The following chart shows the aggregate net profit margin of the S&P 500 using earnings data updated through the 1st quarter of 2015 (75% complete):

With yet another quarter now on the books in which profit margins have remained steady at record highs, it’s becoming increasingly difficult for open-minded investors to reject the possibility that “this time is different”–i.e., the possibility that the observed profit margin increase relative to past averages is secular in nature, and that the mean reversion that many have been expecting simply isn’t going to happen.

If the profit margin increase is secular, what is driving it? Analysts who write on the topic tend to cite two factors associated with the cost structure of the corporate sector: (1) weak labor bargaining power leading to reduced labor costs, and (2) low interest rates leading to reduced interest expense. Because these factors are likely to remain in place going forward, analysts have argued that profit margins will remain elevated.

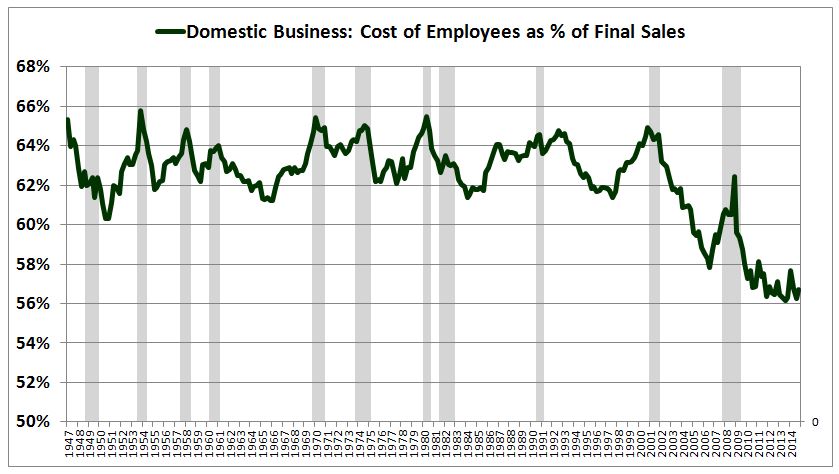

On the labor front, labor bargaining power has weakened substantially amid globalization, automation, and the demise of unions. As a percentage of final sales, labor costs–which consist primarily of wage and pension expenses–have fallen as a percentage of final sales from a previous long-term range of 62% to 64% to a new low of roughly 56%, which translates to a profit margin boost of roughly 7%. From BEA NIPA Table 1.14:

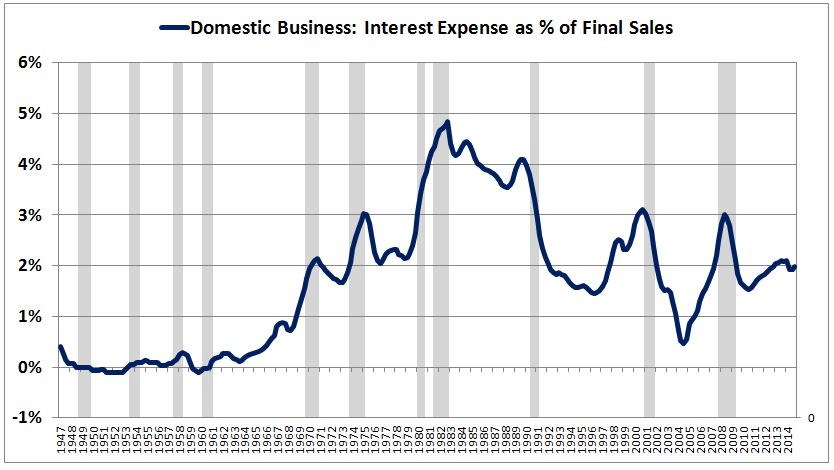

On the interest front, the picture is quite different. Interest rates have fallen by more than 10% over the last 30 years, but interest expense hasn’t shown a proportionate drop. As a percentage of final sales, the reduction in interest expense has amounted to a meager 2.5%. Interestingly, current corporate interest expense is almost twice as high as it was in the 1960s, despite the fact that long-term corporate bond yields are lower today than they were then. Again, from NIPA Table 1.14:

