The big surprise from Thursday’s Fed announcement was not the decision to hold interest rates at zero, which most Fed observers expected, but the revelation that an unidentified FOMC member–probably Narayana Kocherlakota, but possibly another dove–is now advocating the use of negative nominal interest rates as a policy tool:

What follows is a simplified explanation of how a policy of negative interest rates would work. The central bank would begin by enacting a large scale program of “quantitative easing” that would entail the creation of new money and the use that new money to buy assets from the private sector. The new money would end up on deposit at banks, where it would represent an excess cash reserve held physically in vaults or electronically on deposit at the central bank. The central bank would continue the program until the quantity of excess reserves in the banking system was very high. Indeed, the higher the quantity of those reserves, the more powerful–or rather, the more punitive–a policy of negative interest rates would end up being.

After saturating the system with excess reserves, the central bank would require individual banks that hold excess reserves to pay interest on them–effectively, a tax. Individual banks would then have three choices:

(1) Eat the associated expense, i.e., take it as a hit to profit,

(2) Pass the associated expense on to depositors, creating the equivalent of a negative interest rate on customer deposits, or

(3) Increase lending (or purchase assets), so that the excess reserves cease to be “excess”, but instead become “required” by the increased quantity of liabilities that the bank will bear.

This third option is important and confusing, so I’m going to spend some time elaborating on it. Recall that the issuance of loans and the purchase of assets by banks create new deposits, which are bank liabilities. Required reserves are calculated as a percentage of (certain types of) those liabilities. Importantly, required reserves do not incur interest under the policy (at least as the policy is currently being implemented in Europe), and so increases in lending, which increase the quantity of reserves that get classified as “required” as opposed to “excess”, represent a way to avoid the cost, both for banks individually, and for the banking system in aggregate.

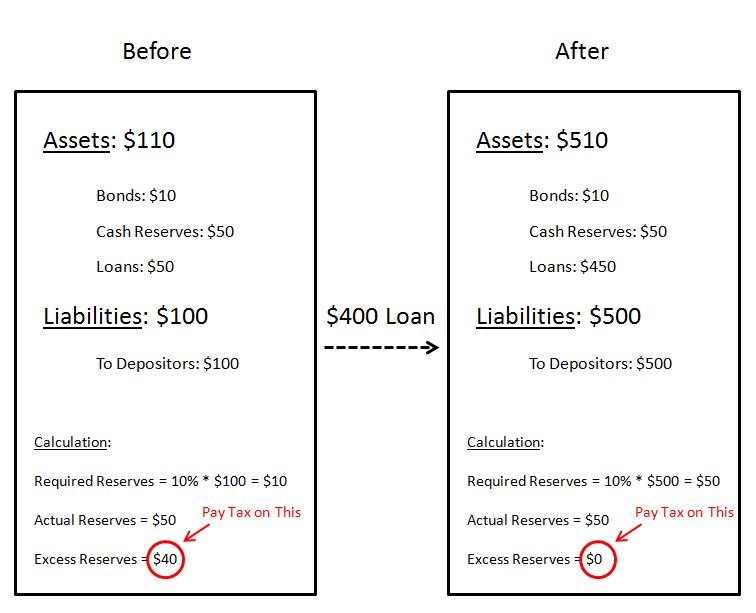

The following schematic illustrates with an example:

We have an individual bank–we’ll call it American Bank. This bank begins with $110 in assets, $50 of which are cash reserves, and $100 in deposit liabilities, all of which are subject to the reserve requirement. If we assume that the reserve requirement is 10% of deposit liabilities, then the bank will be required to hold $100 * 10% = $10 in reserves. But, in this case, American bank is holding $50 in reserves–$40 more than it is required to hold. In a negative interest rate regime, it will have to pay interest, or tax, on that excess. So if the annual interest rate is -2%, it will have to pay $40 * .02 = 80 cents (8% of its $10 in capital, so no small amount!). The payment will go to the central bank, or to the treasury, or whoever.

Now, let’s suppose that American Bank issues $400 in a new loan. The way it would actually make this loan would be to simply create (from essentially nothing) a new deposit account for the borrower, with a $400 balance in it, that the borrower can draw from on demand. Let’s suppose that the borrower keeps the $400 in that same account, i.e., doesn’t withdraw it as physical cash or move it to another bank by transferring it or writing a check on it that gets cashed elsewhere. It follows that the bank will not have to come up with any actual money to fund the loan. The money that is funding the loan is the money that the loan created, which has stayed inside the bank. Only when that money leaves the bank does the bank have to “come up with it.”

