is able to raise capital more easily, and is therefore more able to direct additional economic resources into its money-losing, value-destroying operation, where the resources are likely to be wasted. Conversely, when a profitable, value-generating business is given an undeservedly low price, it is less able to raise capital, and is therefore less able to direct economic resources into its profitable, value-generating operation, where they would otherwise have been put to beneficial economic use.

Personally, I tend to be skeptical of the alleged relationship between equity prices and capital formation. Corporations rarely fund their investment programs through equity issuance, and so there’s no reason for there to be any meaningful relationship. This is especially true for the mature companies that make up the majority of the equity market’s capitalization–companies that comprise the vast majority of the portfolio holdings on which active management fees get charged.

To illustrate the point with an example, suppose that the market were to irrationally double the price of Pepsi $PEP, and irrationally halve the price of Coke $KO. Would the change have any meaningful effect on the real economy? In a worst case scenario, maybe $PEP would divert excess income away from share buybacks towards dividends, or arbitrage its capital structure by selling equity to buy back debt. Maybe $KO would do the opposite–divert excess income from away dividends towards share buybacks, or arbitrage its capital structure by selling debt to buy back equity. Either way, who cares? What difference would it make to the real economy? For the shift to impact the real economy, it would have to be the case that money used for share repurchases and dividends and other types of financial engineering is deployed at the direct expense of money used for business investment, which evidence shows is not the case, at least not for large companies such as these. The companies make the investments in their businesses that they need to make in order to compete and profitably serve their expected future demand opportunities. Whatever funds are left over, they return to their shareholders, or devote to financial arbitrage.

Many investors believe that the current equity market is excessively expensive, having been inflated to an extreme valuation by the Federal Reserve’s easy monetary policy. Let’s assume that the most vocal of these investors are right, and that stocks in the market are at least twice as expensive as they should be. The Fed, then, has doubled the market’s valuation–or alternatively, has halved the equity funding costs of corporations. Ask yourself: is this alleged “distortion” leading to excessive corporate investment? No, not at all. If the current economy were experiencing excessive corporate investment, then we would be experiencing an inflationary economic boom right now. But we’re experiencing nothing of the sort–if anything, we’re experiencing the opposite, a period of slumpy moderation, despite being more than 7 years into an expansion. That’s because, contrary to the Fed’s better intentions, the transmission mechanism from share prices to real investment is weak.

Absolute and Relative Valuation: Samuelson’s Dictum

The price dynamics seen in our hypothetical market are obviously different from the price dynamics seen in real markets. In real markets, individual investors are allowed to invest directly in individual shares, which allows them to directly influence relative valuations inside the equity space. Similarly, in real markets, many of the active funds that invest in equities–for example, hedge funds–are able to significantly vary their net exposures to equities as an asset class. This ability allows them to directly influence the equity market’s absolute valuation.

With that said, there’s probably some truth to the model’s implication. Individual investors (as well as the first-level custodians that manage their money, e.g., RIAs) probably exert greater control over the market’s absolute valuation. That’s because they directly control flows into and out of investment vehicles that have no choice but to be fully invested in equities–e.g., active and passive equity mutual funds and ETFs. Conversely, they probably exert less control over the relative valuation of shares inside the equity market, because they’re less likely to be the ones directly speculating inside that space, opting to rely on the available investment vehicles instead.

In contrast, the professional managers that operate downstream of individual investor flows, and that manage the various investment vehicles that provide those investors with equity exposure, probably exert less control over the market’s absolute valuation. That’s because when flows come into or go out of their vehicles, they have to buy and sell, which means they have to put the associated buying and selling pressures somewhere into the market. They cannot opt to “hold” the pressure as a buffer–they have to pass it on. Conversely, they probably exert greater control over the relative valuation of shares inside the market, given that source investors often step aside and leave the task of making relative trades in the market to them, based on their expertise.