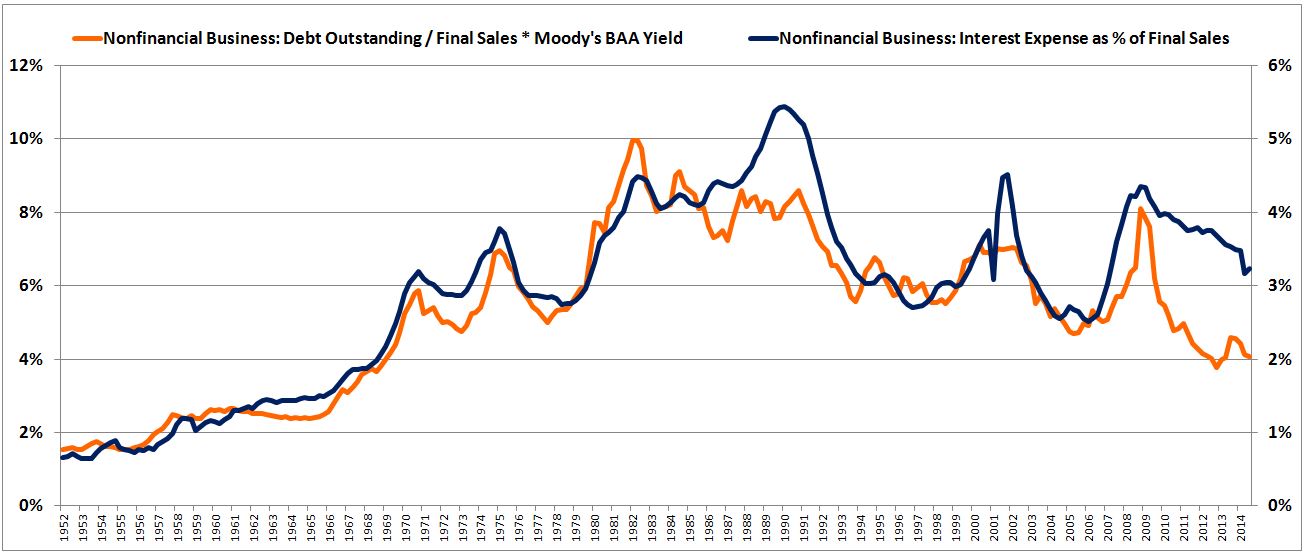

The reason that interest expense hasn’t fallen on par with the fall in interest rates is that corporate debt levels have grown substantially alongside the fall. Recall that total interest expense depends not only on the interest rate paid, but also on the quantity of debt that the interest must be paid on.

The following complicated chart demonstrates the point graphically. The blue line is the interest expense of nonfinancial corporations as a percentage of final sales. The orange line is an approximation of that expense using nonfinancial corporate debt outstanding and Moody’s BAA yield as functional inputs.

In terms of the explanations themselves, reductions in various components of the corporate cost structure may have helped to catalyze the profit margin increase, but they do not explain how corporations have been able to hold on to profit margins in the face of competition.

On classical capitalist economic theory, reductions in corporate costs should not lead to sustained increases in profit margins. The reason is simple. With all else equal, increased profit margins imply increased returns on (newly) invested capital (ROIC). Increased ROICs tend to provoke increased investment inflows into the sector or industry where the ROICs have increased. These inflows add capacity and therefore intensify competition. They also put upward pressure on corporate costs–wages and interest rates. The combined result is downward pressure on ROICs and therefore downward pressure on profit margins. To quote the inventor of capitalism himself:

“The increase of stock, which raises wages, tends to lower profit. When the stocks of many rich merchants are turned into the same trade, their mutual competition naturally tends to lower its profit; and when there is a like increase of stock in all the different trades carried on in the same society, the same competition must produce the same effect in them all.” — Adam Smith, The Wealth of Nations, 1776, I.IX.2

It’s clear, then, that explanations that point to lower labor costs and lower interest expense cannot be the whole story. They fail to explain how the mechanism of mean-reversion in profitability, a fundamental tenet of the way capitalist economies operate, could be circumvented for so long.