After the loan is made, American Bank will have $510 in assets (the $110 in previous assets plus the $400 in new loans, that the borrower owes it), and $500 in liabilities (the $100 in previous deposits plus the new $400 that the borrower is holding on deposit with it). The required reserves will be $500 * 10% = $50, which is exactly the amount of cash that it has on hand. So it’s excess reserves will be $0 and it will not have to pay any interest or tax. Problem solved.

Now, suppose that the borrower decides to move the $400 that it has on deposit at American Bank to some other bank. But American Bank only has $50 in actual cash reserves to move. And those reserves are needed to meet the $50 in required reserves, so they can’t be moved. How, then, will the bank satisfy the borrower’s demand to send $400 to another bank? Easy–it will simply go into the Fed Funds market, borrow $400 from a bank that has excess funds to lend, and transfer the funds to the bank that the borrower wants them transferred to. Its $400 liability to the borrower will then disappear, to be replaced by a $400 liability to the bank from which it borrowed.

Of course, nothing will actually physically move in this process. The transfer will occur electronically, at the Fed, through the adjustment of the deposit balances of the involved banks–essentially, a spreadsheet operation. The bank that is lending $400 to American Bank will see its deposit balance at the Fed fall by $400, American Bank will see no change to its deposit balance, and the bank that is receiving the $400, which is the bank that the borrower is moving the money to, will see its deposit balance increase by $400.

But what if other banks lack sufficient funds, over and above the amount that they themselves have to hold to meet reserve requirements, to lend to American Bank? That won’t happen. The Fed uses asset purchases and asset sales to manipulate the quantity of funds in the banking system, over and above those that are needed to meet reserve requirements, so that there are always sufficient excess funds available to be lent, at the Fed Funds rate, the Fed’s target short-term rate. When the Fed wants that rate to be higher, it uses asset sales, which take funds (money) out of the system and put assets (e.g., bonds) in, to make the supply of excess funds available to be lent tighter; if it wants that rate to be lower, it uses asset purchases, which take assets (e.g., bonds) out of the system and put new funds (money) in, to make the supply of excess funds available to be lent more plentiful. Importantly, the targeted variable in the Fed Funds market is not the supply of excess funds available to be lent, but the price. The Fed, through its operations, effectively guarantees that there will always be a sufficient supply of excess funds available to be lent at the target price–though it may be an expensive price, if the Fed wants less lending to take place.

But what if other banks refuse to lend to American Bank, even though there are excess funds are available to be lent? Again, not a problem. If the bank can prove that it is worthy of a loan, then it can borrow directly from the Fed, through the discount window, at a price slightly higher than the price targeted in the Fed Funds market.

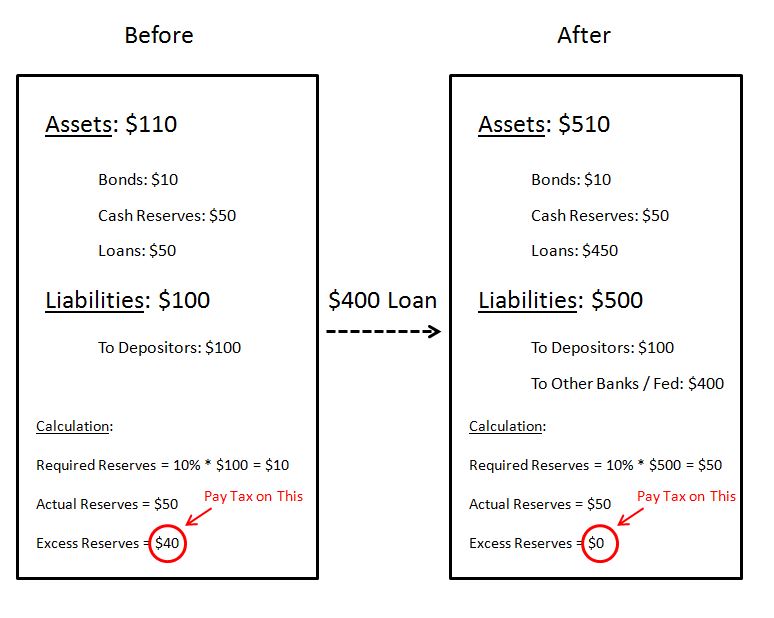

To summarize, if the borrower moves his deposit to another bank, the picture changes to look like this:

As you can see, nothing really changes when the borrower moves the money except the composition of the bank’s deposit liabilities. Previously, they were liabilities to an individual, now they are liabilities to other banks, or to the Fed. They are still subject to the reserve requirement, and so the bank’s reserve excess remains zero.

