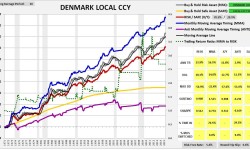

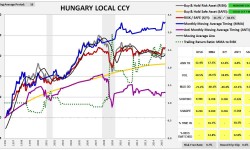

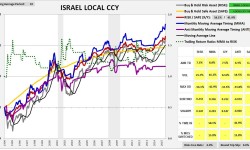

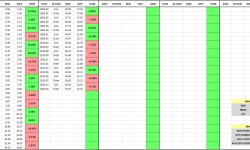

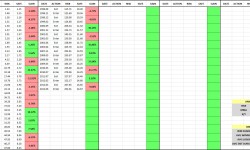

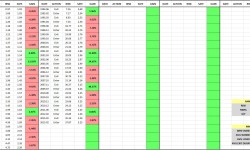

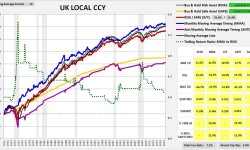

The following table shows the historical win percentage and average excess performance of the MMA timing strategy versus the X/Y portfolio and the RISK portfolio for foreign equities where prices and returns are denominated in local currency terms:

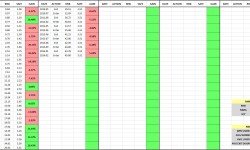

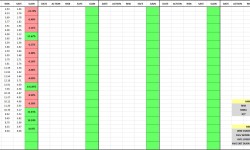

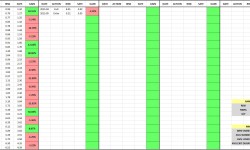

The following tables show the performance numbers of the different strategies in each foreign market:

Note that these returns are nominal returns. The strong nominal performances of certain emerging market countries in the table–e.g., Turkey–are not reflections of underlying corporate strength, but rather consequences of persistently high inflation. Equities are claims on the output of real capital, and therefore exhibit nominal fundamentals that shift commensurately with the price index over time.

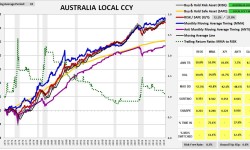

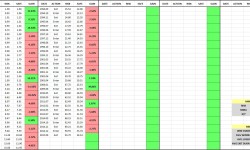

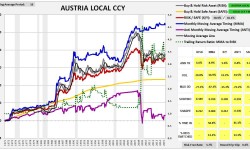

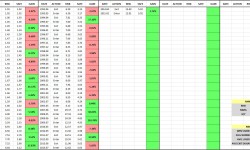

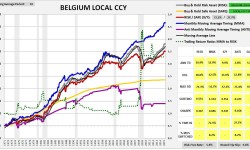

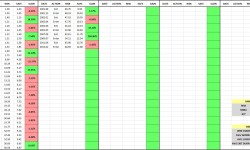

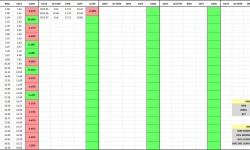

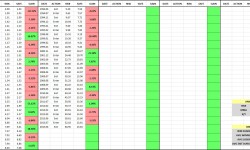

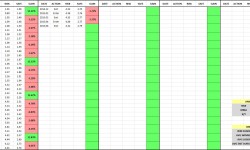

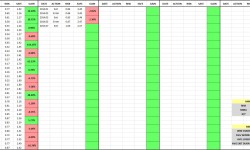

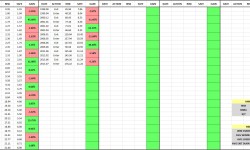

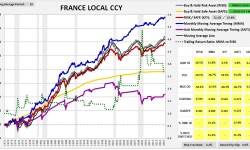

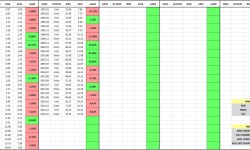

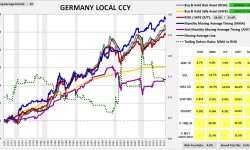

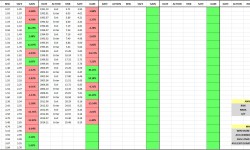

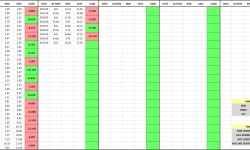

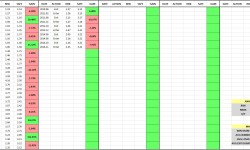

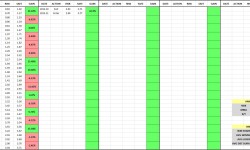

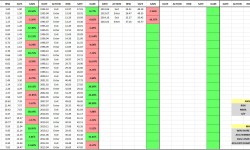

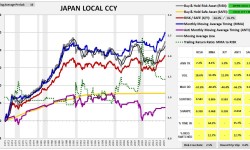

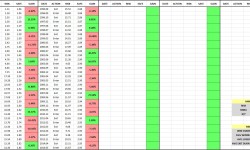

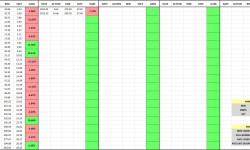

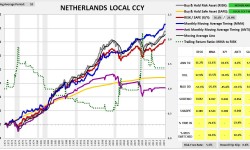

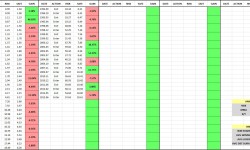

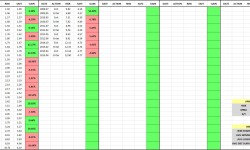

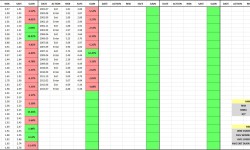

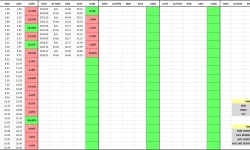

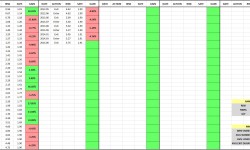

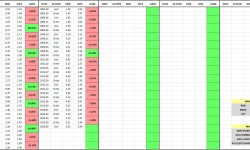

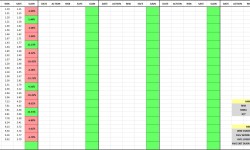

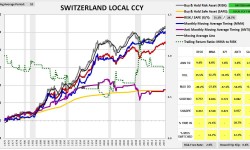

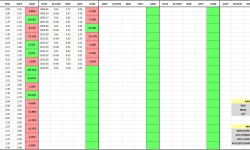

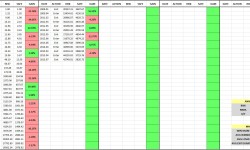

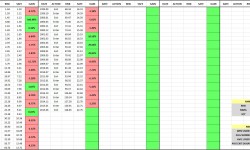

The following charts provide visual illustrations of the individual performances. The tables to the right of the charts show the MMA strategy’s entry/exit dates and registered gains/losses (relative to buy and hold). The charts and tables form a slideshow that begins when any image is clicked:

Source: MSCI, FRED, Goyal, Statistical Archives of the Riksbank, and Other National Central Bank Websites (for local currency short-rates).