Ultimately, on classical economic theory, there are only two ways for profit margins to experience sustained increases over the long-term:

First, corporate agents can become more risk-averse. If they become more risk-averse, then higher ROICs will be necessary to entice them to invest–that is, the reward to investment will have to increase to get them to come off the sidelines and take risk. Investment is the basis for competition, and therefore if higher ROICs are necessary to entice corporate agents to invest, then higher ROICs will be necessary to entice them to compete with each other. The result will be higher ROICs at the eventual competitive equilibrium.

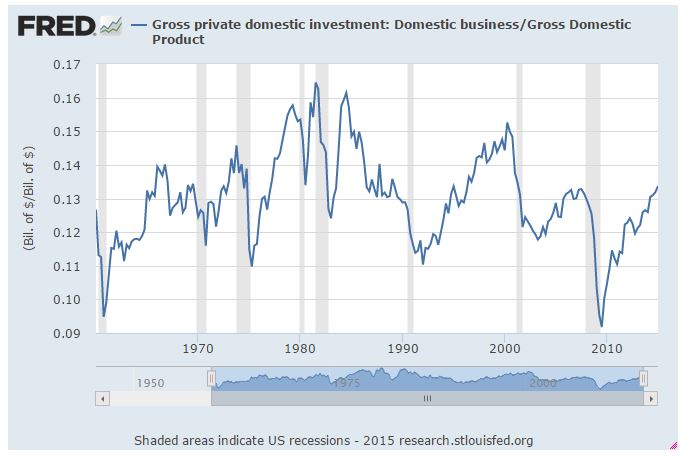

The data, however, do not support the claim that risk-aversion has increased. Corporate investment as a percentage of GDP, for example, is higher now than it was at the prior cycle high, and at roughly the same level as the highs of the cycles of the 1960s and early 1970s.

A second mechanism through which ROICs can sustainably increase is through increases in barriers to entry. Barriers to entry keep competition out. As they get stronger, the players protected by them are able to successfully operate at increased levels of profitability, free from the threat of competition.

This brings us to the subject of the piece, the “Winner Take All” economy. The point is difficult to quantify or conclusively prove, but it seems that the dramatic technological changes of the last 20 years have made credible competition in certain key sectors of our economy more difficult, and have allowed dominant best-in-breed companies–the $AAPLs, $GOOGs, $MSFTs, $FBs, and so on of the world–to command sustainably higher profit margins.

The current U.S. economy seems to have more genuine monopolies than the economies of old–more companies that face little to no competition. The increase in monopoly businesses and monopoly products seems be due, at least in part, to the massive distributional, network-creative and network-protective power of the internet, and also the shift towards the production of non-physical things. A first-mover with a strong intangible product can distribute that product to the entire world at little cost, protect it as intellectual property, and build a profitable user network around it that other corporations will have an increasingly difficult time competing with.

Think for a moment: how would one go about competing with the likes of an $AAPL, $GOOG, $MSFT or $FB–the Iphone, Google search, Windows/Office, or Facebook? Would it even be possible? These companies have tried to enter into each other’s domains in the past, but they’ve never succeeded–in fact, they’ve never even come close. Every competitive effort has turned out to be a hopeless waste of time and money–a Microsoft phone, a Facebook search, a Google Plus, and so on. It’s no wonder, then, that these companies have been able to enjoy elevated profit margins–in excess of 20% on a net basis–that would have been unheard of 50 years ago. The effect seems to extend, albeit to a lesser degree, to dominant non-technological companies that have been able to leverage modern technology to efficiently expand their customer bases, the pervasiveness and relevance of their brands, and the dominance of their market positions.

To be fair, there are a number of other, non-technological explanations that one can point to in to account for the increase in barriers to entry. Our economy, for example, has become increasingly complex from a regulatory perspective, and complex regulation tends to make new entry more difficult. Additionally, over the last few decades, the corporate sector has shown an increased preference for deploying excess capital into mergers and acquisitions rather than new investment, which naturally tends to reduce competition. The point, however, is that technology, with its creation of massive, ubiquitous companies that are literally impossible to compete with, appears to be the single biggest driver of the profit margin increase in aggregate.

The possibility that increased barriers to entry represent the primary causal factor behind the observed profit margin increase is supported by the fact that the increase has not been broad-based, as would be expected if it were a simple consequence of weak labor bargaining power, low interest rates, or some other generic factor associated with the corporate cost structure. Rather, it is concentrated in specific sectors–especially the technology sector–and in specifically dominant individual large cap, blue-chip names.