This fact may be the reason for Samuelson’s famous observation that markets are more efficient at the micro-level than at the macro-level. If micro-level decisions–e.g., decisions about which specific companies in the equity market to own–are more likely to be made by professionals that possess experience and skill in security selection, then we should expect markets to be more efficient at the micro-level. Conversely, if macro-level decisions–e.g., decisions about what basic asset classes to invest in, whether to be invested in anything at all, i.e., whether to just hold cash, and how much cash to hold–are more likely to be made at the source level, by the unsophisticated individuals that allocate their wealth to various parts of the system, individuals that are in no way inclined to optimize the timing of the flows they introduce, then we should expect markets to be less efficient at the macro-level.

We should note, of course, that the concept of efficiency is far more difficult to make sense of at the macro-level, where the different assets–cash, fixed income, and equities–are orthogonal to each other, i.e., of a totally different kind. The advantages and disadvantages associated with holding them cannot be easily expressed in each other’s terms.

To illustrate, a share of Google $GOOG and a share of Amazon $AMZN are the same general kind of asset–an equity security, an intrinsically-illiquid stream of potential future dividends paid out of future free cash flows. Because they are the same general kind of asset, it is easier to express the value of one in terms of the value of the other. If, at every point into the future, a $GOOG share will generate double the free cash flow of the $AMZN share, then it has double the value, and should be double the price; similarly, if it will generate half the free cash flow, then it obviously has half the value, and should be half the price.

A share of Google $GOOG and a dollar bill, in contrast, are not the same kind of asset–one is an equity security, an intrinsically-illiquid stream of future monetary payments, the other is fully-liquid present money, in hand right now for you to use in whatever way you please. Because they are not the same kind of asset, there is no easy way to put the two asset types together onto the same plane, no necessary, non-arbitrary ratio that one can cite to express the value that one posseses in terms of the other–e.g., 710 dollars for every $GOOG share. But that is precisely what it means to “value” them.

The Active Management Fee: Can it Be Earned?

Now, let’s be fair. In working to establish “correct prices”, active funds in a secondary market do provide macro-level benefits for the economy. It’s just that the benefits are small, frequently exaggerated in their actual economic impacts. As compensation for the work they perform in those efforts, the funds charge a fee–in our hypothetical example, the fee was 1% of assets. To earn that 1% fee, the funds need to outperform the market by 1% before fees. As a group, is it possible for them to do that?

The temptation is to say no, it is not possible. The passive fund is holding the market portfolio. Since the passive fund plus the collection of active funds equals the overall market, it follows that the active funds, collectively, are also holding the market portfolio. Given that the two segments of the market–passive and active–are holding the same portfolios, it’s logically impossible for one segment to outperform the other. In previous pieces, we called this observation, attributable to William Sharpe, “The Law of Conservation of Alpha.” Aggregate alpha in a market must always sum to zero.

The Law of Conservation of Alpha seems to leave us no choice but to conclude that the active funds in our hypothetical system will simply underperform the passive fund by the amount of their fees–in the current case, 1%–and that the underperformance will continue forever and ever, never being made up for. But if that’s the case, then why would any rational investor choose to invest in active funds?

Imagine that there are two asset classes, A and B, and that you have the option of investing in one or the other. Suppose that you know, with absolute certainty, that asset class B is going to underperform asset class A by 1%. Knowing that fact, why would you choose to invest in asset class B over asset class A? Why would you choose to invest in the asset class with the lower expected return?

It makes sense for investors to accept lower returns in exchange for lower amounts of risk. But, in this case, the group of active funds are not offering lower risk in comparison with the passive fund. They are offering the exact same risk, because they are holding the exact same portfolio. In fact, there’s a relevant sense in which the active funds, considered individually, are offering additional risk in comparison with the passive fund–specifically, the additional risk of underperforming or outperforming the benchmark. To be fair, that risk may not be a clear net negative in the same way that volatility is a net negative, but it certainly isn’t a net positive, and therefore it makes no sense for investors to throw away 1% in annual return, every year, year after year, in exchange for the highly dubious “privilege” of taking it on.