It’s important to understand that when banks implement this third option, the cash reserves that were “excess” continue to exist as reserves–as physical cash held in storage or as balances held on deposit at the central bank. Only the central bank can (legally) create or destroy them, which it does through its open market operations–its purchase and sale of assets from the private sector. Because the reserves still exist, they still have to be held by some person or entity. Unless customers extract them and hold them physically as metal coins and paper bills, the banking system in aggregate–some bank somewhere–continues to hold them.

The point, however, is that they no longer get classified as excess reserves. They become required reserves, required by the larger quantity of deposit liabilities that the banking system ends up bearing. Because required reserves do not incur interest expense under the policy, an increase in aggregate bank lending, which will increase the quantity of reserves that get classified as “required” as opposed to “excess”, represents a potential way for banks to avoid the cost–both individually, and in aggregate.

Returning to the question of how banks would respond, there’s obviously a limit to the cost increase that they will be willing to absorb. If the negative rate is “negative” enough, they will try to pass that increase on to their customers, charging interest to those who hold deposits with them and who cause them to have unneeded excess reserves in the first place. Proponents of the policy believe that this outcome would stimulate the economy by increasing the velocity of money. Bank deposits would become an item that everyone wants to get rid off, but that someone has to hold. They would get tossed around like a hot potato, moving from individual to individual, in the form of increased spending, trading and investing.

Of course, spending, trading and investing aren’t the only ways to get rid of a bank deposit. A depositor can take physical delivery of the money, and put it into her own storage, outside of the banking system–a piggy bank, a mattress, a safe, wherever. The assumption is that this type of maneuver would be inconvenient and therefore rarely used. If the assumption were to be proven wrong, the next step would be to eliminate physical money altogether, so that all cash ends up trapped inside the banking system, with the owners forced to pay interest on it for as long as they choose to continue to hold it.

With respect to the third option, which is to increase lending, banks aren’t always able to increase their lending in the normal ways–they need credible borrowing demand from borrowers. That demand isn’t guaranteed to be there. To generate it, however, they can offer to pay borrowers to borrow–funding the payments with the income that they generate from charging their depositors interest. The negative interest rate regime will then come full circle, in a perverse reversal of the normal banking arrangement–instead of borrowers paying depositors to borrow their money, with the banking system acting as an intermediary, depositors will be paying borrowers to borrow their money, with the banking system again acting as an intermediary.

In assessing the third option, we can’t forget the impact of regulatory capital ratios, which can quickly become limiting. In our example, American Bank had $50 in cash reserves, which carry a risk-weighting of 0%, $10 in bonds which we assume are government bonds that also carry a risk-weighting of 0%, and $50 in retail loans, which carry a risk-weighting of 100%. Simplistically, the bank has $10 in capital, so the bank’s capital ratio would be $10 / (0% * $50 + 0% * $10 + 100% * $50) = $10 / $50 = 20%, well above the 8% Basel requirement. After the new $400 loan, however, the bank’s capital ratio would fall to $10 / (0% * $50 + 0% * $10 + 100% * $450) = $10 / $450 = 2%, which is well below the 8% Basel requirement. So American Bank would not actually be able to do what I just proposed.

Given limits to regulatory capital ratios, the only way for banks to use the third option to substantially increase required reserves and reduce interest expense would be to buy assets that don’t carry a risk-weighting–banks would either have to do that, or raise capital, which no bank is going to want to do. It follows that the types of interest rates that would see the biggest relative drop under a regime of substantially negative interest rates would not be the risk-bearing interest rates that real economic participants pay, but the risk-free interest rates that governments and other risk-free borrowers pay. Those securities would get gobbled up by the banking system, pushed to rates as negative as the negative rates on excess reserves.

Proponents of the policy assume that if banks choose to respond by increasing their lending to the private sector, that the increase will necessarily be stimulative to economic activity. That may be true, but not necessarily. It’s possible that banks could issue zero interest rate loans to highly creditworthy private sector borrowers who don’t want or need the money, and who have no plans to spend or invest it, but who agree to take and hold the loans in exchange for other perks–for example, a waiving of interest and fees on other deposits being held. Such loans–even though they wouldn’t be doing anything economically–would increase the bank’s deposit liabilities and required reserves, and therefore decrease the portion of its reserves that get classified as “excess”, eliminating the associated interest expense. Of course, these loans, even though safe, would carry regulatory risk, and so the ability of the banking system to engage in them would be limited by regulatory capital.