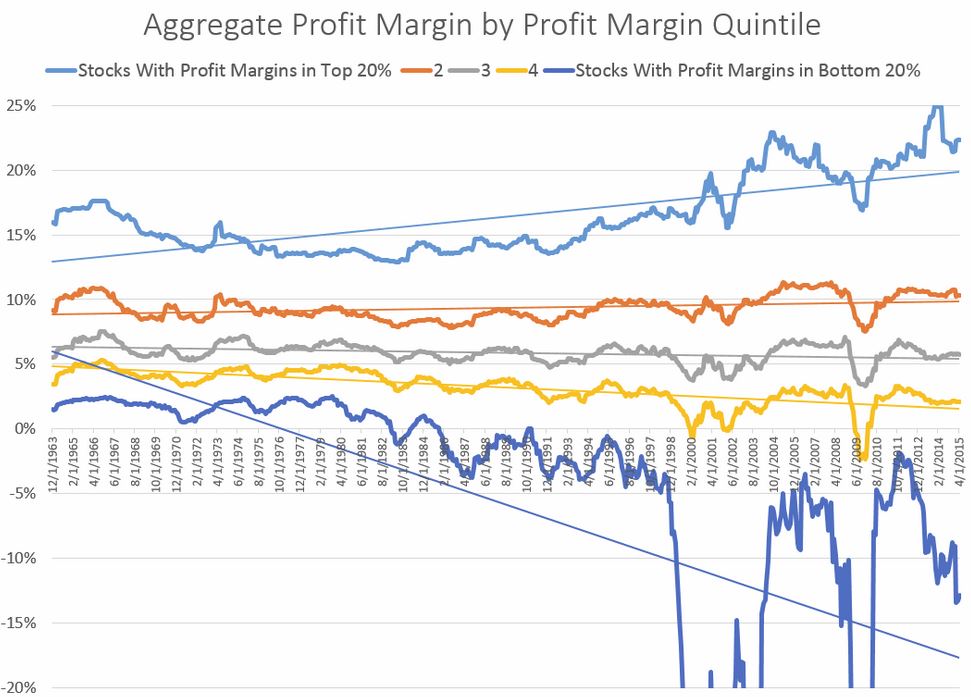

Fortunately, we don’t have to accept the explanation on faith. We can test it empirically, in actual data. If a “Winner Take All” economy, with its associated barriers to entry–first-mover barriers, network barriers, patent barriers, size barriers, regulatory barriers, and so on–has allowed an increasingly concentrated group of dominant companies to earn substantially higher profit margins, then we should expect the following. If we separate companies in the market into different tiers based on their profit margins, we should expect the higher tiers to have seen larger increases in their profit margins in recent decades than the lower tiers. Increases in the profit margins of the higher tiers–at the expense of the lower tiers–would represent the “Winner” gradually “Taking All.”

I recently asked my favorite blogger, the brilliant Patrick O’Shaughnessy of O’Shaugnessy Asset Management (Twitter: @millennial_inv, Blog: http://www.investorfieldguide.com), to put the hypothesis to the test by separating companies in the market into different bins by profit margin, and then charting the aggregate profit margins of each bin. If our explanation is correct, then the aggregate profit margins of the higher bins should have increased more over the last few decades than the aggregated profit margins of the lower bins. Lo and behold, that’s exactly what the data shows. The profit margin increase of the last 20 years has not been broad-based, shared by all bins, but has instead been concentrated in the highest profit-margin bins. The companies in those bins have seen their profit margins explode, while the companies in the lower-tier bins have seen little if any increase–and for some bins, an outright reduction.

The following chart, taken from Patrick’s recent blog post, “The Rich Get Richer”, beautifully illustrates the point:

Notice that the profit margins of the various bins moved roughly commensurately up until the late 1980s and early 1990s. At that point, something happened. The profit margins of the top bin proceeded to explode, rising by over 1000 basis points (bps). The profit margins of the next two highest bins stayed roughly flat. And the profit margins of the two lowest bins actually fell–even as the labor and interest costs of companies in those bins were supposedly reduced. Overall, the dispersion of profit margins increased dramatically–which is the hallmark sign of a “Winner Take All” economy.