What we have in our hypothetical market is an obvious arbitrage–go with the passive fund, and earn an extra 1% per year in expected return, with no strings attached. As investors become increasingly aware of that arbitrage, we should expect them to shift their investments out of the active funds and into the passive fund, a transition that is taking place in real markets as we speak. Our intuitions tell us that there should be adverse consequences associated with the transition. As more and more investors opt to free-ride on a passive approach, pocketing the 1% instead of paying it, we should expect there to be negative impacts on the market’s functioning.

In a previous piece, I argued that there were impacts on the market’s functioning–but that, surprisingly, they were positive impacts. Counter-intuitively, the transition out of active funds and into passive funds makes the market more efficient in its relative pricing of shares, because it preferentially removes lower-skilled players from the active segment of the market, leaving a higher average level of skill in the remaining pool of market participants to set prices. I extended the argument to include the impact on retail investors, who, in being persuaded to take on equity market exposures through passive vehicles, rather than by picking individual stocks or active fund managers themselves, were rendered less likely to inject their own lack of skill into the market’s relative pricing mechanism. Granted, they will be just as likely to distort the market’s absolute valuation through their knee-jerk inflows and outflows into the market as a whole, but at least they will not be exerting additional influences on the market’s relative valuation, where their lack of skill would end up producing additional distortions.

Now, if market participants were to shift to a passive approach in the practice of asset allocation more broadly–that is, if they were to resolve to hold cash, fixed income, and equity from around the globe in relative proportion to the total supplies outstanding–then we would expect to see a similarly positive impact on the market’s absolute pricing mechanism, particularly as unskilled participants choose to take passive approaches with respect to those asset classes in lieu of attempts to “time” them. But, to be clear, a broader shift to that broader kind of passivity is not currently ongoing. The only areas where “passive” approaches are increasing in popularity are areas inside specific asset classes–specifically, inside the equity and fixed income markets of the developed world.

Active to Passive: The Emergence of Distortion

Passive investing may improve the market’s efficiency at various incremental phases of the transition, but there are limits to the improvement. To appreciate those limits, let’s assume that the migration from active to passive in our hypothetical market continues over the long-term, and that the number of active funds in the system ends up shrinking down to a tiny fraction of its initial size. Whereas the active segment of the market initially consisted of 999 active funds collectively controlling roughly 50% of equity assets, let’s assume that the active segment shrinks down to only 10 funds collectively controlling 0.5% of equity assets. The other 99.5% of the market migrates into the passive fund.

In evaluating the impact of this shift, it’s important to remember that active investors are the entities that set prices in a market. Passive investors cannot set prices, first because they do not have any fundamental notion of the correct prices to set, and second because their transactions are forced to occur immediately in order to preserve the passivity of their allocations–they cannot simply lay out desired bids and asks and wait indefinitely for the right prices to come, because the right prices may never come. To lay out a desired bid and ask, and then wait, is to speculate on the future price, and passive funds don’t do that. They take whatever price is there.

In the above configuration, then, the tiny segment of the market that remains active–which holds roughly 0.5% of the total equity supply–will have to set prices for all 5,000 securities in the market. It follows that a much smaller pool of resources will be devoted to doing the “work”–i.e., the fundamental research, the due-diligence, etc.–necessary to set prices correctly. For that reason, we should expect the configuration to substantially reduce the market’s efficiency, contrary to what I asserted earlier.

In our hypothetical market, a 1% active management fee was initially being levied on 50% of the market’s capitalization, with the proceeds used to fund the cost of due-diligence. After the migration, that 1% fee will be levied on only 0.5% of the market’s capitalization, yielding roughly 1/100 of the proceeds. The shrunken proceeds will have to pay for the cost of due-diligence on a security universe that hasn’t shrunken at all. Because the active segment will have a much smaller amount of money to spend on the due-diligence process, a new investor that enters and spends a given amount of money on it in competition with the active segment will be more likely to gain an edge over it. At the margin, active investors that enter at the margin will be more capable of beating the market, which is precisely what it means for the market to be less efficient.