Earlier, we noted that it’s important for the central bank to inject excess reserves into the system through quantitative easing prior to implementing a policy of negative interest rates. The reason is obvious. On the assumption that lending stays constant, every excess reserve in the system is going to have to be held, and paid interest on, by some bank, and ultimately, by some depositor, the person who actually owns the money, and who is holding it on deposit at the bank. Quantitative easing increases the quantity of bank deposits and excess reserves in the system. It therefore increases the number of assets in the system that are directly subject to negative rates, and that incur the obligation to pay those rates.

To explain with an example, if the private sector’s asset portfolio consists of $10 in cash and $1000 in fixed income assets, and the Fed imposes a negative interest rate, that rate will only directly hit $10. But if the Fed goes in and buys 100% of the fixed income assets, swapping them for newly issued money, such that the private sector’s asset portfolio shifts to $1010 of cash and $0 in fixed income assets, and if it then imposes a negative interest rate, that rate will directly hit all $1010–the private sector’s entire asset portfolio. It will cause that much more pain, and will therefore have that much more of an effect.

Of course, this effect would come at a cost. Psychologically, there’s a big difference between not making money, as inflation slowly erodes its value, and outright losing it–particularly meaningful amounts of it. People tend to suffer much more at the latter, and are therefore likely to go to far greater lengths to avoid it. The result of the policy, then, would not be an increase in what economies at the zero-lower-bound need–well-planned, productive, useful, job-creative investment–but rather panicky, rushed, impulsive financial speculation that leads to asset bubbles and the misallocation of capital, with detrimental long-term consequences on both output and well-being.

Worse, the policy is likely to be deflationary, not inflationary. Like any tax, it destroys financial wealth–the financial wealth of the people that have to pay it. That wealth is taken out of the system. Granted, the wealth can be reintroduced into the system if the government that receives it resolves to take it and spend it. But in the instances of unconventional monetary policy that have played out so far–quantitative easing globally and negative interest rates in Europe–that hasn’t happened. Governments have pocketed the income from these programs, sending it into the financial “black hole” of deficit reduction.

Even if the wealth is reinjected into the system in the form of tax cuts or increased government spending elsewhere, we have to consider the behavioral effects on those that rely, at least in part, on returns on accumulated savings to fund their expenditures. Those individuals–typically older people–represent a growing percentage of western society. Under conventional policy, they simply have to deal with low interest rates on their savings–tough, but manageable. To require them to deal with negative interest rates–confiscation of a certain percentage of their savings as each year passes–would be a significant paradigm shift. Their confidence in their ability to fund their futures–their future spending–would likely fall. They would therefore spend less, not more, exacerbating the economic weakness. Granted, the threat of punishment for holding risk-free assets might coax them into speculating in the risky financial bubbles that will have formed–but then again, it might not. If it does, they will suffer on the other end.

Hopefully at this point, the reader intuitively recognizes that imposing meaningfully negative interest rates on the population is a truly terrible idea. If we’re only talking about a few basis points, a sort of “token” tiny negative rate that is put in place for optics, as has been done in Europe–fine, people will grow accustomed to it and eventually ignore it. But a serious use of negative rates, that involves the imposition of levels meaningfully below zero–e.g., -2%, -3%, -4%, and so on–would be awful for the economy, and for people more generally.

The problem of how to stimulate a demand-deficient economy is fundamentally a behavioral problem. It needs to be evaluated from a behavioral perspective. We have to ask ourselves, what specific behavior do we want to encourage? We know the answer. We want corporations and the entrepreneurial class to invest in the production of useful, wanted things. Their investment creates jobs, which produce incomes for working people, incomes that can then be used to purchase those useful, wanted things, completing a virtuous cycle in which everyone benefits and prospers.

The question is, if corporations and the entrepreneurial class aren’t doing enough of that, how do we get them to do more of it? The answer, which I’m going to elaborate on in the next piece, is not by punishing them with a highly repressive monetary policy, a policy that goes so far as to confiscate their money unless they hand it off to someone else. Rather, the answer is to put the economy in a condition that causes them to become confident that if they invest in the production of useful, wanted things, that they will receive the due reward, profit. In an economy like ours, a more-or-less structurally sound economy that happens to suffer from deficient aggregate demand associated with legacy private sector debt and wealth inequality issues, the way to do that is with fiscal policy.