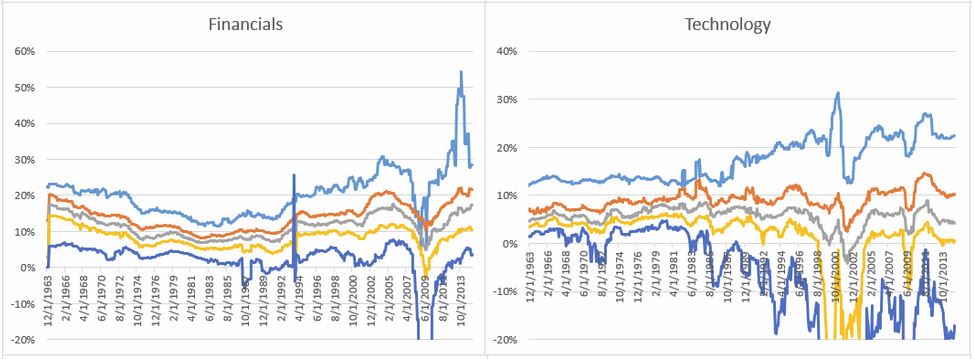

The effect was particularly pronounced in the two sectors that we wrote about previously–technology and finance–which together make up more than 40% of S&P 500 earnings.

As the chart shows, the profit margins of the top bins in these sectors have increased by over 1000 bps. The profit margins of the lowest two bins, in contrast, have either gone nowhere or outright contracted.