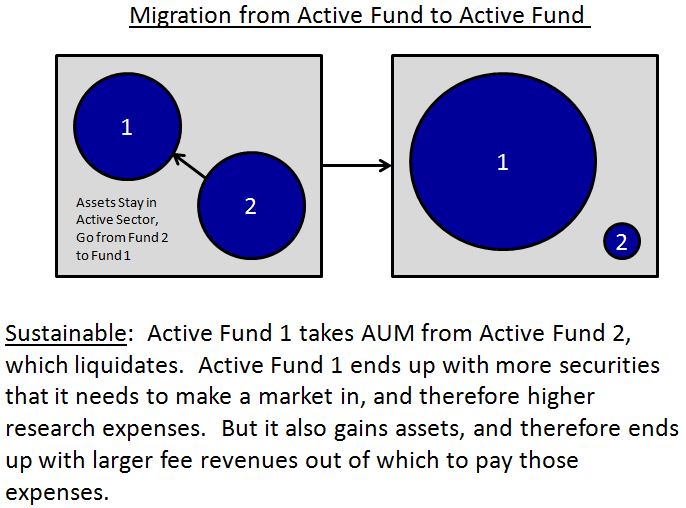

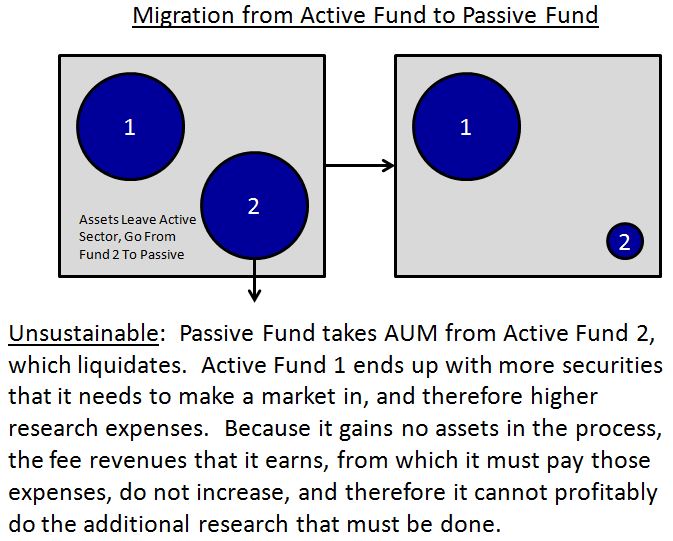

This thinking is headed in the right direction, but there’s a subtle problem with it. The best way to see that problem is to trace out the literal process by which the active segment will end up shrinking. Suppose we return to where we initially started, with 999 active funds and 1 passive funds. In their efforts to arbitrage the 1% differential in expected returns, investors transfer large sums of money out of the 100 active funds with the worst performance track records, and into the market-performing passive fund, forcing the 100 active funds to shut down.

The 100 active funds that end up shutting down will have to sell their shares to raise cash to redeem their investors. But who will they sell their shares to? They might be able to sell some of their shares to the passive fund, because it will be receiving cash inflows, and will need to buy shares. But they won’t be able to sell all of their shares to the passive fund, because the passive fund will have to buy shares of every company in the market–all 5,000, in proportion to the supply oustanding–many of which the active funds won’t be holding. The passive funds will therefore have no choice but to buy at least some of their shares from the other 899 active funds that remain.

Working out the implications of the flows, then, the 100 underperforming active funds, in liquidating themselves, will have to sell at least some of their shares to the 899 remaining active funds. Those remaining active funds will be in a position to buy the shares, because they will have received cash from selling some of their own shares to the passive fund when it went in to buy. But before the remaining active funds can buy the new shares, they will have to conduct research–due-diligence–to determine the appropriate prices. That due-diligence will cost money. Where will the money come from?

