Is the U.S. stock market expensive? To answer the question, we need to get precise about what we mean by “expensive.” Expensive relative to what? When valuation bears say that the stock market is expensive, they usually mean “expensive relative to the past.” They take charts of normalized valuation metrics–Shiller CAPE, Price to Sales, Price to Book, Market Cap to GDP, Q-Ratio, and so on–and point out that the current value is higher than the average value.

OK, but so what? Most of us already agree that the stock market is expensive–again, relative to the past. If the choice were between investing in the 2014 market, and investing in the “average” market of the pre-1995 period, I doubt that very many informed investors would choose 2014. The typical market before the tech-bubble was priced to offer very attractive returns, with a median P/E of around 13 times trailing earnings. The current market, at around 17 times trailing earnings, is priced much more richly. But this doesn’t mean that the current market is priced incorrectly. It doesn’t mean that a mistake is being made, and that you should therefore hunker down in cash and wait for the situation to get “corrected.” There’s an excellent chance that nothing is going to get corrected, that you’re going to wait in vain forever, because nothing is wrong.

Yes, the market is expensive relative to the past, but why shouldn’t it be? If markets are efficient, then equities cannot remain priced for historically attractive returns while all other asset classes are priced for historically unattractive returns. In such a scenario, every rational investor will choose to hold equities. But, as a rule, someone must always be found to hold the other stuff–including the cash. Equity prices will therefore get pushed up and implied returns pulled down. The market will seek out a new equilibrium in which relative valuations are more congruent with each other, and where it is easier to find a willing holder of every asset.

Right now, cash and bonds are offering historically unattractive returns. That condition is unlikely to change any time soon. Granted, as the economy picks up steam over the next few years, the Fed will tighten. But it’s unlikely that the Fed will tighten by very much. Maybe by a couple hundred basis points, but nothing that would provide an independently attractive return to savers.

The U.S. economy is a mature, aging economy with very little population growth. Relative to the past, it has a much smaller “future” to build for, and much less in the way of new, genuinely innovative things that it can build. For this reason, the U.S. household and corporate sectors have little reason to invest and expand credit at the paces that characterized prior historical eras.

Over the next several years and decades, the Fed will likely find it difficult to ensure that adequate levels of investment and credit creation take place to match the desired level of savings in the economy. The only variable that it can adjust to achieve the required balance is the interest rate, and therefore the interest rate is almost certainly going to remain low relative to history. If you disagree, just look at what the market is saying: the 10 year treasury is at 2.65% for a reason.

The Last 20 Years

Stocks have been expensive relative to the past for pretty much the entirety of the last 20 years. The expensiveness coincides very neatly with the time when the low interest rate regime initially began. The biggest mistake that valuation bears have made is to interpret this expensiveness in moralistic terms, as some kind of “scandal.” It’s not a scandal. It’s the expected outcome of a properly functioning market.

Some have suggested that the Federal Reserve is unfairly “punishing” savers by setting interest rates at a low level. But this is empty rhetoric. Savers do not have a right to get paid to sit on risk-free bank deposits. When the economy is overheating, the Fed may choose to create an interest rate environment that rewards them for sitting on bank deposits rather than spending and investing and making the overheat worse. But this reward is not a right, just like the reward of a low borrowing cost that the Fed sometimes affords to those that do choose to spend and invest, when economic conditions call for it, is not a right.

From 2003 to 2008, valuation bears typically focused on two themes: the first was the rising level of instability in the U.S. economy, expressed most vividly in the housing bubble, the second was the market’s elevated valuation. They got the first theme right, but the second theme wrong. Unfortunately, they interpreted the 2008 plunge as confirmation that they were right on both themes. The experience has given them the misplaced confidence to stubbornly fight the tape, to continually bet on a repeat of 2008, even when there’s been little reason to expect one.

Let’s be honest. To the extent that you, the reader, are a valuation bear, you probably got the cyclical economic call right, and you deserve credit for it. But you got the valuation call wrong. That’s why you avoided the crash, but were then unable to participate in much of the bull market that has subsequently ensued. If you had focused simply on the cycle itself, and ignored the “overvaluation” bit, you would have been much better off. Not just from 2009 to now, but from 1995 to now.