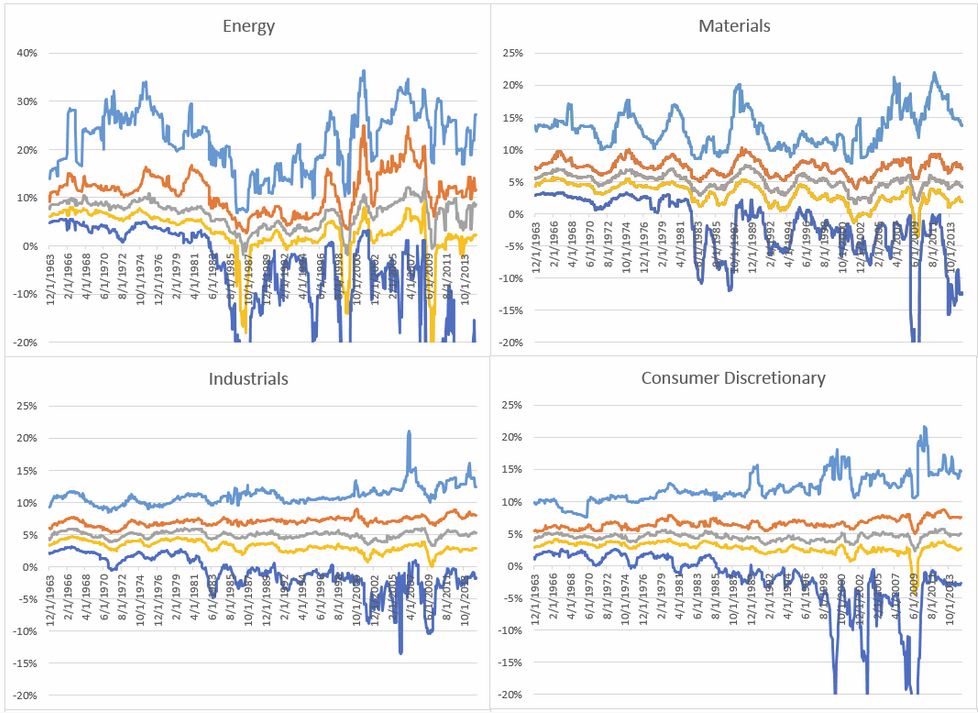

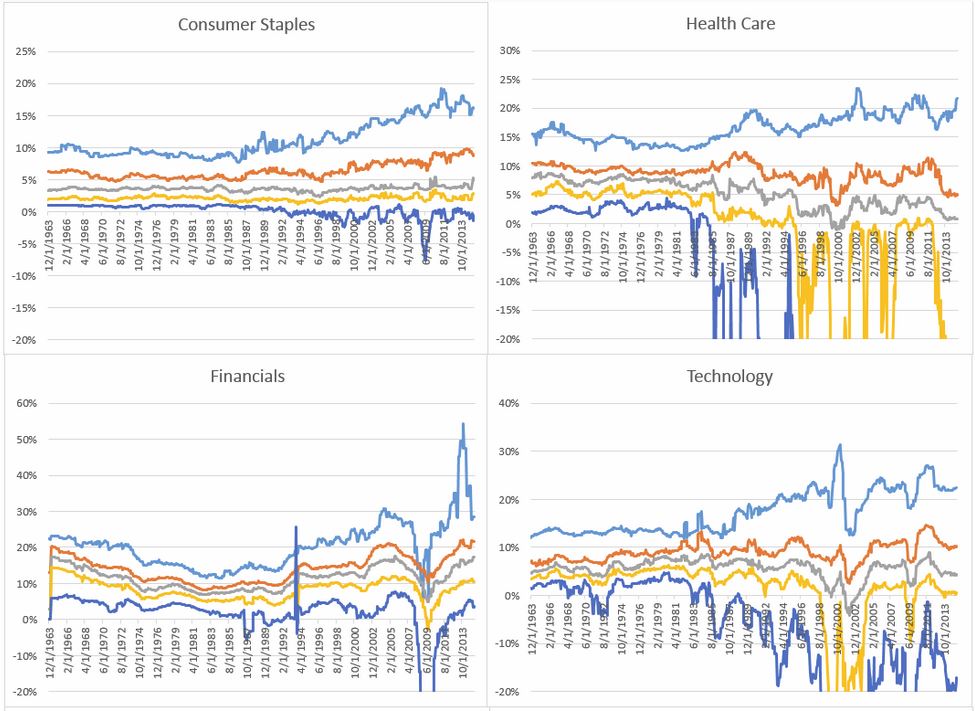

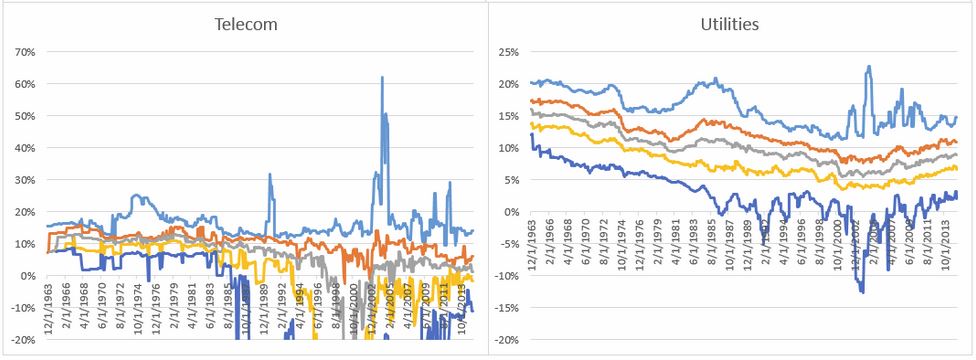

For reference, here are individual graphs for all sectors:

As our account would predict, companies that are farther away from the “new economy”–for example, companies in the energy and material sectors that sell basic commodities and that are price takers, or companies in the utility sector whose profit margins are determined by the government–do not show the effect. For the most part, the high profit margin bins in those sectors haven’t seen any more of a profit margin increase than the other bins. The effect is instead concentrated in sectors where the dominant players have pricing power–technology, finance, consumer staples, consumer discretionary, health care, and to a lesser extent, industrials.

It remains an unresolved question as to whether and for how long the trend towards a “Winner Take All” economy will persist. But open-minded investors should admit that it could persist for a very long time, if not forever–and that it could even extend further, with profit margins rising further. At any rate, given that profit margins have stayed firmly elevated for such a long time without any signs of sustainably falling, and given that we now have a compelling explanation for why they would be expected to stay elevated over the long-term, bearishly-inclined investors should seriously consider the possibility that the “mean-reversion” that they’ve been patiently waiting for isn’t going to happen, at least not to the extent expected.