Unfortunately, there is nowhere for it to come from, because the assets that the remaining active funds will have under management, and therefore the fee revenues that they will be able to earn, will not have increased. Crucially, in the migration, assets will not be moving from the 100 underperforming active funds to the remaining active funds who will perform the needed fundamental research on the shares being sold–rather, assets will be moving from the 100 underperforming funds to the cheapskate passive fund, which doesn’t spend any money at all on the research process, opting to simply give the money back to its investors instead. Consequently, the money needed to fund the additional research will not be available. Unless the money is taken out of some other necessary research activity, or out of the active fund manager’s wages or profits, the research and due-diligence necessary to buy the shares will not get done.

The following two schematics distinguish two types of migrations: a sustainable migration from active fund to active fund, and an unsustainable migration from active fund to passive fund.

In our scenario, the remaining active funds will not have done the research necessary to buy the shares that the underperforming funds will need to sell, and will not get paid any additional money to do that research. Consequently, they aren’t going to be interested in buying the shares. But the 100 underperforming active funds have to sell the shares–they have to get cash to redeem their investors. So what will happen? The answer: the bid-ask spread will effectively widen. Prices will be found at which the remaining active funds will be willing to transact–those prices will simply be much lower, to ensure adequate protection for the funds, given that they haven’t done the work necessary to be comfortable with the purchases, or alternatively, given that they need to pay for that work, and that the money has to come from somewhere.

The point articulated here is admittedly cumbersome, and it might seem out of place to think about the process in terms of the need to pay for “research.” But the point is entirely accurate. The best way to grasp it is to start from the endgame scenario that we posited, a scenario where active funds shrink down to some absurdly small size–say, 0.5% of the market, with the other 99.5% of the market invested passively. How do you get to a situation where a measly 0.5% of the market, a tiny group of managers that are only able to draw in a tiny revenue stream out of which to pay for fundamental research, is setting prices–placing bids and asks–on a massive equity universe consisting of 5,000 complicated securities? The only way you get there is by having bid-ask spreads completely blow out. If their counterparties are desperate, then yes, the tiny group of active funds will trade in securities that they aren’t familiar with or interested in, and that they haven’t done adequate due-diligence on. But they will only do so at prices that are sufficient to provide them with extreme margins of safety: ultra-low bids if they have to be the buyers, and ultra-high asks if they have to be the sellers.

In the previous piece on Indexville, we posed the question: what will happen if the active segment of the market becomes too small, or if it goes away completely? Most people think the answer is that the market will become “inefficient”, priced incorrectly relative to fundamentals, making it easier for new active investors to enter the fray and outperform. But we saw that that’s not exactly the right answer. The right answer is that the market will become illiquid. The bid-ask spread will blow out or disappear entirely, making it increasingly costly, or even impossible, for investors–whether passive or active–to transact in the ways that they want to.

The example above takes us to that same conclusion by a different path. If an active segment with a tiny asset base and tiny fee revenues is left to set prices on a large universe of complicated securities, the bid-ask spreads necessary to get that segment to transact will explode, particularly in those securities that it has not done sufficient research on and that it is not familiar with or comfortable transacting in–which will be most securities, given that a tiny segment of a large market cannot single-handedly do the work of studying and forming a sound fundamental opinion on everything inside it.

Liquidity Provision: A Way to Earn the Fees

We return to the question at the title of the previous section: Can the fees that active managers collectively charge be earned? The answer is yes. The fees can be earned out of revenues generated through the provision of liquidity–selling at the ask to those that need to buy, and buying at the bid from those that need to sell. The excess return over the market equals half the spread between the two, times the volume, divided by the capital employed. As the active segment of the market shrinks in size, that excess return will increase. At the same time, the fees extracted by the segment will decrease, bringing the segment closer to a condition in which its fees match its excess returns, which is what it means for the active segment to earn its fees.