Anchoring and the Sunk Cost Fallacy

To return to the issue of interest rates, we can find periods in history–say, the 1910s or the 1940s–where cash and bonds yielded very little while stocks were cheap, priced for very high returns. But we’re not living in the 1910s or the 1940s. There’s no reason to use the cautiousness and irrationality that investors exhibited in those periods as a guide for what’s likely to happen now, in the year 2014. We need to give markets some credit–they are capable of evolving, progressing, becoming more efficient over time. Over the last 100 years, they’ve evolved immensely. Easy arbitrage opportunities, whether across asset classes, or inside them, have become much fewer and farther between.

Over the last 10 years, cash has returned roughly 1.5% annually. Over the next 10 years, those on the sidelines will be lucky to see cash match that average return. Who is the person that is going to opt to hold cash at a long-term return of 1.5% if stocks are priced to return their historical average of 10%? Certainly not me. Certainly not you. Not even the valuation bears. But then who? In the year 2014, is there anyone historically misguided enough to think that hunkering down in cash in such an environment is the right answer? In 1917, or 1942, a sufficient number of those people may have existed, enough to create an arbitrage opportunity for the rest of the market. But very few exist now. And therefore investors should not expect, as a matter of course, to be offered the historical average, 10%, in exchange for taking equity risk. It’s not a realistic expectation.

To use the market’s valuation relative to the past as a criterion for investing is to fall prey to the behavioral bias of anchoring and the fallacy of sunk cost. Who cares if stocks offered a better return in the past than they currently offer? All that matters is what they are offering now, and what they are likely to offer in the future. We select from the options that are there, not from the options that used to be there, and especially not from the options that we think “should be” there in a moral sense.

I’m all for the idea of going into Europe, or Japan, or even cautiously into the mess of the Emerging Markets, to try to find better equity bargains than currently exist in the U.S. Likewise, I fully support efforts to try to identify and exploit the hidden forces that might eventually cause U.S. stocks to fall appreciably, so that they offer more attractive returns. But “valuation relative to the past” is not one of those forces.

Asset Supply: The Expensiveness is Not Only a Function of Implied Returns

An issue that often gets neglected, but that is crucial here, is the issue of asset supply. What is the total supply of cash in the market? What is the total supply of credit? What is the total supply of equity? The prices required to attract the needed holders of each asset class, and thereby move the market towards equilibrium, depend not only on the relative implied returns, but also on the relative amount of each asset class in existence–how much there is that needs to be held in investor portfolios.

To briefly review, the “supply” of equity is the total dollar “amount” of it in existence–the total shares outstanding times the market price. The relative supply of equity is the total dollar amount of it in existence relative to the total amount of cash and credit in existence. That relative amount matters because the three asset classes take up space in investor portfolios, and investors have preferences for how much space each should take up–what “percentage” of their overall portfolios each should represent. They seek out certain exposures. How much exposure they seek out is a function of all of the familiar variables that drive market outcomes: sentiment, confidence, mood, valuation, culture, demographics, past experience, reinforcement, social, environmental, and market feedback, and so on. If you flood the market with new cash and credit, and nothing else changes, equity prices will experience upward pressure, unrelated to any of these variables, because investors will attempt to allocate the new “wealth” in accordance with their allocation preferences. The amount of equity exposure they want isn’t going to fall just because new cash and credit have been shoved into their portfolios for them to hold. Therefore, equity prices will get pushed up.

Right now, there’s a very large amount of cash and credit in existence. It’s been building up in the system for over 30 years. At currently high market prices, the relative supply of equity, and therefore the aggregate portfolio exposure to it, is roughly in line with normal levels, despite the large amount of cash and credit in existence. However, if you were to pull the market down substantially, so as to bring the implied return back to its historical average–say, 10%–the relative supply of equity would fall well below normal levels. But at an implied 10% return, the portfolio demand for equity exposure would be much higher than it is now–despite the much lower relative supply. The result would be a supply shortage that pushes equity prices right back up. For a related discussion of some of the allocative forces underneath the market’s seemingly relentless upward pressure, I highly recommend Josh Brown’s recent viral hit, The Relentless Bid, Explained.

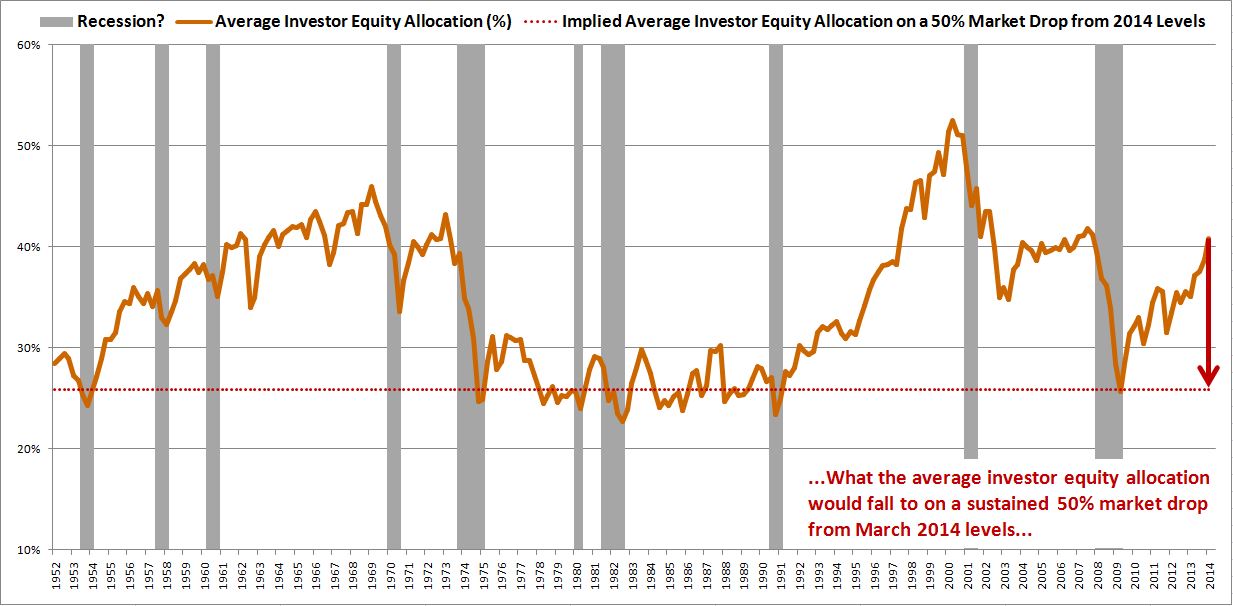

Citing a number of different normalized valuation measures, John Hussman recently estimated that that the U.S. equity market is more than 100% overvalued, that it needs to fall by more than 50% just to offer normal historical returns. But even if John is right in this conclusion, it doesn’t matter–the market isn’t capable of sustaining a 50% fall in the current environment.

Sure, the market could fall by 50% in a temporary panic, unrelated to valuation, as it did in late 2008 and early 2009. But for it to drop by 50% in a long-term valuation re-rating, a move that actually sticks, investors would need to undergo a sea change in portfolio allocation preference. They would need to want their equity exposures reduced to the record lows of the early 1980s, a period when the competition–cash and bonds–was yielding double digits. Right now, the competition is yielding virtually nothing.

A scenario where stocks offer normal historical returns, where cash and bonds offer nothing and a few hundred basis points respectively, and where investors choose to keep their stock exposures at generational lows, not for a couple of quarters as they work through a panic, but for the long haul–for years, decades–is too unrealistic to even be worth discussing. Definitely not a scenario that anyone should be betting on.

Once we agree that the stock market is expensive, and that it should be expensive, the next step is to consider whether it’s as expensive as these “normalized” valuation measures suggest it to be–whether it’s at a clear extreme that cannot be justified by reference to the secular drop in interest rates and the favorable supply dynamics. I say that it is not–at least not yet. In the coming weeks, I intend to write more on some of the reasons why.