The active segment of the market has two external counterparties that it can provide liquidity to: first, the passive segment, which experiences inflows and outflows that it must deploy and redeem, and second, the corporate sector, which sometimes needs to raise equity funding, and which, more frequently in the present era, wants to buy back its own shares. The total flows of those external counterparties–the total amount of buying and selling that they engage in–will determine the amount of excess return that the active segment can generate in providing liquidity to them, and therefore the maximum fees that it can collectively “earn.” Any fees that get extracted above that amount will be uncompensated for, taken from investors in exchange for nothing.

If the market were suffering from an inadequate amount of active management, the consequences would become evident in the performance of passive funds. Passive funds would begin to exhibit increased tracking errors relative to their benchmarks. Every time they received a cash inflow and attempted to buy shares, they would be forced to buy at the elevated ask prices set by the small number of active funds willing and able to transact with them, ask prices that they would push up through their attempted buying. Conversely, every time they received redemption requests and attempted to sell shares, they would be forced to sell at the depressed bid prices set by the small number of active funds willing to transact with them, bid prices that they would pull down through their attempted selling. On each round-trip, each buy followed by a sell, they would lodge a tracking loss relative to their indices, the mirror image of which would be the excess profit earned by the active segment in providing them with liquidity.

Now, you might think that liquidity in the market is already provided by specialized market-makers–e.g., computers trading on HFT algorithms–and that active, fundamentally-informed investors are not needed. But market-makers of that type only provide one small phase of the market’s liquidity–the phase that entails bridging together, over the very short-term, the temporarily divergent flows of participants that are seeking to hold shares for longer periods of time. Active investors, those that are willing to adjust their demand for shares based on fundamental value, are crucial to the rest of the process, because they are the only entities that are capable of buffering and balancing out longer-term flow imbalances that otherwise emerge in the market–situations, for example, where there is an excess of interested sellers, but no interested buyers, either present or en route, even after the ask price is substantially lowered. Without the participation of value-responsive active investors in those situations, market-makers would have no buyers to bridge the selling flows against, and would therefore have to widen their spreads, i.e., lower their bids–or even remove them from the market altogether.

Right now, the average tracking error in the average passive fund is imperceptible. This fact is proof that the current market, in its ongoing migration into passive funds, isn’t even close to suffering from an insufficiency of active management. With at most 40% of the equity market having gone passive, the point in the transition where tangible market illiquidity will ensue is still very far away.

That’s why, in the previous piece, I argued that the active segment of the market is not even close to being able to earn its fees in the aggregate. Active managers aren’t doing anything wrong per se, it’s just that the shrinkage they’ve suffered hasn’t yet been extreme enough to undermine the function they provide, or make the provision of that function profitable enough to reimburse the fees charged in providing it. Granted, they may be able to earn their fees by exploiting “dumb-money” categories that we haven’t modeled in our hypothetical market–e.g., retail investors that choose to conduct uninformed speculation in individual shares, and that leave coins on the floor for skilled managers to pick up behind them–but they aren’t even close to being able to collectively earn their fees via the liquidity they provide to the other segments of the market, which, evidently, are doing just fine.

The Actual Forces Sustaining Active Management

Active managers, in correctly setting prices in the market, provide a necessary benefit to the economy. In a mature, developed economy like ours, where the need for corporate investment is low, and where the corporate sector is able to finance that need out of its own internal cash flows, the benefit tends to be small. But it’s still a benefit, a contribution that a society should have to pay for.

Right now, the people that are paying for the benefit are the people that, for whatever reason, choose to invest in the active segment of the market, the segment that does the work necessary to set prices correctly, and that charges a fee for that work. But why do investors do that? Why do they invest in the active segment of the market, when they know that doing so will leave them with a lower return on average, in exchange for nothing?

The question would be more apt if active investors were investing in a fund that owned shares of all actively-managed funds–an aggregate fund-of-all-active-funds, if one can envision such a monstrosity. Investors in such a fund would be giving away the cost of fees in exchange for literally nothing—a return that would otherwise be absolutely identical to the passive alternative in every conceivable respect, except for the useless drag of the fees.

But that is not what people that invest in the active segment of the market are actually doing. Active management is not a group sport; the investors that invest in it are not investing in the “group.” Rather, they are investing in the individual active managers that they themselves have determined to be uniquely skilled. It’s true that they pay a fee to do that, but in exchange for that fee, they get the possibility of outperformance–a possibility that they evidently consider to be likely.

Every investor that rationally chooses to invest in the active segment of the market makes the choice on that basis–an expectation of outperformance driven by the apparent skill of the individual active manager that the investor has picked out. Whereas this choice can make sense in individual cases, it cannot make sense in the average case, because the average of the group will always be just that–average in performance, i.e., not worth extra fees. In choosing to invest in the active segment, then, active investors are choosing, as a group, to be the gracious individuals that pay for the cost of having “correct market prices”, in exchange for nothing. Passive investors are then able to free-ride on that gracious gift.

How, then, is the active segment of the market able to remain so large, particularly in an environment where the fees charged are so high, so much more than the actual cost of doing the fundamental research necessary to have a well-functioning market? Why don’t more active investors instead choose the passive option, which would allow them to avoid paying the costs of having a well-functioning market, and which would net them a higher average return in the final analysis?

The answer, in my view, is two-fold:

(1) The Powers of Persuasion and Inertia: For every active manager, there will always be some group of investors somewhere that will be persuaded by her argument that she has skill, and that will be eager to invest with her on the promise of a higher return, even though it is strictly impossible for the aggregate group of managers engaged in that persuasive effort to actually fulfill the promise. Moreover, absent a strong impetus, many investors will tend to stay where they are, invested in whatever they’ve been invested in–including in active funds that have failed to deliver on that promise.

(Side note: Did you notice how powerful that shift from the use of “he” to the use of “she” was in the first sentence of the paragraph above? The idea that the manager that we are talking about here is a female feels “off.” Moreover, the connotation of deceipt and trickery associated with what the active manager is doing in attempting to convince clients that he has special financial talents and that his fund is going to reliably outperform is significantly reduced by imagining the manager as a female. That’s evidence of ingrained sexual bias, in both directions).

(2) The Framing Power of Fee Extraction: Fees in the industry get neglected because they are extracted in a psychologically gentle way. Rather than being charged as a raw monetary amount, they are charged as a percentage of the amount invested. Additionally, rather than being charged abruptly, in a shocking one-time individual payment, they are taken out gradually, when no one is looking, in teensy-weensy daily increments. As a result, an investor will end up framing the $10,000 fee she might pay on her $1,000,000 investment not as a literal payment of $10,000 that comes directly out of her own pocket, but rather as a negligible skim-off-the-top of a much larger sum of money, taken out when no one is looking, in miniscule incremental shavings that only accumulate to 1% over the course of a full year.

To illustrate the power that this shift in framing has, imagine what would happen if the DOL, in a follow-up to its recent fiduciary interventions, were to require all annual fees to be paid at the end of each year, by a separate check, paid out of a separate account. Then, instead of having the 1% fee on your $1,000,000 mutual fund investment quietly extracted in imperceptible increments each day, you would have to cut a $10,000 check at the end of each year–go through the process of writing it out, and handing it over to the manager, in exchange for whatever service he provided. $10,000 is a lot of money to pay to someone that fails to deliver–even for you, a millionaire!

If the way fees are framed were forcibly modified in this way, investors would become extremely averse to paying them. The ongoing shrinkage of the market’s active segment–in both its size and its fees–would accelerate dramatically. The effects of the policy might even be so powerful as to push the market into a state in which an acute scarcity of active management ensues–a situation in which everyone attempts to free-ride on the index, and no one steps up to pay the expenses associated with having a well-functioning market. If that were to happen, active funds would find themselves capable of generating excess returns from the provision of liquidity that substantially exceed the fees they charge. Investors in active funds, who are the only ones actually paying the cost of that service, would begin to receive a benefit for having paid it, a benefit that would be well-deserved.